Knowing When to Be Greedy

The uncertainty that we entered the year with did not abate as investors and the Federal Reserve awaited details on tariffs. It was a quarter tailor made for the diversified portfolio and an important reminder to investors of this basic, but often ignored, tenant of investing. Diversification is easy to dismiss, particularly when your home market has an extended stretch of outperformance. But moments like these were built for a well-constructed portfolio.

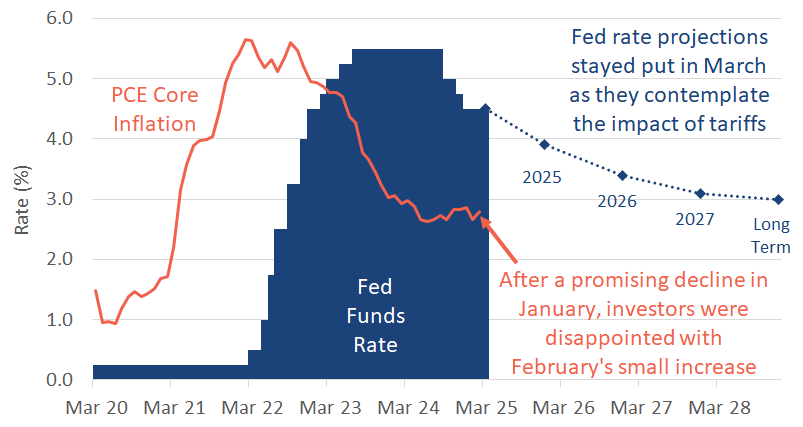

The Federal Reserve remains in “wait and see” mode

The Fed left rates on hold once again as it grapples with sticky inflation and the uncertainty of the tariff strategy. The Fed wants to see continued progress toward 2% inflation in order to justify additional rate cuts.

While PCE Core Inflation (a preferred Fed measure) dipped in January to 2.7%, it disappointed in February, popping back up to 2.8%. That may not seem like a large increase, but it is less the magnitude and more the direction that is of concern to the Fed. The rise is particularly concerning for the Fed as they know that rising tariffs, tightened immigration and tax relief, all have the potential to stoke inflation.

Rate cuts are still forecast for 2025, but, as always, it will be data dependent.

Chart 1: Inflation disappoints

Source: The US Federal Reserve, Bureau of Economic Analysis

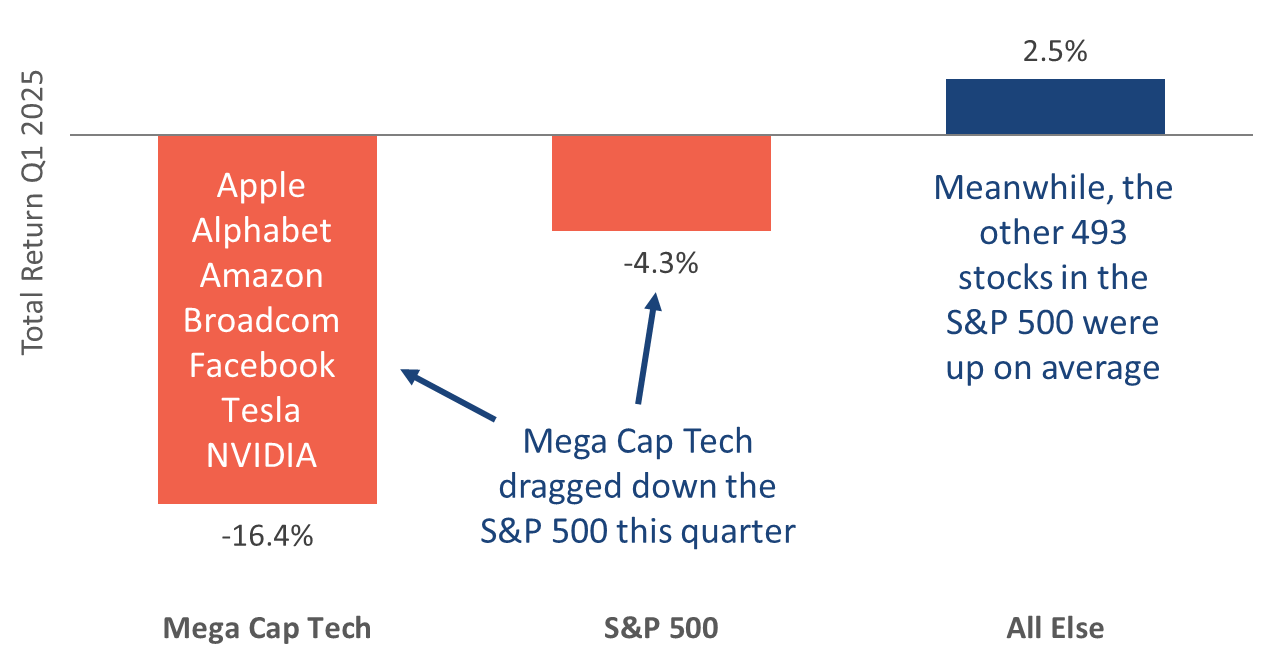

Large tech stocks dragged down the S&P 500

Lofty expectations caught up with the mega caps this quarter in a broad sell off of the recent market leaders. Tesla fell the hardest, but Apple, Alphabet, Amazon, Broadcom, and NVIDIA all posted double-digit declines. The remaining 493 stocks in the index were up 2.5% on average but could not offset the declines of the seven mega cap stocks.

The weakness came as uncertainty about the future path of inflation continued to escalate throughout the quarter. Elevated inflation makes it harder for the Fed to cut rates which is disappointing to investors in US stocks who were looking forward to more stimulative (lower) rates.

We’ve been talking for some time about the concentration risk building in market cap weighted indices like the S&P 500. In the first quarter, we saw the first real signs of that risk being realized.

Chart 2: Mega cap tech falters

Source: Factset, S&P 500 index total return

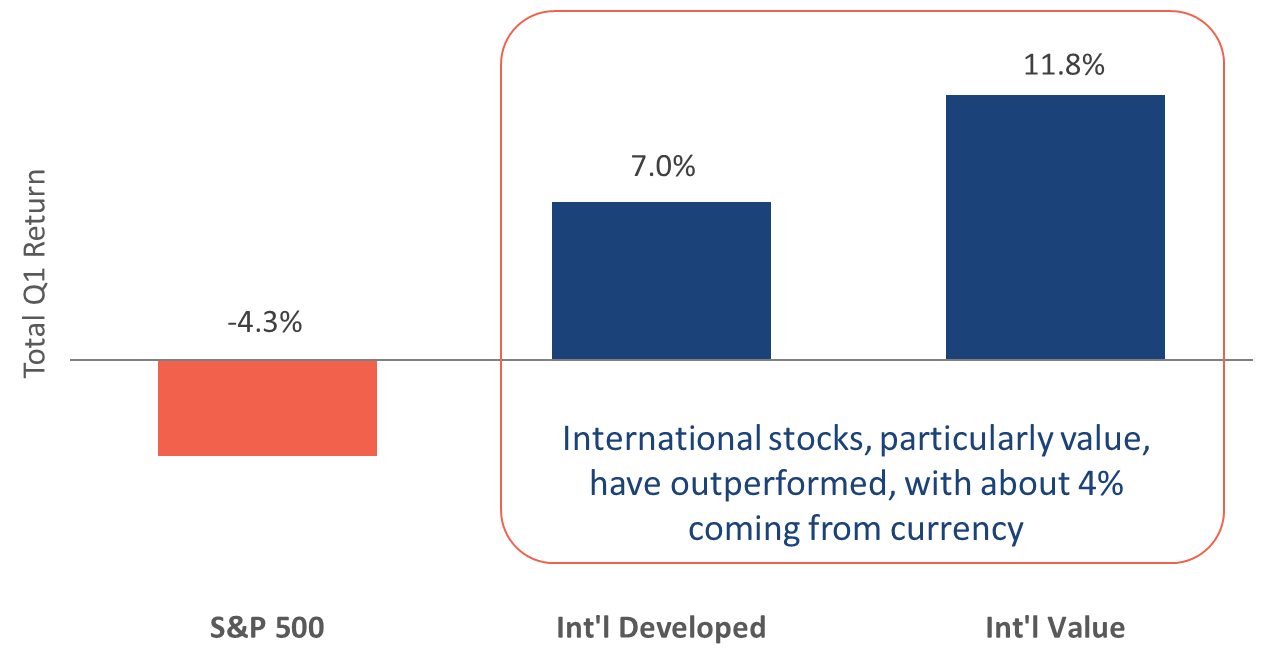

The decline in US stocks was not matched in overseas markets

Well-diversified portfolios that avoided too much home bias benefited from a strong first quarter performance in international stocks. Developed markets rose as investors shifted to regions with lower valuations. In addition, investors celebrated countries like Germany that are looking to boost their economies through increased debt-funded spending.

Even better performance was seen in international value stocks, which were up double digits for largely the same reasons.

While emerging markets stocks ended higher on the quarter, they did not surpass the returns of their developed counterparts. That was in part due to currency differences. About 4% of the developed international outperformance was due to US dollar weakness. Emerging economies tend to be more exposed to the dollar, so our holdings in that space did not enjoy that benefit.

Chart 3: Geographic diversification rewarded

Source: Factset, S&P 500 index, MSCI EAFE, MSCI EAFE Value

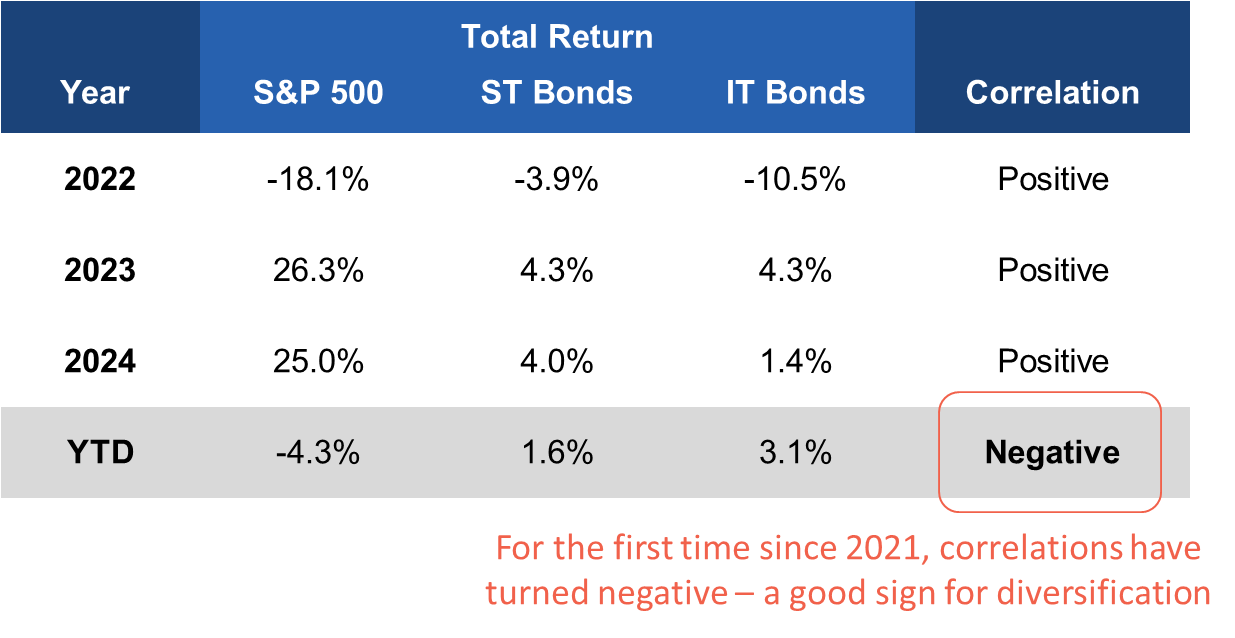

Recent high correlation between stocks and bonds broke down

There’s been much talk about high correlation between stocks and bonds in recent years. Historically bonds have had a negative correlation to equities, meaning that when equities fall, bond values go up. That relationship has not held in recent years.

The lack of correlation is an important benefit during rebalancing. The hope is that if stocks fall significantly, you can sell bonds to purchase the cheaper equities. That is an important way to extract value out of a diversified portfolio. But it does not always work. In the 2022 equity sell-off, bonds also fell in value – not as much but they still fell.

This year has started off more traditionally. In the face of declining stocks, bonds have produced positive returns enabling more effective rebalancing.

Chart 4: Bonds played their part

Source: Factset, S&P 500 index, BBG US Agg 1-3Y, BBG US Intermediate Agg

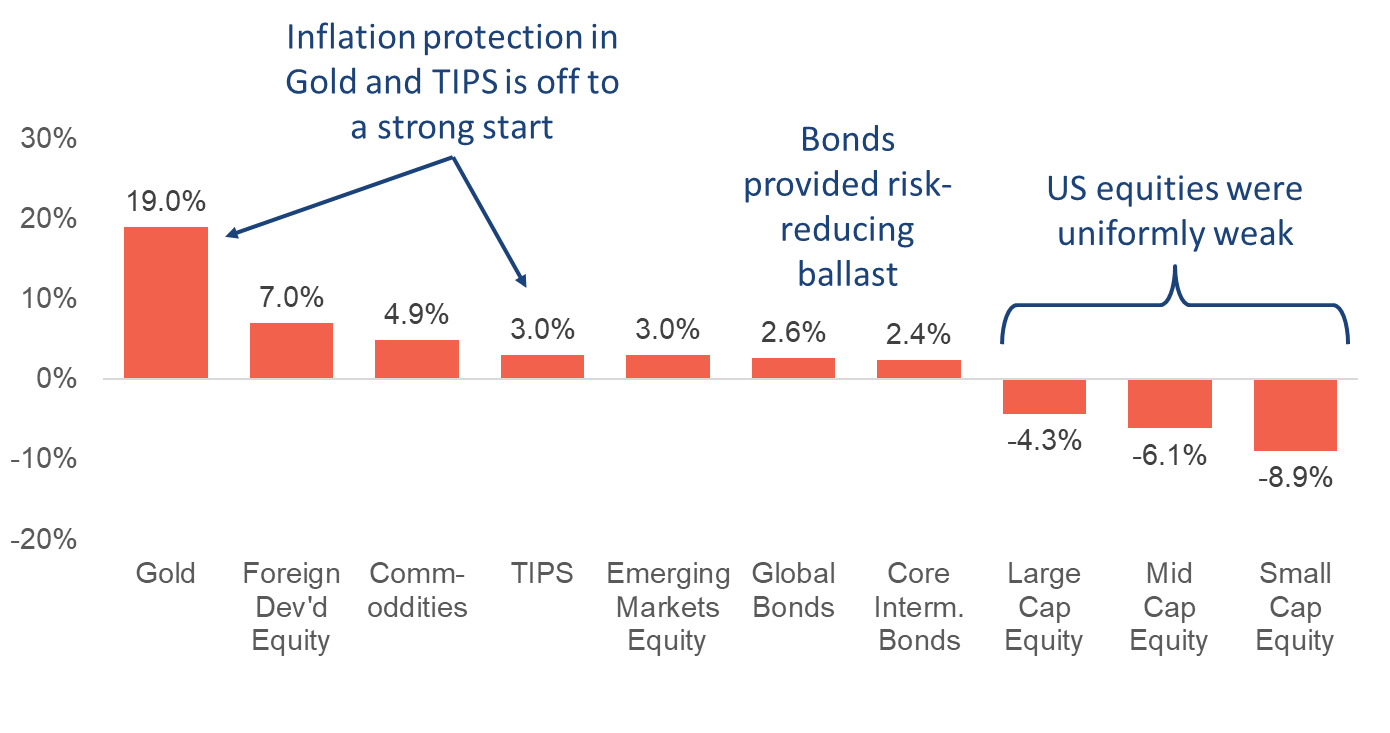

Gold continues to be a preferred asset in uncertain markets

We wrap up our review of the first quarter of 2025 with a snapshot of performance across asset classes. For the first time in recent memory, US equities are notably at the bottom of the performance scale.

High valuations and an uncertain economic outlook have shifted investor focus away from US equities and into international and perceived safe havens.

- Small-cap stocks took the brunt of the US equity underperformance.

- Gold produced a stunning 19% return, driven by its perception as both an inflation and uncertainty safe haven.

- International stocks significantly outperformed domestic stocks, helped by better valuations and currency.

- US bonds produced positive returns thanks in part to a downward shift in the yield curve as US economic uncertainty rises.

Chart 5: Q1 2025 Asset Class Performance

Source: Factset

“Be fearful when others are greedy and greedy when others are fearful.” – Warren Buffett

March’s weather may have come in like a lion and out like a lamb, but investors experienced a different weather pattern. The storm that was brewing as the quarter came to an end intensified as April 2nd’s tariff announcements appeared to catch investors off guard.

The announcement

The Trump administration unveiled tariffs that were more extensive than expected. Starting April 5, 2025, a universal 10% tariff will be imposed on all imported goods, applying to all countries unless specific exemptions are made. Additional “reciprocal tariffs” targeting approximately 60 countries deemed the “worst offenders” in trade practices will begin on April 9, 2025. Rates vary, with some as high as 54%. The scale of the tariffs rolled out have not been seen since the 1920s.

As of yet, no concrete countermeasures have been imposed yet from trading partners. For now, a full-blown trade war remains a risk, but not a certainty. Economists say these tariffs could lower GDP growth in the quarters ahead and push inflation higher. The probability of recession is elevated but not a given. Growth could just slow rather than turn negative.

Stocks were not impressed

As we type, markets are reacting sharply to the tariff announcements, with US large cap stocks down around 9%. Small cap is down slightly more. Bond prices rose, helping to offset equity declines in diversified portfolios.

Our initial take

The tariff announcement provided more questions than answers, elevating uncertainty further. In these early days, we are seeing the initial knee-jerk reactions based on assumptions and incomplete information. It will take time for the true impact to show up in economic data and company earnings reports. And let’s not forget, the administration could still capitulate.

Looking at Q2 and beyond

These are the moments that define an investor’s success, or lack thereof. How you react to market shocks matters. Do you react in fear, or do you heed the wise words of Warren Buffett, “be greedy when others are fearful and fearful when others are greedy.”

We don’t want to underplay the emotions of moments like these. It is not fun, and it is okay to experience fear, anger, and whatever other feelings bubble up. The important thing is not to let those emotions impact decisions on your investments. We certainly do not.

Once we set our emotions aside, we can’t help but see opportunities…

- Opportunities to lock in some tax losses to potentially lower tax bills,

- Opportunities to systematically rebalance from more expensive to cheaper securities,

- And perhaps opportunities to pick up some bargains if the sell-off continues.

We’ve been here before. In fact, the US stock market fell much further in 2018, 2020, and 2022… and that was a tremendous period to be an equity investor. That is, it was a tremendous period for equity investors that stayed invested and did not exit the market in fear.

We do not know the future and are not saying that these April showers will bring May flowers. Those flowers might come next week, next year or later. The stock market is volatile, and the price of attractive long-term returns is having to weather the inevitable bouts of weakness. But we take faith in the fact that companies have historically found a way to growth and profitability.

In the meantime, we have built diversified portfolios that can take advantage of these market moves. They are not immune from the downside, but a well-diversified portfolio enhances our ability to tax-loss harvest and opportunistically rebalance. In addition, we stand ready to make tactical allocation changes should a significant valuation opportunity open up.

On behalf of the team here at Strategic, I thank our growing community of clients, friends, and family members for placing their trust in us during these uncertain markets. We value your partnership.

About Strategic

Founded in 1979, Strategic is a leading investment and wealth management firm managing and advising on total client assets of over $3 billion, as of 6/3/26.

Disclosures

Strategic Financial Services, Inc. is registered with the Securities and Exchange Commission (SEC) as an Investment Advisor. The term “registered” signifies compliance with regulatory requirements and does not imply a certain level of skill or training.

The information provided on our website, including weekly market commentaries, financial planning articles, and other educational resources, is intended solely for educational purposes. It is designed to offer insights into financial planning and investment management, aiming to enhance understanding of financial concepts, strategies, and market trends. This content should not be interpreted as personalized investment advice or a recommendation for any specific strategy, financial planning approach, or investment product. Financial decisions are deeply personal and should be made considering the individual’s specific circumstances, goals, and risk tolerance. We recommend consulting with a professional financial advisor for personalized advice.

Please be aware that Strategic Financial Services, Inc. does not provide legal or tax advice. The content on this website is not intended to be used as such or as a substitute for legal or tax advice from a licensed professional. We advise seeking guidance from qualified legal and tax advisors regarding these matters.

Investment Risks and Portfolio Management.

The discussion of any investments on this website is for illustrative purposes only and provides no guarantee that the advisor will make any investments with the same or similar characteristics as those presented. The investments identified and described herein do not represent all the investments purchased or sold for client accounts. The selection of representative investments to discuss is based on various factors, including recent company news or earnings releases.

It should not be assumed that any investments discussed were or will be profitable. All investments involve risk, including the potential loss of principal. There is no assurance that investments mentioned will remain in client accounts at the time you view this information.

When index returns are mentioned on this site, they are provided as a general indicator of market conditions and are not representative of any client’s portfolio performance. Indices are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. Therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

While index returns are used as a framework to report on general market conditions, they should not be construed as an indicator of future performance of any specific investment or portfolio. Discussion of index returns is intended to provide context and insight, not to suggest that clients will achieve similar results. Each client’s portfolio is managed according to their specific investment goals and financial situation.

The opinions and any forward-looking statements expressed in the articles and videos featured in our resource center are as of the date of publication. These statements are based on current laws, regulations, market conditions, and other relevant factors, including third-party data. Given the dynamic nature of financial and regulatory environments, as well as potential changes in market conditions or economic circumstances, the information provided may become outdated or may no longer be accurate.

We rely on third-party data to form our opinions and projections, which means that these are subject to the same uncertainties that affect all data-dependent analyses. As such, we advise readers to exercise caution and not rely solely on the statements made herein for making financial decisions. It is recommended that investors consult with a professional advisor who can help assess the relevance and accuracy of the content in light of the current economic climate and personal financial situation.

Our website contains links to third-party websites as a convenience to our users. Strategic Financial Services, Inc. does not control, endorse, or guarantee the content found on such sites. We are not responsible for the accuracy, legality, or content of the external site or for that of subsequent links.

Contact the external site for answers to questions regarding its content.

The inclusion of any link does not imply our endorsement of the site, nor does it imply any association with its operators. Use of any such linked website is at the user’s own risk.