Inflation, Election, and AI…Oh My

After such a strong first quarter for equities, it would have been greedy to expect more upside, but investors got it. Artificial Intelligence and the Fed’s battle with inflation were the dominating themes, both of which contributed to some market imbalances, particularly between Large and Small Cap stocks. In addition, investors are contending with the emotions and implications of an upcoming Presidential election. We tackle it all in this quarter’s Perspectives.

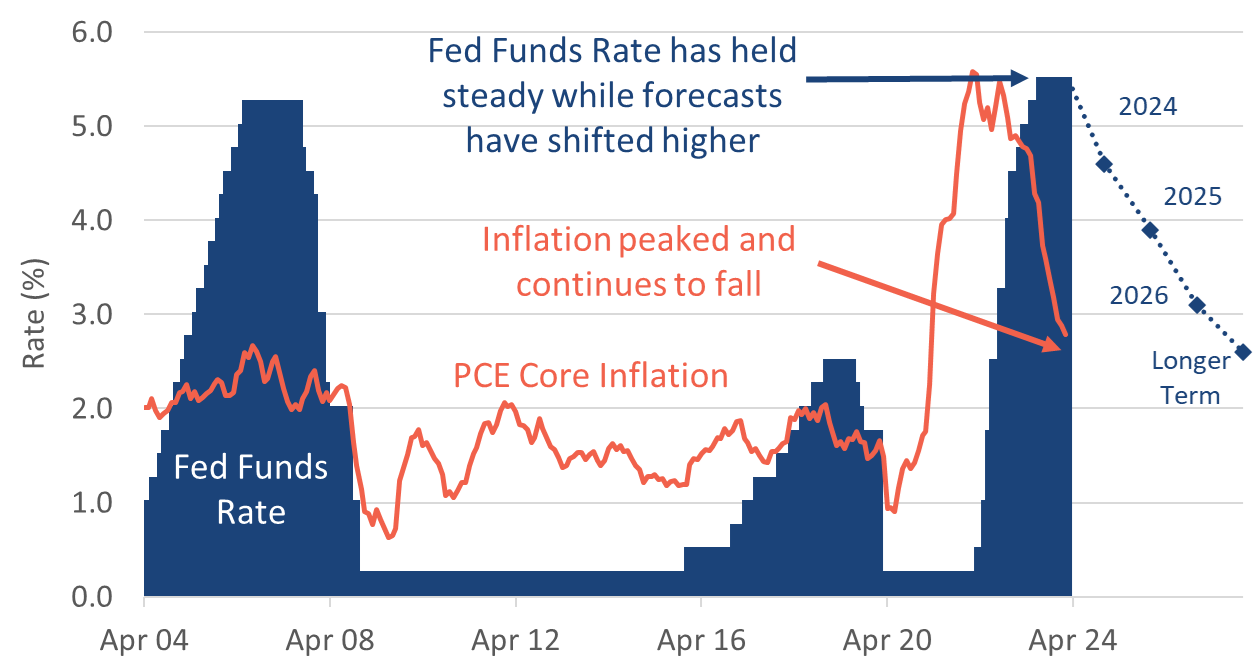

The “higher for longer” scenario is playing out as inflation cools

The Fed’s fight against inflation persists, as rates were once again held at a high level. Inflation resumed its declines in the second quarter, continuing to inch towards the Fed’s target. For many, it has been a slower-than-hoped path to get here, but PCE Core Inflation (a preferred Fed measure) is now at just 2.6%.

Despite the progress on inflation, investors’ expectations for rate cuts continue to fall. Hopes of significant cuts this year have diminished, with one cut now appearing the most likely scenario. That is a far cry from the five plus that were forecast at the beginning of the year.

The higher-for-longer approach has hurt Value and Small-Cap stocks this year. These companies are more reliant on debt funding than cash-rich Mega-Cap stocks. Higher rates have meant more expensive financing.

Chart 1: Rates Cut Expectations Diminished

Source: The US Federal Reserve, Bureau of Economic Analysis

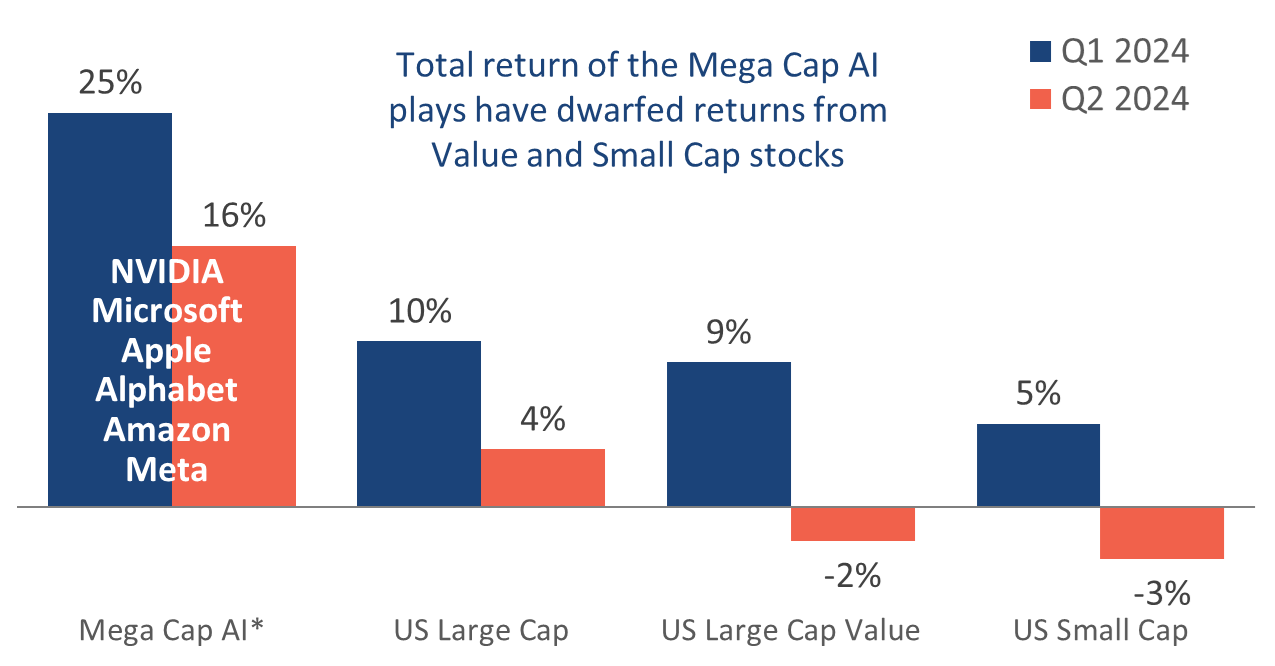

AI drives market returns, but Mega Caps are benefiting more

Rates are not the only thing benefiting large companies over their Value and Small Cap peers. Artificial Intelligence (AI) is driving the wedge between the haves and the have-nots deeper.

Deep-pocketed Mega-Cap stocks, like NVIDIA, Microsoft, and Alphabet, have dominated market performance and are the early AI winners for investors. The top six companies in the S&P 500 represent nearly 30% of the market cap. Concentration risk in market cap-weighted indexes is real, though these companies have shown few signs of weakness for now.

To date, Value and Small-Cap stocks have been left behind in the AI rally. Investors should not write them off, as the adoption of AI could create a productivity revolution beyond the Mega-Cap space. While we do not waste time speculating, it is certainly possible that the next leg of the AI rally comes from a new group of companies that use the technology to increase their productivity and reach.

Our preferred investment approach in the current environment is to overweight the Momentum factor, using funds that invest in trending stocks. This approach has the potential to pick up on changing dynamics in AI leadership.

Chart 2: AI Rising Tide Does Not Lift All Ships

Source: Factset, R1000, R1000V, R2000. *Simple Average

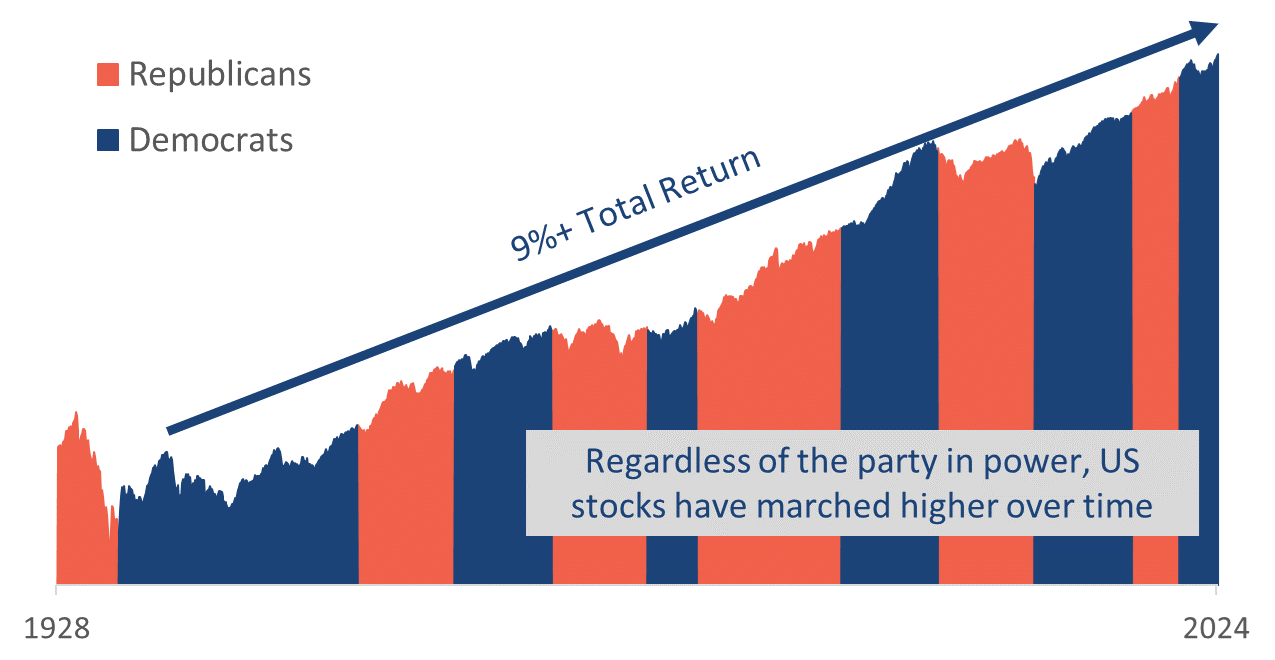

US stocks have advanced irrespective of the administration

Election angst is in full swing. The outcome of the coming election is unknowable, but investors can take comfort in past precedents. As evidence-based investors, we take many of our queues from the past. It is not to say that history will repeat itself, but it rhymes often enough to provide an advantage to students of its lessons.

The world economy and the economic cycle are bigger determinants of stock market returns than those sitting in the White House. Policies can have an impact, but companies are dynamic and find a way to profit across administrative regimes.

An election is a binary uncertain event, which naturally elevates investor nerves. Attempts to predict the market reaction should be avoided. Evidence-based investors know that the future is unknowable, and the best investing action at any point in time is the one based on what we know today and not what we think will happen in the future.

Chart 3: The Economy Drives Investments Not Presidents

Source: Factset, S&P 500 index total return

Source: Factset, S&P 500 index total return

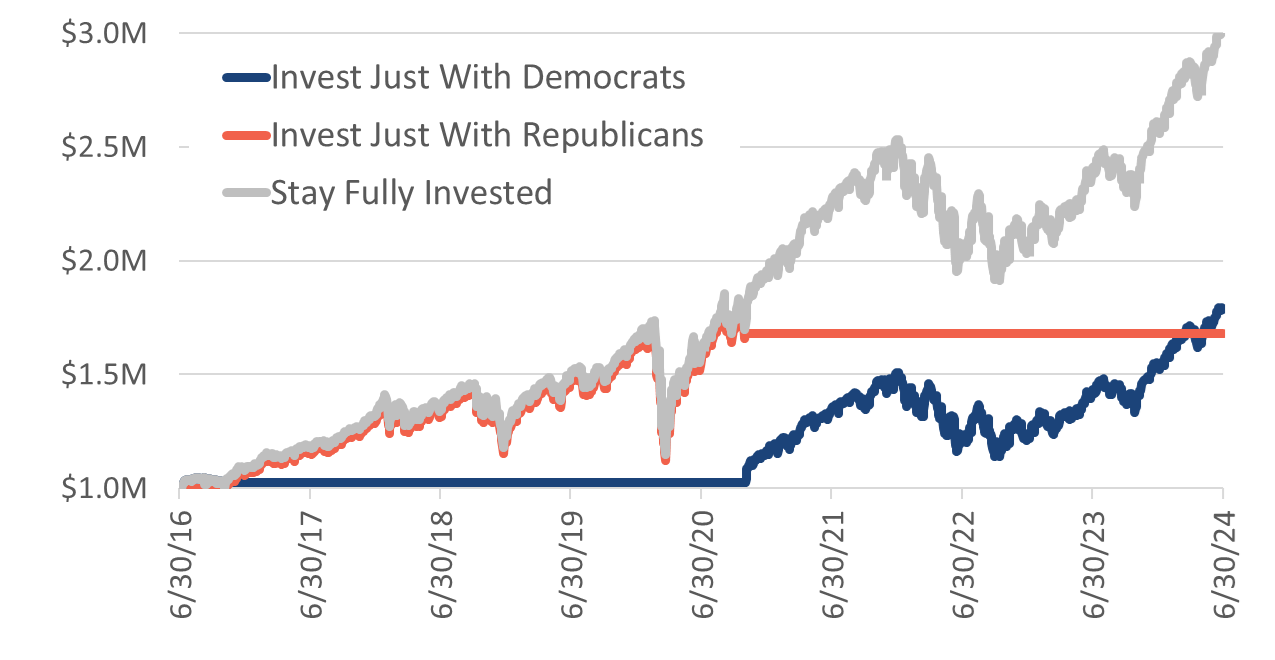

Despite administration differences recently, returns have been similar

We can use the past eight years as a case study. During this time frame, we have seen two very different types of administrations in the White House. Despite the differences between the Obama/Biden administrations and Trump administration, the stock market has found a way to higher ground. Coincidentally, it is up a fairly similar amount during both periods of time.

The chart below shows the perils of letting political concerns get in the way of sound investing decision-making. Investors who stayed invested across administrations faired far better than those who speculated about the impact of politics on stock returns. Historically and recently, investors have been better off disregarding politics and putting their trust in a corporation’s ability to navigate a path to profitability.

Chart 4: It Does Not Pay to Bet on Administrations

Source: Factset, S&P 500 total return

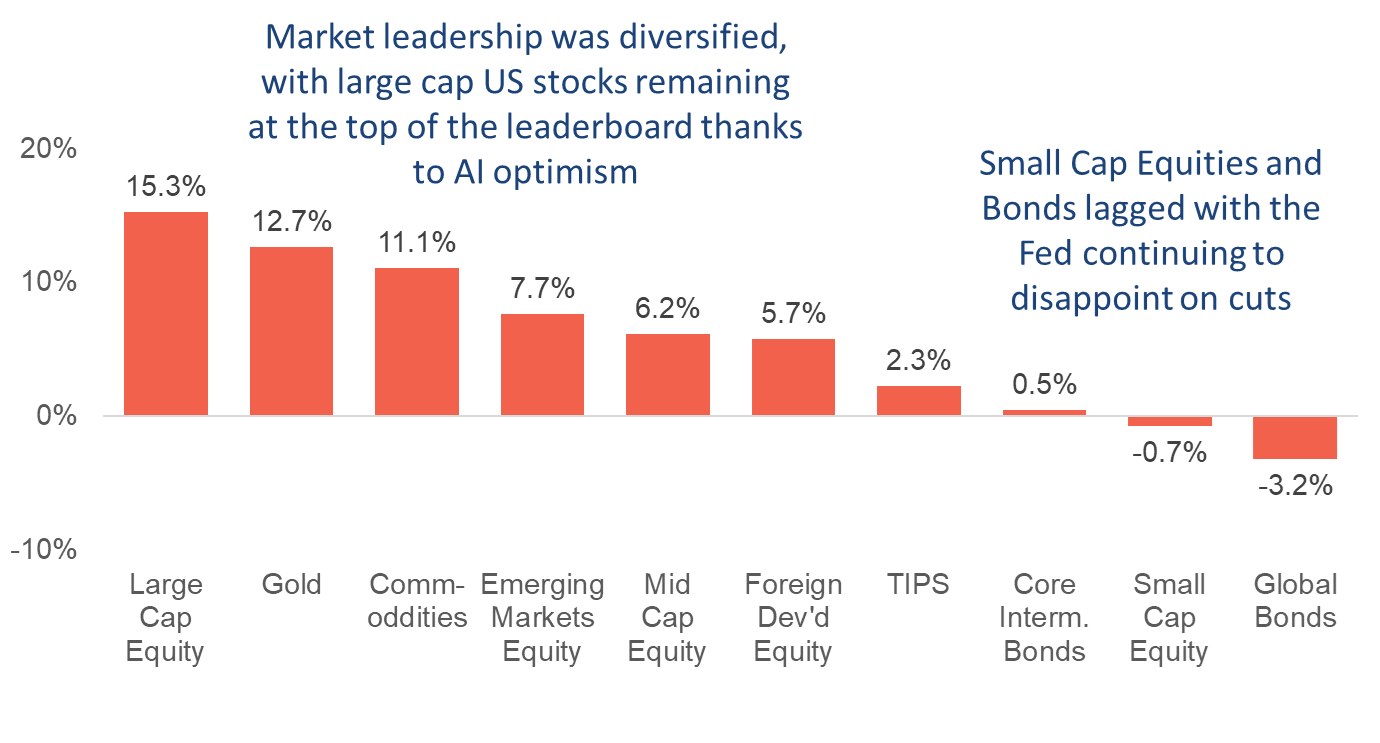

H1 2024 saw diversified market leadership

Diversification paid off, with a wide range of asset types atop the leaderboard. US Large Cap continues to plow ahead, fueled by AI optimism. It has been a while since that has not been the case. However, below the surface, there were new market leaders in the second quarter: Gold and Emerging Markets.

Gold’s strong showing extended into Q2. The precious metal has benefited from a combination of rising uncertainty (it is viewed as a store of value in uncertain times) and global central bank demand. Central banks around the world have been buying gold, in part to reduce their reliance on US dollar reserves.

Fixed income performance stalled as the Fed once again failed to meet market hopes for rate cuts. Small Cap stocks continue to lag their larger peers despite an apparent valuation opportunity. They are facing the combined challenge of high interest rates on their debt as well as not being seen as benefiting from the initial AI optimism.

Chart 5: Asset Class Performance for H1 2024

Source: Factset

“Stop trying to predict the direction of the stock market, the economy, or elections.” – Warren Buffett

As we round the corner to the second half of the year, there is a lot for investors to contend with – the impact of Artificial Intelligence, an election supercharged with emotion, and a Fed that may yet begin the journey towards lower rates. This may feel like a lot, because it is… but at the same time, it is not unusual.

As investors, we face the uncertain impact of these known market themes every day. Worse yet, we face the uncertain impact of the things we don’t yet know about! Remember when we all sauntering blissfully into 2020, oblivious that in a few months the world would literally be shut down? Or remember in late 2022 when we all got our first real taste of AI with the public launch of ChatGPT? Bring on the AI rally!

Whether we are facing an election or the unknown next megatrend, our job as evidence-based investors is not to predict it but to prepare for it. Here is what some of that preparation looks like as we enter the second half of 2024:

- True diversification. AI is creating concentration risk in Mega Cap stocks. US Large Cap stocks look relatively expensive versus the rest of the world. Investors have a tendency to have too much home bias in their portfolios. All of these are reasons that proper diversification is as important as ever. For us, that would include an ample allocation to Small Cap, Emerging Markets, and Developed International, as well as exposure to Gold.

- Smart rebalancing. Investments will go up and down… sometimes by a lot. Within that risk is opportunity, and smart investors have a plan to capitalize on it. For us, it is “opportunistic rebalancing.” We look at portfolios every week for opportunities to sell high and buy low. If you are worried about the election, don’t run to the safety of cash. Instead, have a rebalancing plan that can capitalize on market swings.

- A mental gut check. The worst mistakes investors make are often those driven by emotion and behavioral biases. There are a myriad of pitfalls that investors can fall prey to in 2024. Mindlessly chasing risky AI assets because of FOMO, market-timing out of election fear, and taking on concentration risk due to home bias are just a few. Knowing is half the battle. Being aware of the many behavioral biases that investors can face will prepare you to make the right decisions when emotional pressure mounts.

Election years can be emotionally taxing, and gauging the impact of megatrends, like AI, can be daunting. We are here to help and partner with our clients so they can navigate the inevitable uncertainty with confidence. On behalf of the team here at Strategic, I thank our clients, friends, and family members for placing their trust in us. We truly appreciate having you as part of our Strategic Community.

About Strategic

Founded in 1979, Strategic is a leading investment and wealth management firm managing and advising on total client assets of over $3 billion, as of 6/3/26.

Disclosures

Strategic Financial Services, Inc. is registered with the Securities and Exchange Commission (SEC) as an Investment Advisor. The term “registered” signifies compliance with regulatory requirements and does not imply a certain level of skill or training.

The information provided on our website, including weekly market commentaries, financial planning articles, and other educational resources, is intended solely for educational purposes. It is designed to offer insights into financial planning and investment management, aiming to enhance understanding of financial concepts, strategies, and market trends. This content should not be interpreted as personalized investment advice or a recommendation for any specific strategy, financial planning approach, or investment product. Financial decisions are deeply personal and should be made considering the individual’s specific circumstances, goals, and risk tolerance. We recommend consulting with a professional financial advisor for personalized advice.

Please be aware that Strategic Financial Services, Inc. does not provide legal or tax advice. The content on this website is not intended to be used as such or as a substitute for legal or tax advice from a licensed professional. We advise seeking guidance from qualified legal and tax advisors regarding these matters.

Investment Risks and Portfolio Management.

The discussion of any investments on this website is for illustrative purposes only and provides no guarantee that the advisor will make any investments with the same or similar characteristics as those presented. The investments identified and described herein do not represent all the investments purchased or sold for client accounts. The selection of representative investments to discuss is based on various factors, including recent company news or earnings releases.

It should not be assumed that any investments discussed were or will be profitable. All investments involve risk, including the potential loss of principal. There is no assurance that investments mentioned will remain in client accounts at the time you view this information.

When index returns are mentioned on this site, they are provided as a general indicator of market conditions and are not representative of any client’s portfolio performance. Indices are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. Therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

While index returns are used as a framework to report on general market conditions, they should not be construed as an indicator of future performance of any specific investment or portfolio. Discussion of index returns is intended to provide context and insight, not to suggest that clients will achieve similar results. Each client’s portfolio is managed according to their specific investment goals and financial situation.

The opinions and any forward-looking statements expressed in the articles and videos featured in our resource center are as of the date of publication. These statements are based on current laws, regulations, market conditions, and other relevant factors, including third-party data. Given the dynamic nature of financial and regulatory environments, as well as potential changes in market conditions or economic circumstances, the information provided may become outdated or may no longer be accurate.

We rely on third-party data to form our opinions and projections, which means that these are subject to the same uncertainties that affect all data-dependent analyses. As such, we advise readers to exercise caution and not rely solely on the statements made herein for making financial decisions. It is recommended that investors consult with a professional advisor who can help assess the relevance and accuracy of the content in light of the current economic climate and personal financial situation.

Our website contains links to third-party websites as a convenience to our users. Strategic Financial Services, Inc. does not control, endorse, or guarantee the content found on such sites. We are not responsible for the accuracy, legality, or content of the external site or for that of subsequent links.

Contact the external site for answers to questions regarding its content.

The inclusion of any link does not imply our endorsement of the site, nor does it imply any association with its operators. Use of any such linked website is at the user’s own risk.