Opportunity and Risk as Inflation Tames

We are finally seeing signs that the Fed may be winning its battle against inflation. But stocks did not rejoice in Q3, as gains from earlier in the year were reduced in the quarter. In the US stock market, an epic gap has opened between the haves (mega-cap tech) and the have-nots (everyone else), introducing both opportunity and risk.

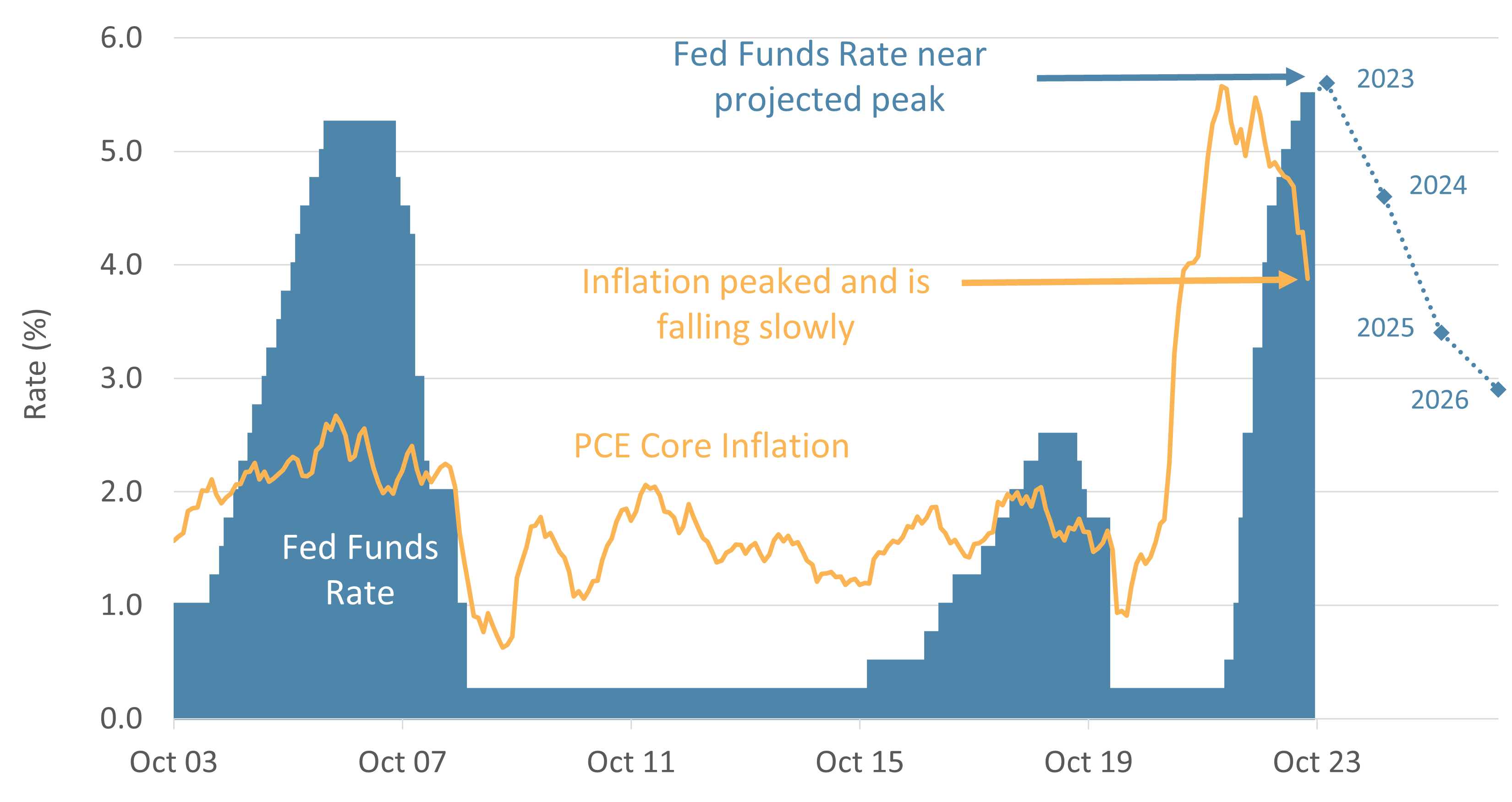

Peak rates expected later in 2023 as inflation falls

Finally! Inflation fell notably in Q3 as the Fed’s actions appear to, at long last, be having an impact. Fed Chairman Powell raised rates just a quarter of a percent in Q3 to 5.5%. Core PCE Inflation (a preferred Fed measure) slipped below 4% for the first time in two years, with inflation declines accelerating in the quarter. As a result, there are now mixed opinions among the Fed Governors about whether additional hikes will be needed. The median expected rate at year-end is just 5.6%, with rate cuts expected in 2024, 2025, and 2026.

Chart 1: The Fed Rate Hikes Resume… For Now

Source: The US Federal Reserve, Bureau of Economic Analysis

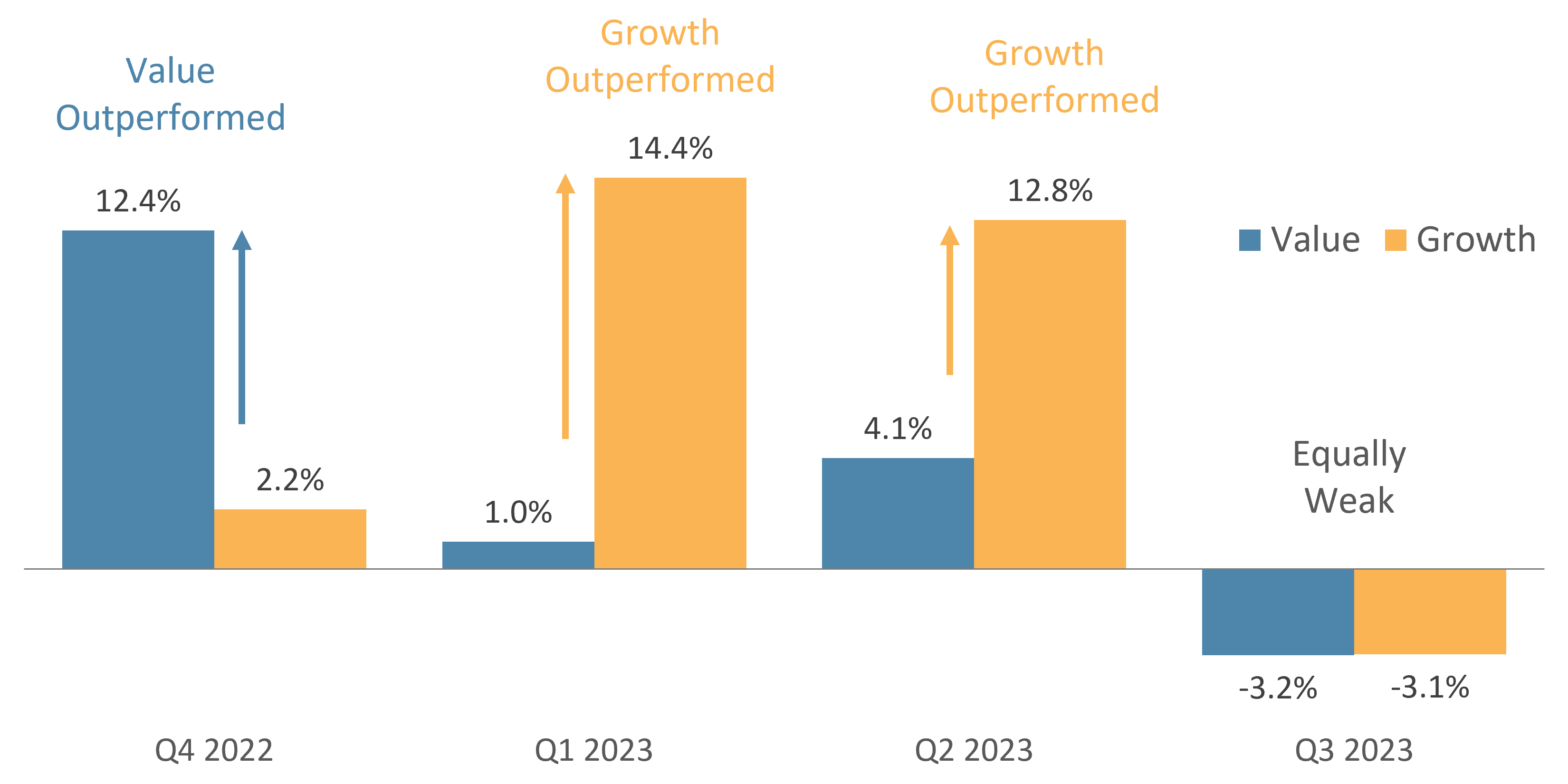

After big divergences, Value and Growth moved in unison

US Growth stocks have dominated performance for much of 2023, but Q3 saw modest and broad weakness. Despite the slowdown, the S&P 500 is still up about 13% on the year. Evidence-based investors with a Value tilt will have likely seen lower returns. Value stocks tend to outperform the broader market over time, but a handful of colossal technology stocks have driven 2023 returns. Historically, Value has tended to rebound from these bouts of underperformance, and we see opportunity in this market segment.

Chart 2: Value and Growth Performance Fell in Q3

Source: Russell 1000 Value and Growth Total Return

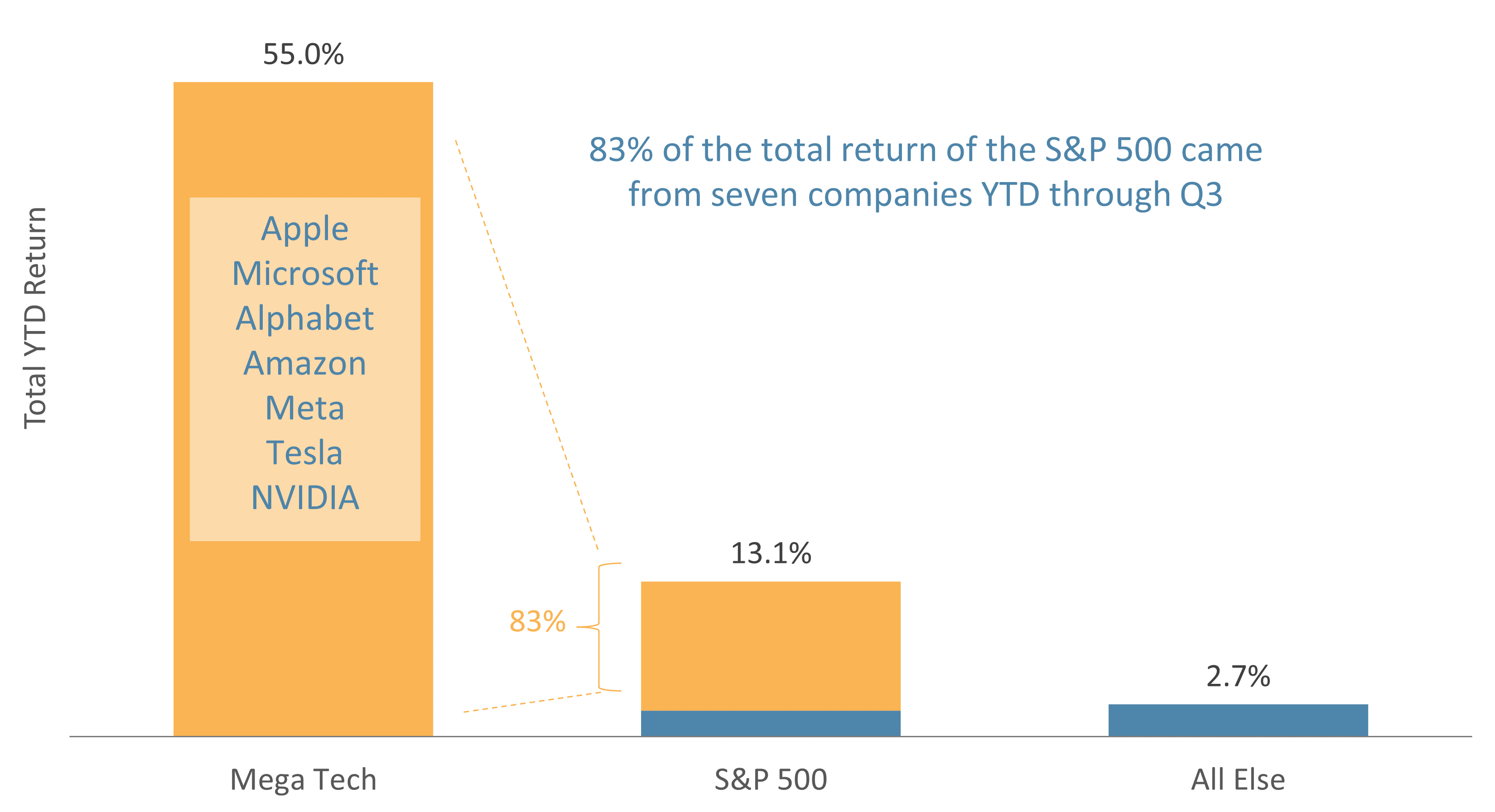

Year-to-date positive US stock performance had narrow leadership

A double-digit nine-month stock market return is respectable, but performance has been far lower outside of the mega-cap tech stocks. Seven (or 1.4%) of the 500 companies comprising the S&P 500 account for 27% of the index’s market cap. That same 1.4% of companies accounted for an astonishing 83% of the 13.1% S&P total return through Q3! Without them, the index would have only been up 2.7%. Market cap-weighted indexes like the S&P 500 have built significant concentration risk in recent years. We believe there are better opportunities that provide more diversified exposure. Our preferred approach is evidence-based factor investing.

Chart 3: Concentration Risk Remains High IN US EQUITIES

Source: Factset, S&P 500

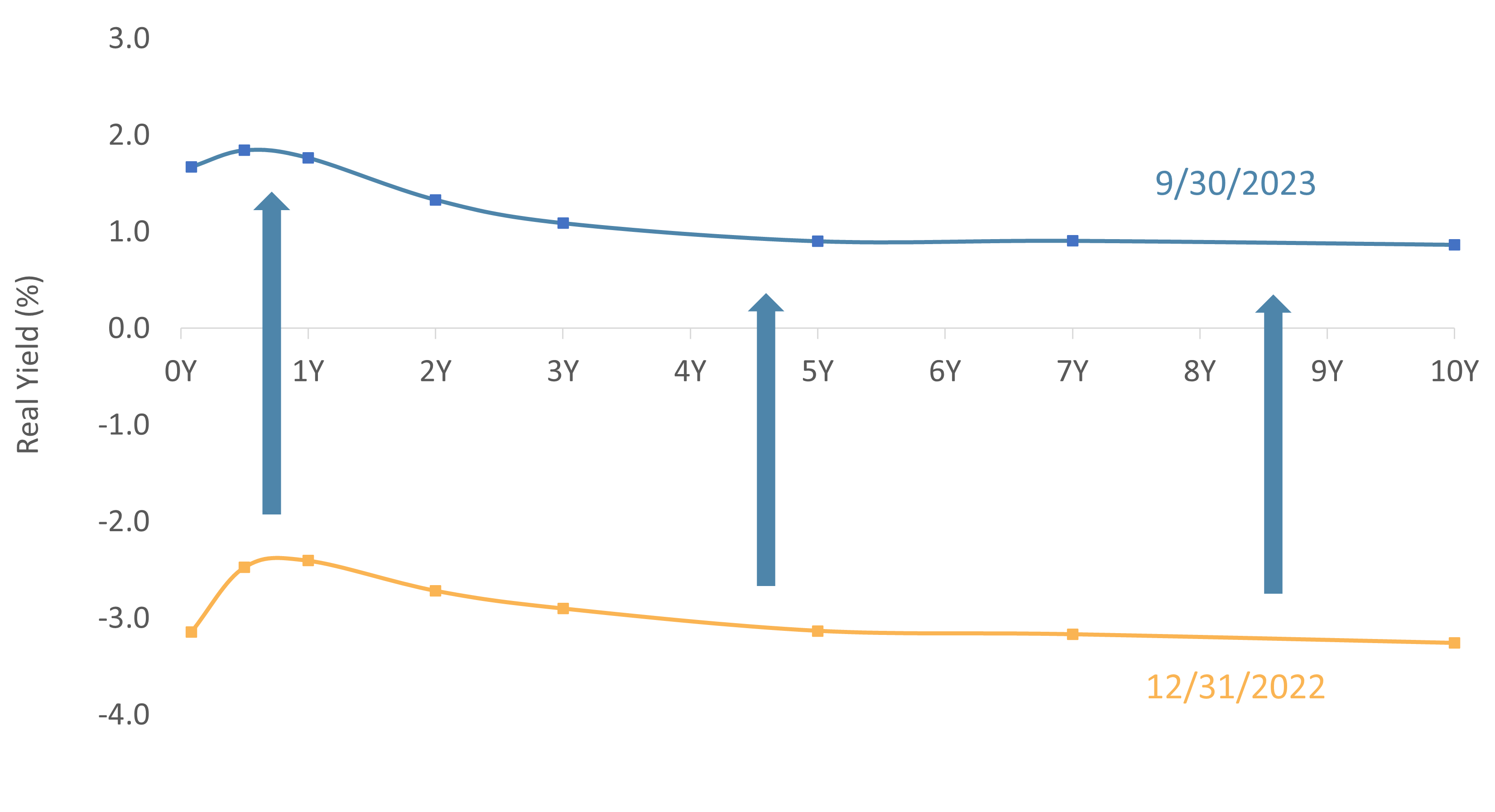

Real yields up on falling inflation and rising nominal yields

Real yields on Treasuries are slim but the highest they’ve been in years. The “real yield” refers to the yield on a bond above and beyond inflation. CPI-U Inflation (often used for calculating real returns on Treasuries) fell from 7.1% at the start of the year to 3.7%. At the same time, the yield curve shifted up, resulting in real positive yields across the curve for the first time in years. While yields are lower at the long end (because the curve is inverted), we increasingly see more opportunity there as rates appear to be peaking. Based on our research, the upside (should rates shift down) far outweighs the downside (should rates shift further up).

Chart 4: Real Treasury Yields Pushed Positive in Q3

Source: Factset, the Bureau of Labor Statistics

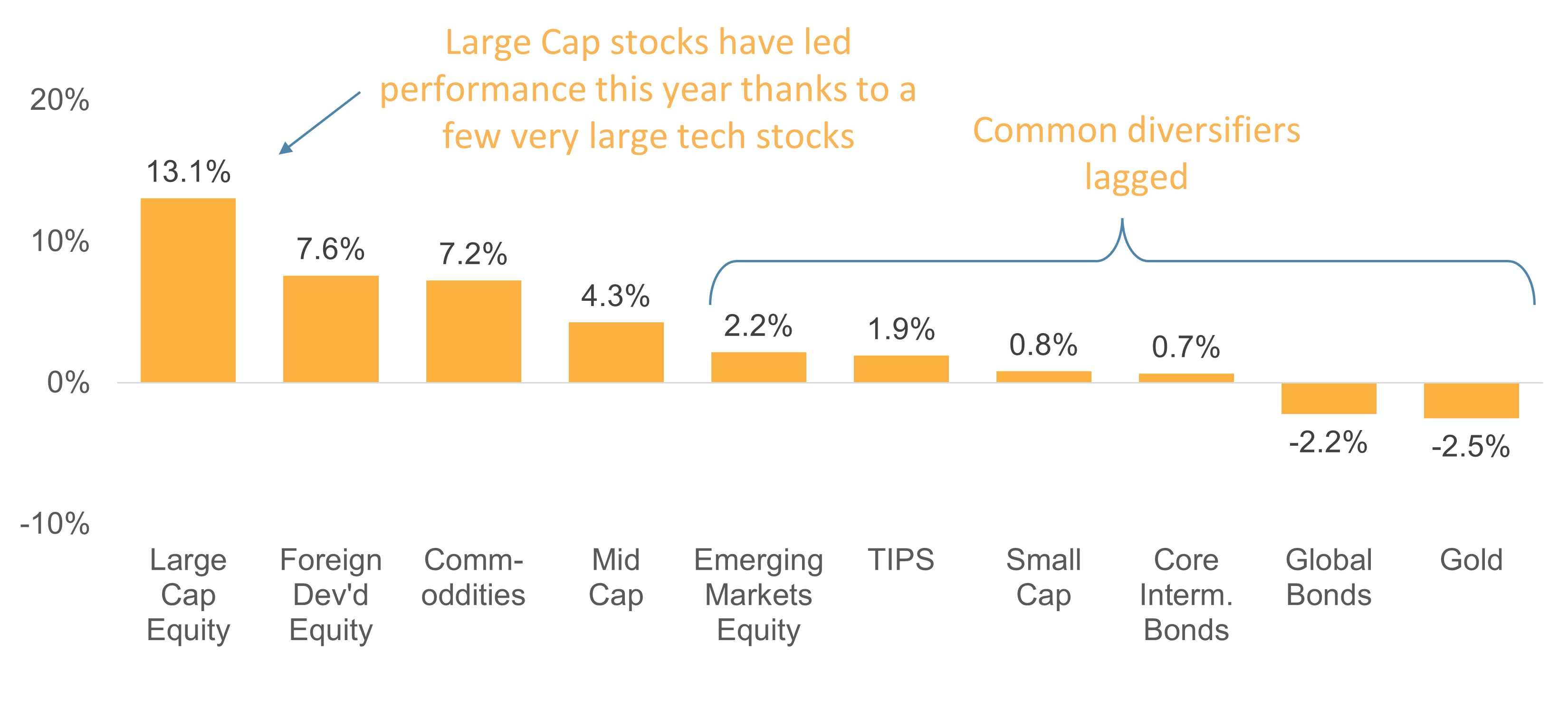

Q3 2023 saw modest declines

US equities pulled back slightly in Q3 after significant gains in the first half. US Large Cap remains atop the leaderboard despite a Q3 hiccup. Foreign-developed stocks had reasonable returns despite facing US dollar headwinds. Commodities rebounded in Q3 as oil prices spiked. In addition, many categories that we would commonly call “diversifiers” (e.g. Gold, TIPS, Small Cap, Emerging Markets, etc.) lagged. While diversifiers struggled year-to-date, their role in enhancing risked-adjusted returns in the long run is critical. With US large cap doing so well, it is easy to be tempted by home bias, but that is not good portfolio management. Stay diversified.

Chart 5: Asset Class Performance Through Q3 2023

Source: Factset, S&P 500

The final quarter of the year is upon us. Despite progress in taming inflation, there is still no consensus on some basic questions that will impact portfolio performance in the future. Will the Fed be able to navigate a soft landing? Is inflation finally tamed? And perhaps most basic… where in the world are we in the economic cycle? Are we approaching recovery or headed for a downturn? The aftermath of the pandemic has made these questions particularly difficult.

Our regular readers will know that we always make a point of saying we do not try to predict the future. It is a fool’s errand for investors. An impossible task. In this turbulent, post-pandemic economy, that impossible task is made even more so. But good investors do not need to predict the future, and we see a market laced with opportunity.

So, how does one approach Q4 without trying to predict? We focus on what we know. We follow the evidence, and within that evidence, we see a roadmap for the coming months. What do we know?

- The Value / Growth performance gap is very wide. Historically, significant underperformance of Value is often followed by big outperformance. We like Value generally, and in this environment, even more so.

- Momentum is a long-term winner. Historically, Momentum stocks (you can access these in a fund like MTUM or VFMO) have been one of the most persistent factors. We like this exposure as a passive way to pick up trending stocks.

- Long-term bonds are well-positioned to benefit from peaking yields. The upside potential if yields fall appears to far outweigh the downside risk should yields rise further.

- Market-cap-weighted indexes, like the S&P 500, have concentration risk in mega-cap tech stocks. In our opinion, these stocks have done great recently but pose a portfolio risk going forward. We favor less market-cap-weighted funds, like multi-factor ETFs.

- Diversification is a free lunch. You can improve risk-adjusted returns with exposure to a variety of asset classes. Don’t be sucked in by US large caps recent outperformance. We recommend including other assets like small cap, international, bonds, and gold.

None of the above observations require a prescient view of the future. Instead, they are opportunities based on what we know today that history would indicate have the potential to enhance portfolio returns. The future is always uncertain, and the best investors bias their portfolios to be prepared to take advantage of whatever it brings.

On behalf of the entire Strategic Financial Services team, I thank our clients, associates, friends, and family for placing your trust in us. You are an amazing community of which we are proud to be a part.

About Strategic

Founded in 1979, Strategic is a leading investment and wealth management firm managing and advising on total client assets of over $3 billion, as of 6/3/26.

Disclosures

Strategic Financial Services, Inc. is registered with the Securities and Exchange Commission (SEC) as an Investment Advisor. The term “registered” signifies compliance with regulatory requirements and does not imply a certain level of skill or training.

The information provided on our website, including weekly market commentaries, financial planning articles, and other educational resources, is intended solely for educational purposes. It is designed to offer insights into financial planning and investment management, aiming to enhance understanding of financial concepts, strategies, and market trends. This content should not be interpreted as personalized investment advice or a recommendation for any specific strategy, financial planning approach, or investment product. Financial decisions are deeply personal and should be made considering the individual’s specific circumstances, goals, and risk tolerance. We recommend consulting with a professional financial advisor for personalized advice.

Please be aware that Strategic Financial Services, Inc. does not provide legal or tax advice. The content on this website is not intended to be used as such or as a substitute for legal or tax advice from a licensed professional. We advise seeking guidance from qualified legal and tax advisors regarding these matters.

Investment Risks and Portfolio Management.

The discussion of any investments on this website is for illustrative purposes only and provides no guarantee that the advisor will make any investments with the same or similar characteristics as those presented. The investments identified and described herein do not represent all the investments purchased or sold for client accounts. The selection of representative investments to discuss is based on various factors, including recent company news or earnings releases.

It should not be assumed that any investments discussed were or will be profitable. All investments involve risk, including the potential loss of principal. There is no assurance that investments mentioned will remain in client accounts at the time you view this information.

When index returns are mentioned on this site, they are provided as a general indicator of market conditions and are not representative of any client’s portfolio performance. Indices are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. Therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

While index returns are used as a framework to report on general market conditions, they should not be construed as an indicator of future performance of any specific investment or portfolio. Discussion of index returns is intended to provide context and insight, not to suggest that clients will achieve similar results. Each client’s portfolio is managed according to their specific investment goals and financial situation.

The opinions and any forward-looking statements expressed in the articles and videos featured in our resource center are as of the date of publication. These statements are based on current laws, regulations, market conditions, and other relevant factors, including third-party data. Given the dynamic nature of financial and regulatory environments, as well as potential changes in market conditions or economic circumstances, the information provided may become outdated or may no longer be accurate.

We rely on third-party data to form our opinions and projections, which means that these are subject to the same uncertainties that affect all data-dependent analyses. As such, we advise readers to exercise caution and not rely solely on the statements made herein for making financial decisions. It is recommended that investors consult with a professional advisor who can help assess the relevance and accuracy of the content in light of the current economic climate and personal financial situation.

Our website contains links to third-party websites as a convenience to our users. Strategic Financial Services, Inc. does not control, endorse, or guarantee the content found on such sites. We are not responsible for the accuracy, legality, or content of the external site or for that of subsequent links.

Contact the external site for answers to questions regarding its content.

The inclusion of any link does not imply our endorsement of the site, nor does it imply any association with its operators. Use of any such linked website is at the user’s own risk.