Finding Peace of Mind in Worrying Times

Contributed by Doug Walters, Max Berkovich, David Lemire

The wall of worry grew in Q1 with “inversion” and “inflation” the buzzwords for investors and the financial media. Despite many stocks and bonds producing negative returns this quarter, there is room for optimism. In this quarter’s perspectives, we discuss how inversion could have near-term positives, inflation is coming from a position of strength, and the ever-present wall of worry is not all it is cracked up to be.

A Quarter of Reckoning for Growth

The high valuations of growth stocks finally met their match in Q1… The Fed. With inflation in its crosshairs, The Fed has started raising rates, which has disproportionately hit growth (aka expensive) stocks. The quarter provided a good reminder of the importance of having diversification even within equities.

- Growth stocks underperformed value by over eight percentage points. Rising interest rates generate a stronger headwind for growth stocks, given their reliance on future profitability.

- Value is a proven factor that has been persistent in its ability to outperform over long periods of time. But there are other persistent factors like quality, value, momentum, and small size.

- A well-diversified portfolio should capture the advantages of each of these and avoid the allure of pure growth.

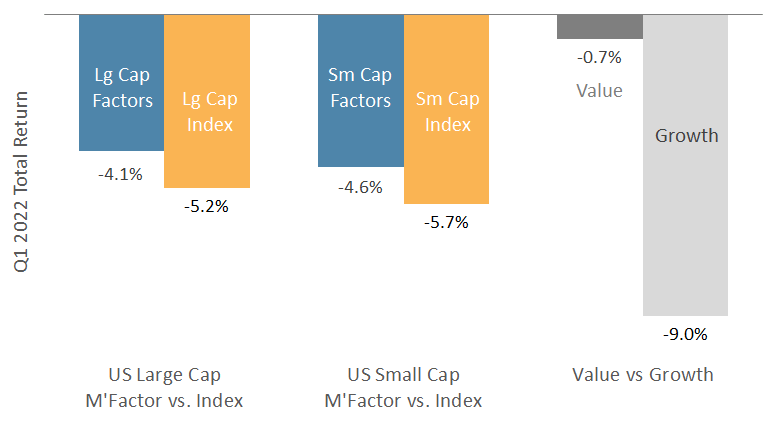

chart 1: persistent factors outperformed in q1 2022

Multifactor funds outperformed the broader market thanks to outperformance from value stocks.

Investors Contend With Yield Curve Inversion

The Treasury yield curve inverted, prompting headlines of an impending recession. Inversion occurs when shorter-dated treasuries, like the 2-year, have higher yields than longer-dated treasuries, like the 10-year. There is an ominous history of these inversions preceding a recession. But…

- Past inversions have not been a helpful timing mechanism for shifting out of equities.

- Over the past 25 years, the median time between inversion and the US stock market (S&P 500) peak is 20 months.

- The median total return of the US stock market from inversion to market peak is 29%.

Marketing timing based on inversion (or any other signal) is risky business. A better approach is to have a portfolio that is prepared to weather the ups and downs of the market and not one whose success is dependent on predicting short-term moves.

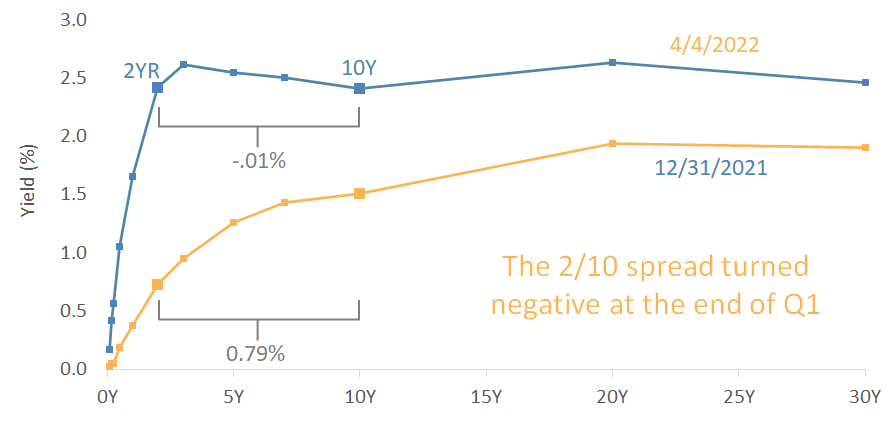

Chart 2: Treasury yield curve inversion

The 2/10 yield spread turned negative in Q1, prompting premature calls of an impending recession.

The Wall of Worry Persists

Investors are currently facing a growing wall of worry. But this is nothing unusual, and the stock market has a historical tendency to climb the wall of worry. This behavior was never more evident than in the pandemic, where stocks flourished against all odds. Will the current wall be scaled once again?

- In the short term, the answer to this question is unknowable.

- But we know that, historically, companies have adjusted to adversity and provided patient investors with attractive long-term returns.

- The savvy investor stays invested and takes advantage of any opportunities that volatility provides.

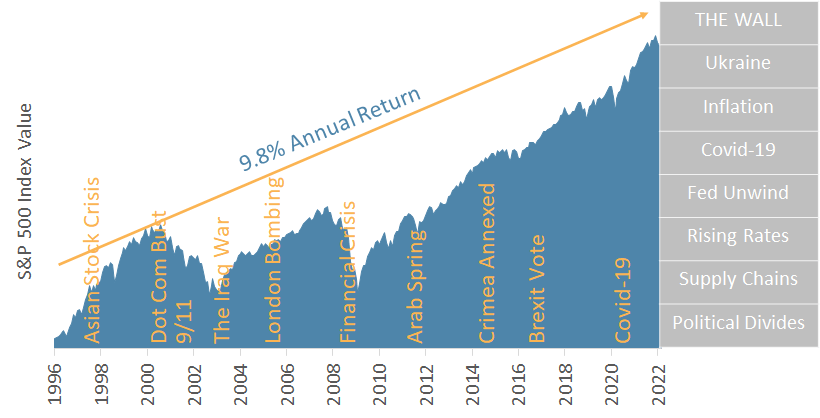

Chart 3: Climbing the wall of worry

Stocks have a long history of successfully climbing the wall of worry.

Another Angle on Inflation

Inflation was tangible in Q1, both in the media and our lives. Given the ever-present wall of worry and the pain at the pump, it is easy to conclude that inflation is driven entirely by pandemic supply chain issues and the Ukraine war. But this would be wrong. In many ways, the US economy is very strong, and this is also contributing to inflation. For example:

- Wages are growing at the fastest pace in nearly 40 years,

- Retail sales are stronger than in the tech bubble, and

- Unemployment is just 3.6%.

We hear concerns about stagflation (high inflation, low growth), but the primary concern now is overheating. That is why The Fed is taking its foot off the gas with higher rates and fewer asset purchases and is signaling it will hit the brakes in Q2. All eyes are watching The Fed to see if they get the balancing act right.

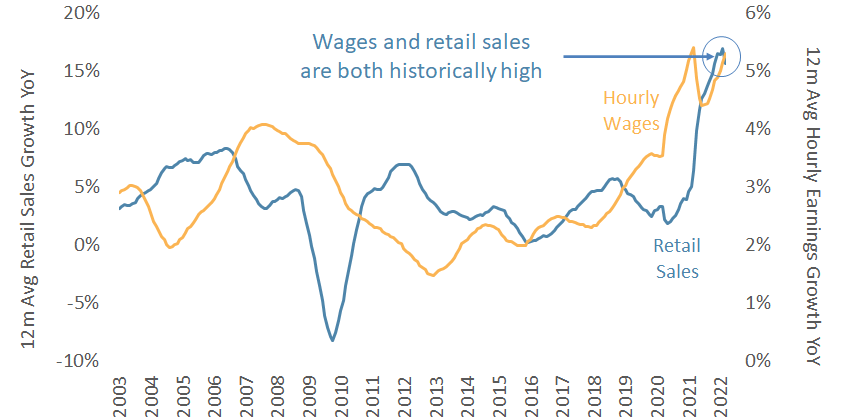

Chart 4: Inflation from a Position of Strength

Inflation is driven in part by a US economy that is very strong in many ways.

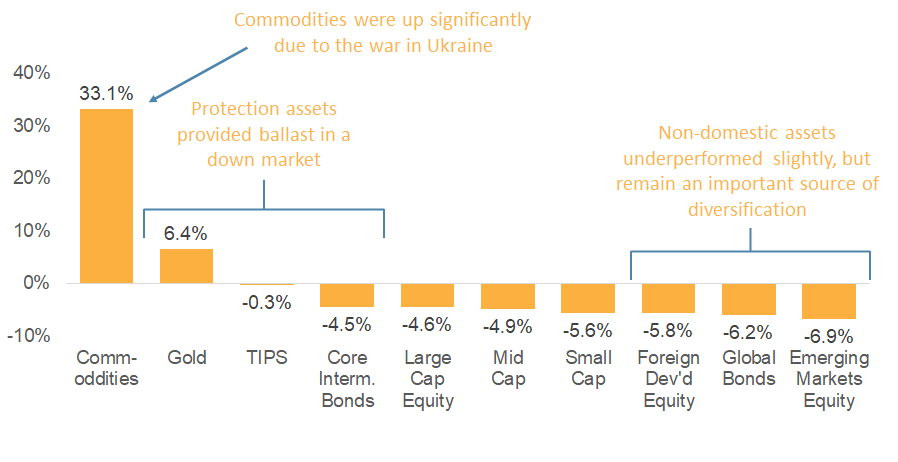

Gold Providing Ballast to Equity Weakness

Before we move on to Q2, we take a look at how various assets have performed thus far this year. Most risk assets slipped in Q1. The “protection” assets within the portfolio (bonds, gold) fared somewhat better, providing important ballast.

- Equities fell across the board. Even core bonds ended up in negative territory.

- Gold proved once again (as it did in 2020) to be a good store of value in a challenging equity environment. That is why we classify gold as “protection” even though, in isolation, it can be quite volatile.

- Commodities spiked as the war in Ukraine exasperated the pandemic supply chain challenges.

- Non-domestic assets underperformed but are a critical ingredient of a well-diversified portfolio that avoids home bias.

Chart 5: Q1 2022 Asset Class Performance

Equities slide across the board in Q1, while gold shines.

As we head into the second quarter and beyond, all eyes are on The Federal Reserve. Current indications are that they will be increasing the pace of rate increases and dwindling their balance sheet. They are walking a tightrope, trying to reign in inflation while not damaging a US economy that is currently firing on all cylinders. Fed tightening is undoubtedly a headwind for equities, particularly expensive growth stocks.

While all of this seems predetermined, the future is unknowable. A new discovery or disaster could change what we think we “know” in an instant. None of us predicted a pandemic, and indeed, none predicted there would be stellar stock returns during a pandemic. We could have predicted that, over time, companies find a way to adapt to the circumstances and provide investors with attractive long-term returns. So should investors simply own the whole market? Set it and forget it? There is a better, evidence-based approach:

- Diversify. It is the one free lunch in finance. Intelligent diversification ensures you do not have all of your eggs in one basket and can dramatically improve risk-adjusted returns. In Europe and Emerging Markets, turmoil may have investors on edge about owning these regions. But they provide essential diversification and, given recent weakness, may be poised for a bounce. Diversification is the best way to weather market volatility.

- Seek persistent factors. You do not need to own the whole market when certain market factors have persistently outperformed. We prefer quality, value, momentum, and size and recommend holding them at the core of your portfolio.

- Opportunistically rebalance. The best way to take advantage of your diversified portfolio is to give your assets room to drift and regularly monitor for opportunities to sell high and buy low. Rebalancing once a quarter is okay, but it will not capture the full potential of a truly well-diversified portfolio.

If you are looking, you can always find much to worry about in this world, but your investments should not be one of them. Our sole purpose is to help our clients live a great life. We believe in taking the worry out of investing so that your mind is freed to focus on what matters most to you. With portfolio peace of mind, what goals and passions will you pursue in 2022?

About Strategic

Founded in 1979, Strategic is a leading investment and wealth management firm managing and advising on total client assets of over $2 billion.

Disclosures

Strategic Financial Services, Inc. is registered with the Securities and Exchange Commission (SEC) as an Investment Advisor. The term “registered” signifies compliance with regulatory requirements and does not imply a certain level of skill or training.

The information provided on our website, including weekly market commentaries, financial planning articles, and other educational resources, is intended solely for educational purposes. It is designed to offer insights into financial planning and investment management, aiming to enhance understanding of financial concepts, strategies, and market trends. This content should not be interpreted as personalized investment advice or a recommendation for any specific strategy, financial planning approach, or investment product. Financial decisions are deeply personal and should be made considering the individual’s specific circumstances, goals, and risk tolerance. We recommend consulting with a professional financial advisor for personalized advice.

Please be aware that Strategic Financial Services, Inc. does not provide legal or tax advice. The content on this website is not intended to be used as such or as a substitute for legal or tax advice from a licensed professional. We advise seeking guidance from qualified legal and tax advisors regarding these matters.

Investment Risks and Portfolio Management.

The discussion of any investments on this website is for illustrative purposes only and provides no guarantee that the advisor will make any investments with the same or similar characteristics as those presented. The investments identified and described herein do not represent all the investments purchased or sold for client accounts. The selection of representative investments to discuss is based on various factors, including recent company news or earnings releases.

It should not be assumed that any investments discussed were or will be profitable. All investments involve risk, including the potential loss of principal. There is no assurance that investments mentioned will remain in client accounts at the time you view this information.

When index returns are mentioned on this site, they are provided as a general indicator of market conditions and are not representative of any client’s portfolio performance. Indices are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. Therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

While index returns are used as a framework to report on general market conditions, they should not be construed as an indicator of future performance of any specific investment or portfolio. Discussion of index returns is intended to provide context and insight, not to suggest that clients will achieve similar results. Each client’s portfolio is managed according to their specific investment goals and financial situation.

The opinions and any forward-looking statements expressed in the articles and videos featured in our resource center are as of the date of publication. These statements are based on current laws, regulations, market conditions, and other relevant factors, including third-party data. Given the dynamic nature of financial and regulatory environments, as well as potential changes in market conditions or economic circumstances, the information provided may become outdated or may no longer be accurate.

We rely on third-party data to form our opinions and projections, which means that these are subject to the same uncertainties that affect all data-dependent analyses. As such, we advise readers to exercise caution and not rely solely on the statements made herein for making financial decisions. It is recommended that investors consult with a professional advisor who can help assess the relevance and accuracy of the content in light of the current economic climate and personal financial situation.

Our website contains links to third-party websites as a convenience to our users. Strategic Financial Services, Inc. does not control, endorse, or guarantee the content found on such sites. We are not responsible for the accuracy, legality, or content of the external site or for that of subsequent links.

Contact the external site for answers to questions regarding its content.

The inclusion of any link does not imply our endorsement of the site, nor does it imply any association with its operators. Use of any such linked website is at the user’s own risk.