Staying Poised for Better Days

Contributed by Doug Walters, Max Berkovich, David Lemire, Eh Ka Paw

The market sell-off continued in Q2 2022. Inflation was the buzzword of the quarter, and all eyes were on The Fed to see how they would respond. There were many pain points for investors, but those that strayed into questionable “shiny objects” like crypto and SPACs had the deepest wounds to lick.

Inflation Concerns Inflating

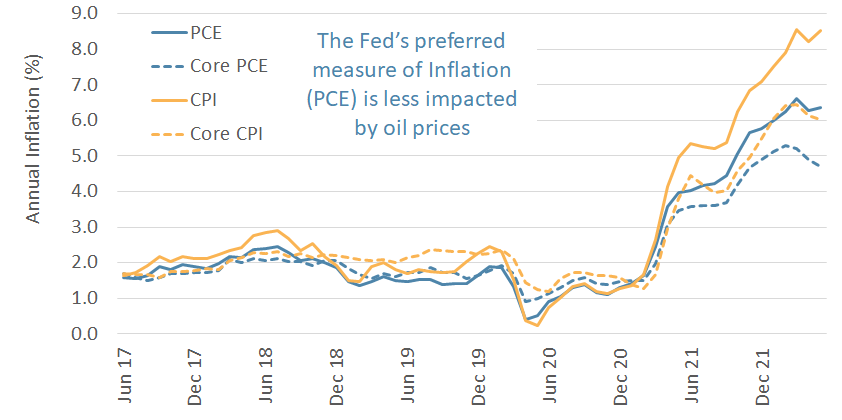

If there was one common theme in Q2, it was inflation and, more specifically, whether or not it is peaking. Personal Consumption Expenditures (PCE) inflation, TheFed’s preferred measure, has weakened over the past two months.

- However, the more famous Consumer Price Index (CPI) inflation has broken away from PCE due to the heavier weighting of energy inputs like oil. The price of oil remains high partly due to the war in Ukraine and partly due to tight pandemic supplies. Oil ended the quarter just 7% off its 2022 high (with little sign of abating).

- Other prices are starting to moderate from their peaks. Since March, lumber is down nearly 60%, copper is down over 20%, and cotton is down almost 40%.

- Food and automobile prices have yet to weaken.

Only time will tell if inflation has peaked, but the Fed has its sights set on ensuring that is the case.

Chart 1: Some measures of inflation are off their peak

The Fed’s preferred measure of inflation is off its peak (for now?)

Source: US Bureau of Labor Statistics, Bureau of Economic Analysis

A Singular Focus

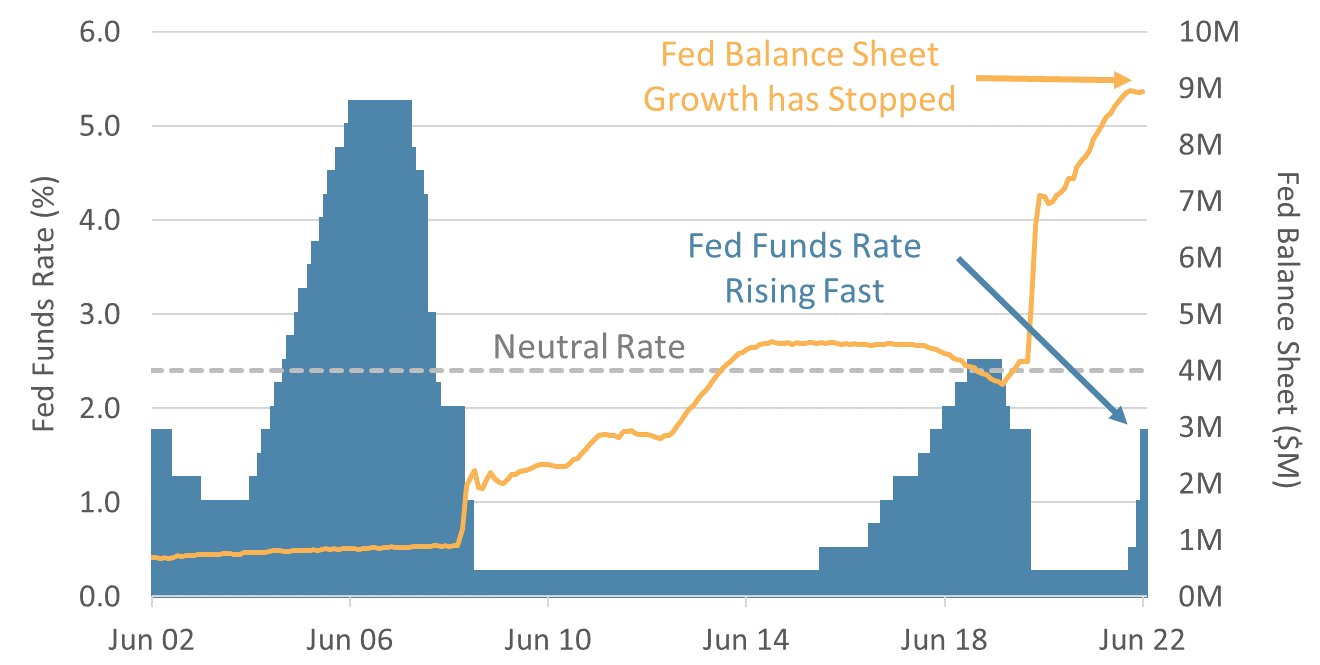

The Fed has its sights set on reducing inflation, using all the tools in its arsenal – most notably rate increases and quantitative tightening (balance sheet).

On rates:

- The Fed Funds Rate is rising fast but is still below the 2.4% level discussed as being the neutral rate. The neutral rate is where the Fed believes its rates are neither stimulative nor restrictive.

- The Fed is currently projecting to raise rates to 3.8% in 2023 before beginning an easing path back toward the neutral rate.

On the balance sheet:

- The Fed’s balance sheet has ballooned to $9T through “quantitative easing” (bond purchases). This month they began the process of tightening by simply ceasing the reinvestment of maturing securities proceeds.

Bond yields are on the rise due to both of these actions. Bond yields have been very low recently and are still low by historical standards. Long-term, investors will benefit from bonds that provide a more attractive yield.

Chart 2: the Fed Response to inflation Accelerates

The Fed is addressing inflation with rates and its balance sheet

Source: The US Federal Reserve

Stock Challenges

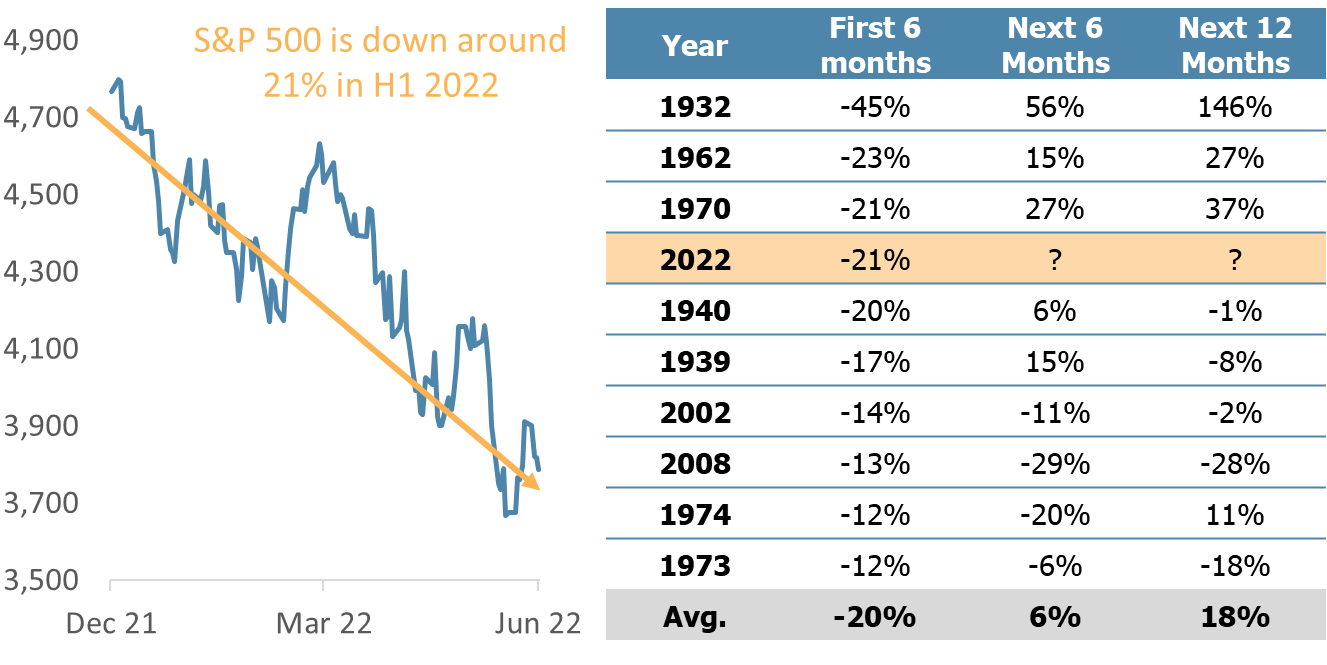

US stocks had a historically bad start to the year, with the S&P 500 recording its fifth-worst start to the year since 1930, falling 21%.

- The average decline of the ten worst starts to the year was 20%.

- Of those, the average price return of the next six months was 6%.

- The average price return of the next 12 months was 18%.

There is significant variation in the months following poor equity performance, but on average, patience has been rewarded with a rebound. There is no way of knowing what the future holds, but as evidence-based investors, we always look to ensure history is on our side.

Chart 3: A Historically Bad First Half

US stocks had a historically bad start to the year, but that does not mean H2 will suffer the same fate

Source: Factset, S&P 500 price return

Not So Shiny Objects

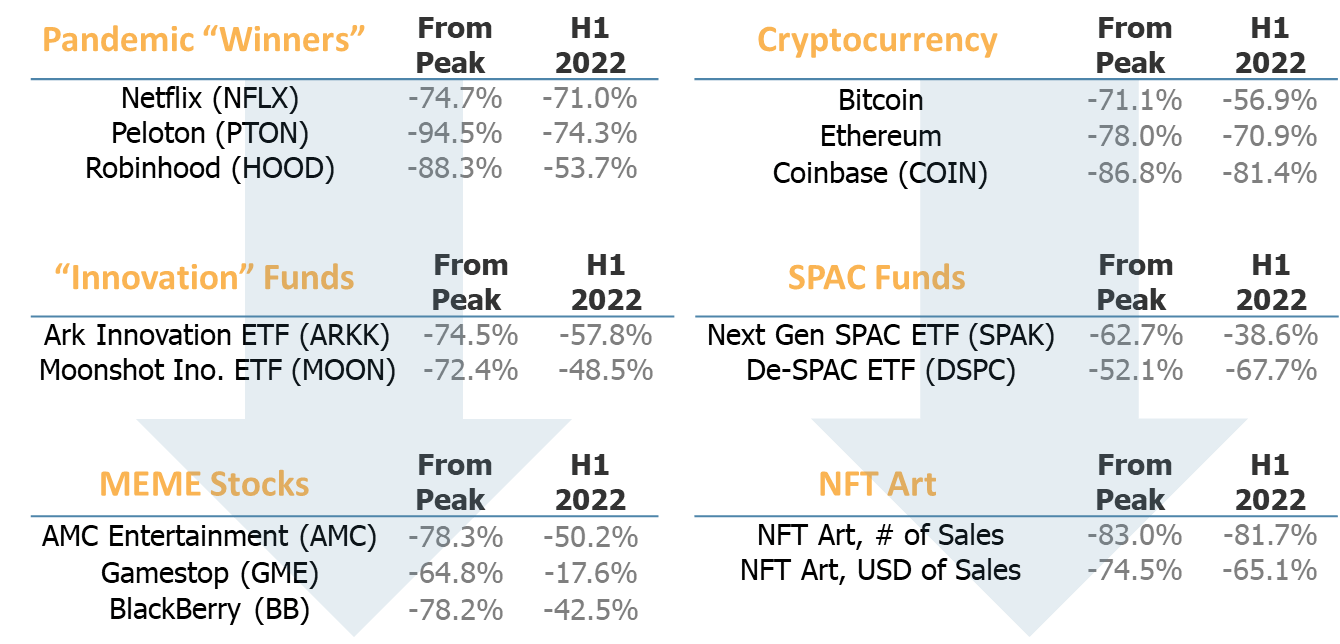

The first half was bad for equities generally, but it was a much worse H1 for previous market darlings. The many shiny objects that have been drawing investor attention in recent years have had a dreadful run this year. What happened?

- Easy money from the Fed and Congress led to excess risk-taking and the chasing of shiny objects.

- With easy money disappearing, assets driven up by nothing more than speculation and FOMO (fear of missing out) have predictably come crashing down.

- The pain may not be over for some of these assets that have little-to-no fundamental value backing their prices.

A focus on evidence (not emotion) based investing will have successfully steered investors clear of these enticing objects of affection.

Chart 4: Shiny Objects Lost Their Luster

It was a much worse first half for previous high-flyers

Source: Price return data except for NFT Art; Factset, Coindesk, NonFungible

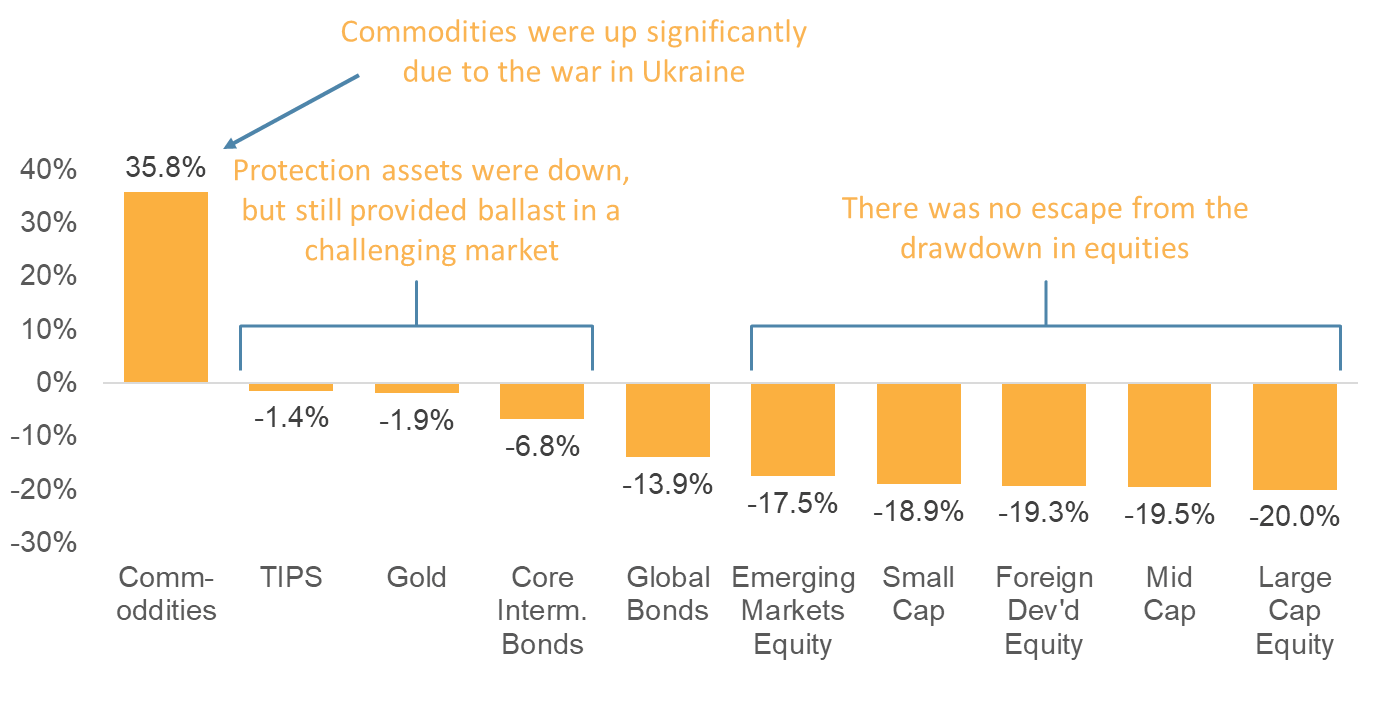

Few Places to Hide

It was a difficult first half, even for a diversified portfolio. Risk assets fell across the board in the first half of the year. Protection assets such as bonds were also down, but not as much, and therefore provided some rebalancing ballast.

- Equities fell across regions and market cap. However, value significantly outperformed growth.

- Gold proved once again (as it did in 2020) to be a good store of value in a challenging equity environment.

- Commodities spiked primarily due to oil which is elevated by pandemic supply constraints and the war in Ukraine.

- TIPS have done relatively well. We believe that dynamic has played out and have recently moved to underweight.

Difficult investment years are not uncommon. Investments are risky assets, and the reward we get for taking that risk is attractive long-term returns.

Chart 5: H1 2022 Asset Class Performance

A Difficult First Half for Equities

Source: Factset

We recently wrote about how a handful of years can shape your long-term investing success. We are not talking about those exceptionally good years but rather the bad ones. And 2022 has clearly been one of those bad ones. The challenge with a really bad year for investment markets is the higher potential for “permanent loss of capital.” That permanent loss can come in two common forms:

- Bad investments. Look at the list of “shiny objects” above for examples. There is a good chance that many of those losses are permanent. If the market weakness continues, there will be more examples of low-quality securities that suffer permanent loss. As discussed above, investing based on science and not speculation can avoid most of these pitfalls.

- Behavioral biases. As humans, we are not wired to be good investors and years like 2022 bring out the worst of our instincts. Action bias, overconfidence, and loss aversion are all examples of biases that contribute to the urge to actively enter and exit investment markets. Market timing has two outcomes: you get lucky and outperform, or you suffer permanent loss of capital.

Our challenge to investors in Q3 is to steer clear of harmful behavioral biases. Knowing is half the battle. Being aware of these innate biases allows you to take control of them through process and discipline, focusing on logic, not emotion. Stick with your well-diversified portfolio and take advantage of market moves through opportunistic rebalancing. Better days will come, and when they do, your portfolio will be poised to capitalize.

About Strategic

Founded in 1979, Strategic is a leading investment and wealth management firm managing and advising on total client assets of over $2 billion.

Disclosures

Strategic Financial Services, Inc. is registered with the Securities and Exchange Commission (SEC) as an Investment Advisor. The term “registered” signifies compliance with regulatory requirements and does not imply a certain level of skill or training.

The information provided on our website, including weekly market commentaries, financial planning articles, and other educational resources, is intended solely for educational purposes. It is designed to offer insights into financial planning and investment management, aiming to enhance understanding of financial concepts, strategies, and market trends. This content should not be interpreted as personalized investment advice or a recommendation for any specific strategy, financial planning approach, or investment product. Financial decisions are deeply personal and should be made considering the individual’s specific circumstances, goals, and risk tolerance. We recommend consulting with a professional financial advisor for personalized advice.

Please be aware that Strategic Financial Services, Inc. does not provide legal or tax advice. The content on this website is not intended to be used as such or as a substitute for legal or tax advice from a licensed professional. We advise seeking guidance from qualified legal and tax advisors regarding these matters.

Investment Risks and Portfolio Management.

The discussion of any investments on this website is for illustrative purposes only and provides no guarantee that the advisor will make any investments with the same or similar characteristics as those presented. The investments identified and described herein do not represent all the investments purchased or sold for client accounts. The selection of representative investments to discuss is based on various factors, including recent company news or earnings releases.

It should not be assumed that any investments discussed were or will be profitable. All investments involve risk, including the potential loss of principal. There is no assurance that investments mentioned will remain in client accounts at the time you view this information.

When index returns are mentioned on this site, they are provided as a general indicator of market conditions and are not representative of any client’s portfolio performance. Indices are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. Therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

While index returns are used as a framework to report on general market conditions, they should not be construed as an indicator of future performance of any specific investment or portfolio. Discussion of index returns is intended to provide context and insight, not to suggest that clients will achieve similar results. Each client’s portfolio is managed according to their specific investment goals and financial situation.

The opinions and any forward-looking statements expressed in the articles and videos featured in our resource center are as of the date of publication. These statements are based on current laws, regulations, market conditions, and other relevant factors, including third-party data. Given the dynamic nature of financial and regulatory environments, as well as potential changes in market conditions or economic circumstances, the information provided may become outdated or may no longer be accurate.

We rely on third-party data to form our opinions and projections, which means that these are subject to the same uncertainties that affect all data-dependent analyses. As such, we advise readers to exercise caution and not rely solely on the statements made herein for making financial decisions. It is recommended that investors consult with a professional advisor who can help assess the relevance and accuracy of the content in light of the current economic climate and personal financial situation.

Our website contains links to third-party websites as a convenience to our users. Strategic Financial Services, Inc. does not control, endorse, or guarantee the content found on such sites. We are not responsible for the accuracy, legality, or content of the external site or for that of subsequent links.

Contact the external site for answers to questions regarding its content.

The inclusion of any link does not imply our endorsement of the site, nor does it imply any association with its operators. Use of any such linked website is at the user’s own risk.