Investing in the Unknown With Confidence

After 2022, investors deserved a break, and they got it. We entered last year with optimism, and it was well-founded. We had no crystal ball, only the knowledge that both equities and bonds went on sale in 2022, increasing the probability of better times to come. Patient investors who stayed the course were rewarded in 2023.

The Federal Reserve was a big player last year, taming inflation without crushing economic activity (at least yet). That dynamic will not change this year. The equity markets are pricing in a very rosy, soft-landing scenario, so there is little room for error as we wait to see if any lagged effects of higher interest rates are yet to be felt.

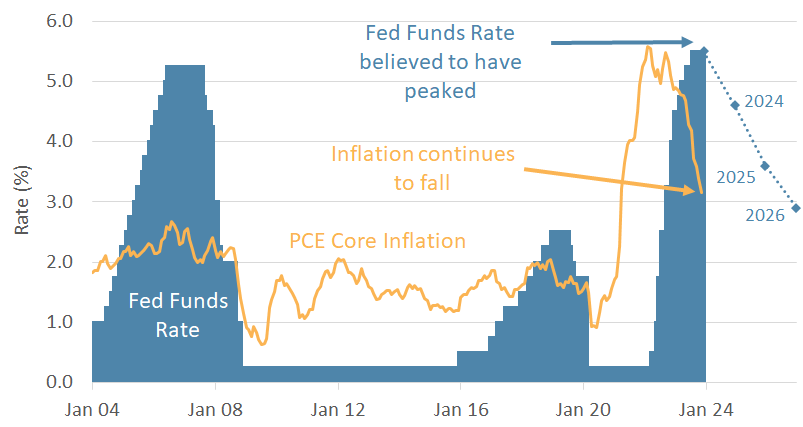

The Fed is signaling that we are at peak rates

The Federal Reserve’s eye remained focused on taming inflation, and progress continued. Inflation dropped quickly as the Fed held rates steady at a historically high level. PCE Core Inflation (a preferred Fed measure) approached but did not quite fall below 3%. It will presumably be a psychological victory to see the inflation number begin with a “2” again.

The Fed did not need to tighten further in Q4 to achieve the decline in inflation. Instead, it monitored the delayed impact of the monetary restrictions it has put on the economy. While the messaging has been “higher for longer,” Fed officials are forecasting rate cuts in 2024, 2025, and 2026, and equity markets appear to have started to price in the optimism of those projected moves.

Chart 1: Rates Held Steady and Forecasts Fell

Source: The US Federal Reserve, Bureau of Economic Analysis

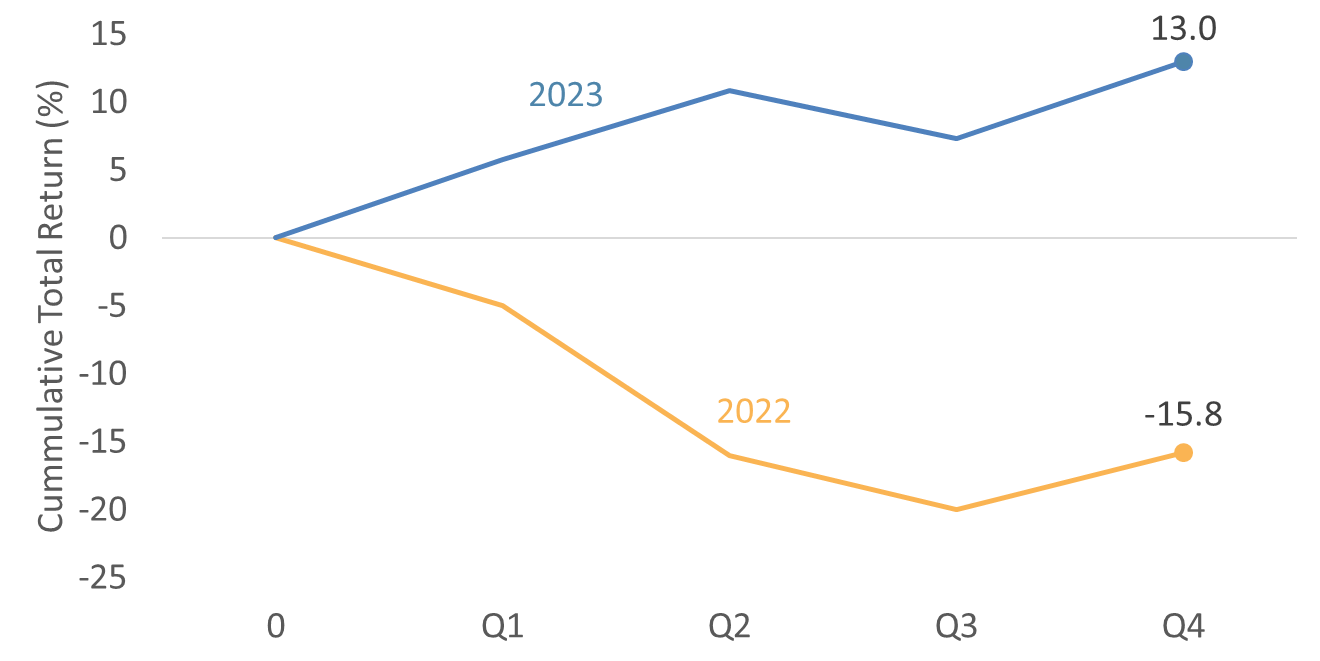

The diversified portfolio bounced back in 2023

Declining equities and fixed income in 2022 caused many to question the value of diversification. Along those lines, there was much talk about the demise of the “60/40” portfolio (a mix of 60% stocks and 40% bonds, which has been a bellwether allocation for many decades). The legendary “60/40” portfolio had a tough 2022, falling 15.8% as correlations between equities and bonds were high. If equities and bonds fall in unison, is diversification broken or at least flawed?

The answer is “no.” The rebound in returns in 2023 rewarded patient investors, with the 60/40 portfolio rising around 13% on the year. One bad year does not make a trend. Investors should stay focused on the long term and not fall victim to recency bias. While we do not advocate a simple 60/40 portfolio specifically, the point is that diversification benefits provide one of the few free lunches in investing and remain an important risk management tool. Diversification will not always work in the short run but is proven to benefit risk-adjusted returns in the long run.

Chart 2: Reports of the 60/40 Demise Were Premature

Source: Factset. 60% S&P500 (VOO), 40% US Agg (AGG) rebalanced quarterly

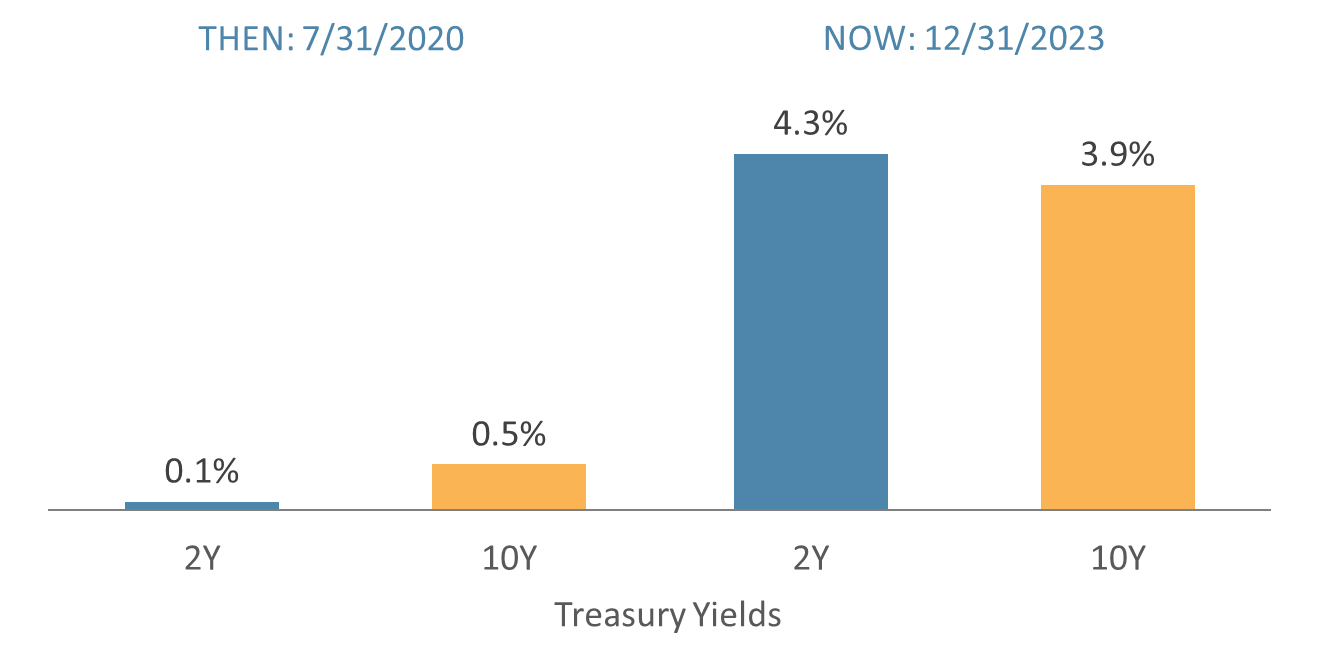

Bonds enter the new year with an elevated margin of safety

Diving into the diversified portfolio, we first look at the Protection side of the portfolio, specifically fixed income (bonds). At the heart of the pandemic, bond yields offered little to investors. Now, there are materially positive yields providing opportunities for investors. The yield curve remains inverted (as it was last year), with the 2-year Treasury (4.3%) yielding more than the 10-year (3.9%). But investors should be careful about chasing yield.

We continue to caution investors not to get sucked in by the Fed’s teaser rates at the short end of the curve. Money markets and CDs offer more yield than longer-term Treasuries, like the 10-year. But we think about investments in terms of “total return” not just yield. We see better risk-reward at the long end of the curve. Attractive short-term rates can vanish quickly, while longer-term rates can have more potential to benefit if and when rates begin to fall.

Chart 3: Treasury Yields Remain Elevated and offer opportunity

Source: Factset

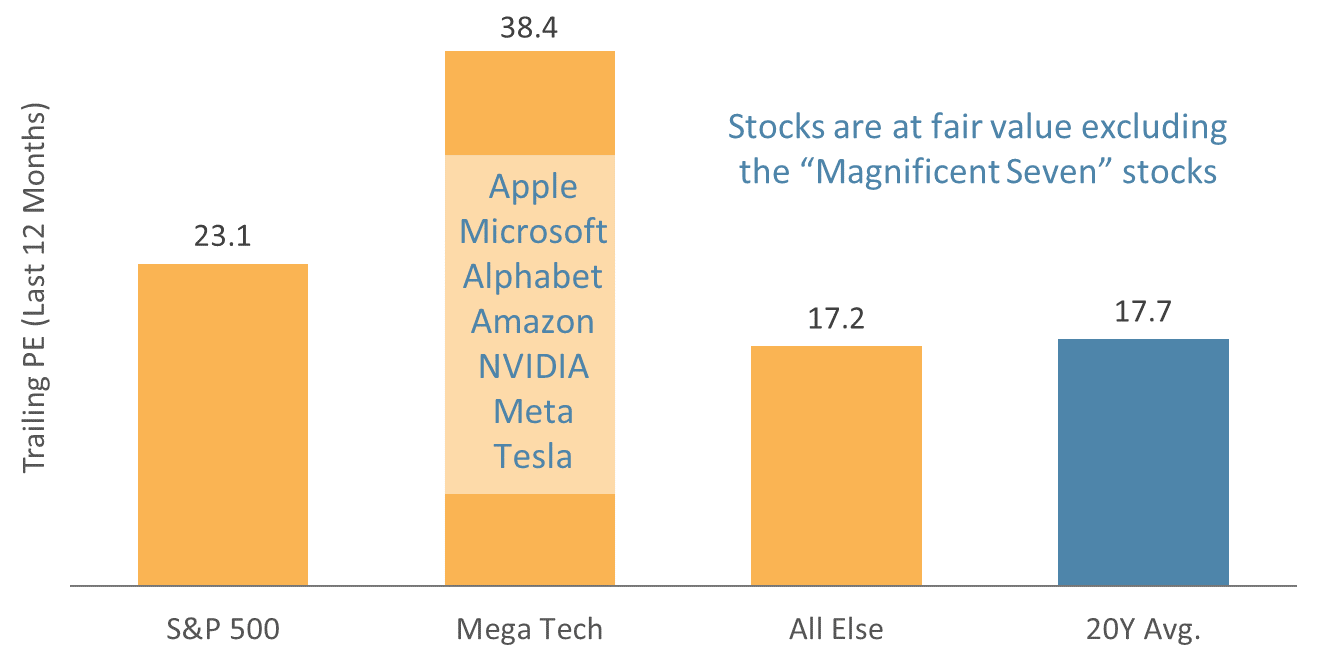

The stock market is forward-looking, and much good news is priced in

The stock rally of 2023 drove up equity valuations. It is worth remembering that the stock market is always forward-looking, meaning investors as a collective are buying and selling based on their expectations for the future. In this light, investors have a rosy view of the future. That rose-tinted vision of the future likely includes a drop in interest rates that the Fed has telegraphed and perhaps a soft landing.

As a result of this optimistic view, the S&P 500 ended the year on the expensive side, with a 12-month trailing PE of 23.1x, compared to the 20-year average of 17.7x. Digging into this number, we find that the “magnificent seven” (Apple, Microsoft, Alphabet, NVIDIA, Amazon, Meta, Tesla) drove much of the elevated valuation, with a combined PE of 38.4x. Excluding these seven, the rest of the market is roughly in line with the long-term valuation of the market.

Does this analysis mean investors should avoid equities? Absolutely not. Trying to time the market is a dangerous game. “Expensive” markets can rally for years. Instead, we recommend avoiding over-concentration in the magnificent seven and the US in general. In other words, diversification is as important as ever.

Chart 4: Stocks End the Year Pricing in a Rosy Future

Source: Factset

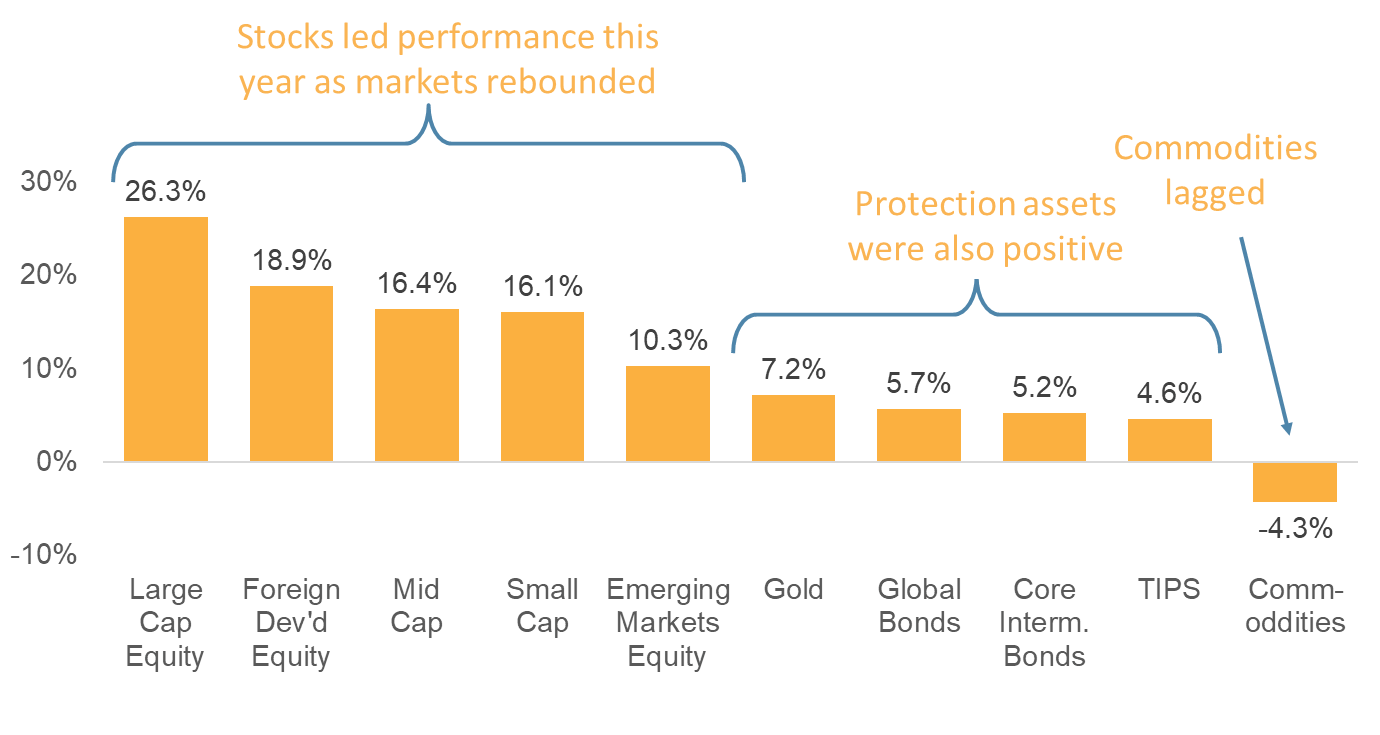

2023 was strong across most asset classes

We have discussed the strength in US equities, and a look across a broader selection of assets shows widespread strength. US Large Cap remains atop the leaderboard, while Foreign Developed also put in a solid performance.

Even “Protection” assets, like fixed income and gold, performed well. As we discussed, in 2022, investors felt the pain of highly correlated declines in fixed income and equities. In 2023, patient investors benefited during the rebound as correlations remained positive.

Commodities, which had performed so well as inflation raged, pulled back in 2023, dragged down, in part, by declining oil prices.

Chart 5: Asset Class Performance for 2023

Source: Factset

“Prediction is very difficult, especially if it’s about the future!” – Yogi Berra

In many ways, 2023 had its challenges. But for most investors, it was sweet redemption after a difficult 2022. Those who stayed the course despite the previous year’s challenges were rewarded. Those who wavered and let emotion drive their portfolios may not have been so fortunate.

As we look forward, will the new year bring continued fortune, or will the market boomerang once again? Will investors be pleased with the pace of Fed interest rate declines or disappointed by slower-than-expected cuts? Will the Fed nail the economic landing or come in too hard? What impact will the Presidential election have on markets? This is the time of year investment professionals put out their predictions for the coming year. But as Yogi Berra said, “Prediction is very difficult, especially if it’s about the future!”

As evidence-based investors, we will not give in to the urge to predict the unpredictable. Instead, we focus on the facts before us to guide our playbook for the coming year. Here is what we are seeing:

- Within equities, valuations are elevated. But history shows stocks can defy valuation gravity for extended periods. So rather than going underweight the asset class, we are neutral with a focus on specific opportunities (discussed below).

- We are generally overweight in Value and Momentum. Value is historically cheap relative to Growth and can benefit from a falling rate environment. Momentum is the most persistent of the factors and has the potential to pivot should market leadership change.

- Diversification within equities is as important as ever. Concentration risk within the “magnificent seven” as well as “home bias” has many investors over-reliant on the fortunes of just a few companies. We remain diversified across both market capitalization (large and small) and geographies (developed international and emerging markets).

- We have begun tilting our fixed income exposure toward Long-Term Treasuries. Investors have been attracted to short-term vehicles like money-market funds and CDs, which are paying the highest rates in some time. But those rates can be fleeting, and we remind investors it is a good time to take advantage of the attractive rates in longer-duration bonds, which have the potential to benefit significantly should rates fall.

A quick election pep talk

While we tend to avoid pointless predictions, we do predict with high confidence that investor angst will rise as we approach the Presidential election this year. Keep your nerve. Do not let emotion drive your investment decisions. As contentious as Presidential elections can get, history shows the stock market is less influenced by the winning party than you may think. Investors enjoyed handsome stock returns under the Obama, Trump, and Biden administrations. There is no certainty in investing, but investors who follow the evidence and hold their nerve over the long run can have swagger entering the unknown. They can have confidence that they have done what they can to give themselves a better chance to reap the benefits markets offer over time.

On behalf of the team here at Strategic, I thank our clients, friends, and family members for their trust in us on this investing journey. We are proud of our Strategic community and look forward to serving you in the year ahead.

About Strategic

Founded in 1979, Strategic is a leading investment and wealth management firm managing and advising on total client assets of over $3 billion, as of 6/3/26.

Disclosures

Strategic Financial Services, Inc. is registered with the Securities and Exchange Commission (SEC) as an Investment Advisor. The term “registered” signifies compliance with regulatory requirements and does not imply a certain level of skill or training.

The information provided on our website, including weekly market commentaries, financial planning articles, and other educational resources, is intended solely for educational purposes. It is designed to offer insights into financial planning and investment management, aiming to enhance understanding of financial concepts, strategies, and market trends. This content should not be interpreted as personalized investment advice or a recommendation for any specific strategy, financial planning approach, or investment product. Financial decisions are deeply personal and should be made considering the individual’s specific circumstances, goals, and risk tolerance. We recommend consulting with a professional financial advisor for personalized advice.

Please be aware that Strategic Financial Services, Inc. does not provide legal or tax advice. The content on this website is not intended to be used as such or as a substitute for legal or tax advice from a licensed professional. We advise seeking guidance from qualified legal and tax advisors regarding these matters.

Investment Risks and Portfolio Management.

The discussion of any investments on this website is for illustrative purposes only and provides no guarantee that the advisor will make any investments with the same or similar characteristics as those presented. The investments identified and described herein do not represent all the investments purchased or sold for client accounts. The selection of representative investments to discuss is based on various factors, including recent company news or earnings releases.

It should not be assumed that any investments discussed were or will be profitable. All investments involve risk, including the potential loss of principal. There is no assurance that investments mentioned will remain in client accounts at the time you view this information.

When index returns are mentioned on this site, they are provided as a general indicator of market conditions and are not representative of any client’s portfolio performance. Indices are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. Therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

While index returns are used as a framework to report on general market conditions, they should not be construed as an indicator of future performance of any specific investment or portfolio. Discussion of index returns is intended to provide context and insight, not to suggest that clients will achieve similar results. Each client’s portfolio is managed according to their specific investment goals and financial situation.

The opinions and any forward-looking statements expressed in the articles and videos featured in our resource center are as of the date of publication. These statements are based on current laws, regulations, market conditions, and other relevant factors, including third-party data. Given the dynamic nature of financial and regulatory environments, as well as potential changes in market conditions or economic circumstances, the information provided may become outdated or may no longer be accurate.

We rely on third-party data to form our opinions and projections, which means that these are subject to the same uncertainties that affect all data-dependent analyses. As such, we advise readers to exercise caution and not rely solely on the statements made herein for making financial decisions. It is recommended that investors consult with a professional advisor who can help assess the relevance and accuracy of the content in light of the current economic climate and personal financial situation.

Our website contains links to third-party websites as a convenience to our users. Strategic Financial Services, Inc. does not control, endorse, or guarantee the content found on such sites. We are not responsible for the accuracy, legality, or content of the external site or for that of subsequent links.

Contact the external site for answers to questions regarding its content.

The inclusion of any link does not imply our endorsement of the site, nor does it imply any association with its operators. Use of any such linked website is at the user’s own risk.