Put the Odds In Your Favor

Investors faced weak markets again in the third quarter. Inflation continues to prove a formidable adversary as the Federal Reserve uses the tools at its disposal to combat rising prices. The inflation story is still being written, but investors enter the fourth quarter with portfolios that can boast higher-yielding fixed income and stocks that are meaningfully cheaper than they were at the start of the year. We like those dynamics.

Fighting the Good Fight

High inflation remains a thorn in the side of the Federal Reserve, and Chairman Powell is singularly focused on extracting it with two powerful tools:

Raising rates:

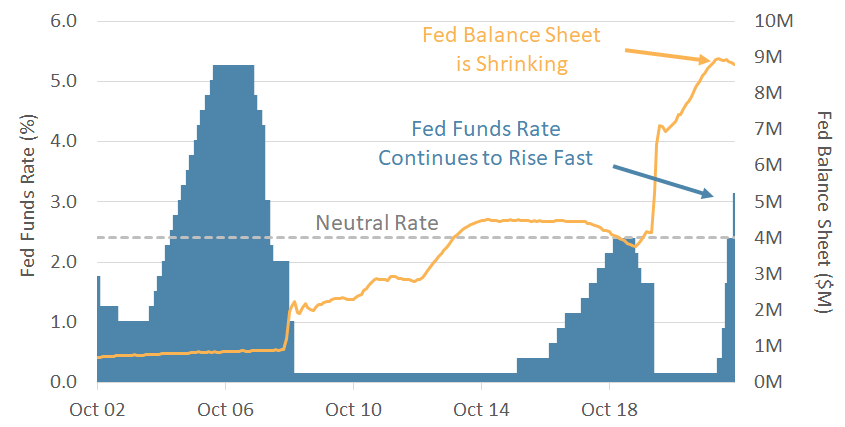

- The Fed Funds Rate was increased by 1.5 percentage points in Q3 and is now above the 2.4% level discussed as being the neutral rate (i.e., neither stimulative nor restrictive).

- The Fed raised its projected peak rate to 4.6%, which caught investors off guard and was a source of market weakness in Q3.

Shrinking the balance sheet

- The Fed’s balance sheet ballooned during and after the Financial Crisis of 2008 through “quantitative easing” (bond purchases).

- They are now in the process of tightening by halting the reinvestment of maturing securities.

- While rate increases boost yields on short-term bonds, quantitative tightening is designed to increase yields on longer-term bonds.

While the Fed’s actions have hit bond returns this year, the higher bond yields are, for the first time in a while, providing meaningful income to the fixed income sleeve of portfolios.

Chart 1: The Fed Tightening Pushes On

The Fed is fighting inflation from multiple angles

Source: The US Federal Reserve

A Formidable Adversary

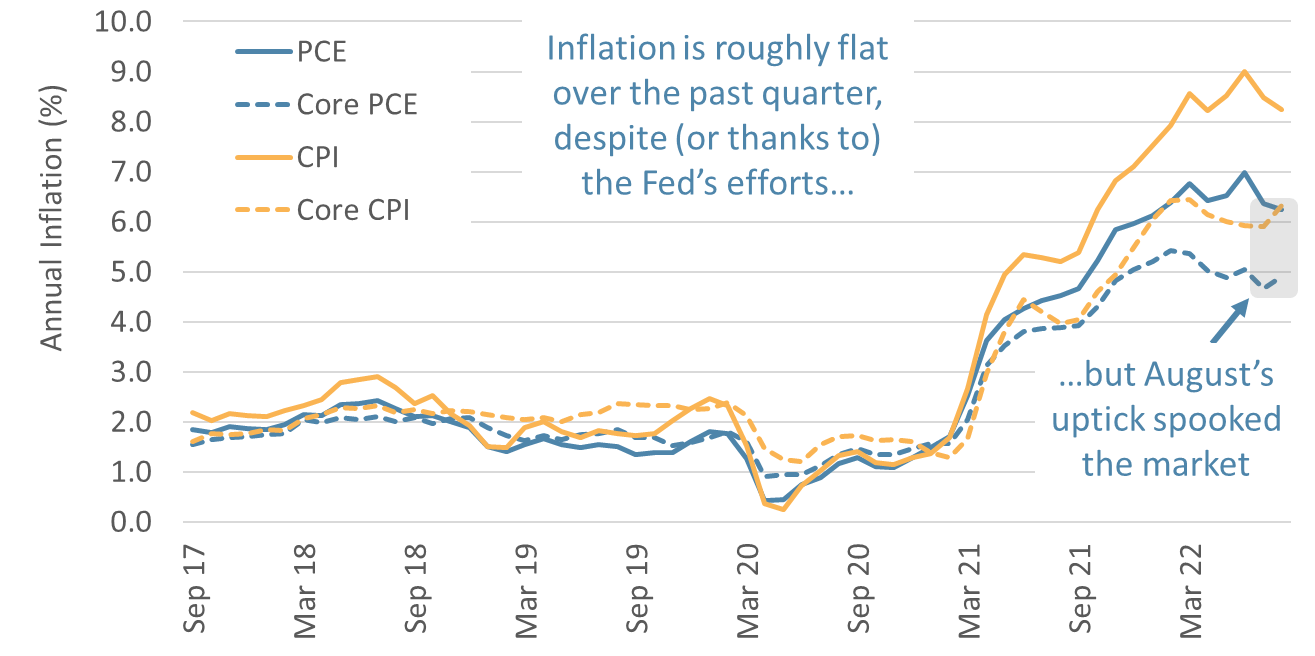

Inflation is proving to be a formidable adversary for the Fed. Core inflation, as measured by both the Consumer Price Index (CPI) and Personal Consumption Expenditures (PCE), has leveled off since the Fed began raising rates.

- But neither CPI nor PCE inflation has fallen significantly, and both negatively surprised in August.

- Sticky real estate prices proved to be one of the culprits in August.

- The increase in August was a blow to investor sentiment. Any inflation setback means a more aggressive Fed and a diminished probability of a soft landing.

While core inflation has been sticky, there has been a notable slowdown in other data, like real estate activity, that should eventually feed into lower prices as the Fed’s policies begin to bite.

Chart 2: Inflation is Proving Stubborn

Inflation has stabilized but has yet to fall meaningfully

Source: US Bureau of Labor Statistics, Bureau of Economic Analysis

Avoiding the Attractive Yield Trap

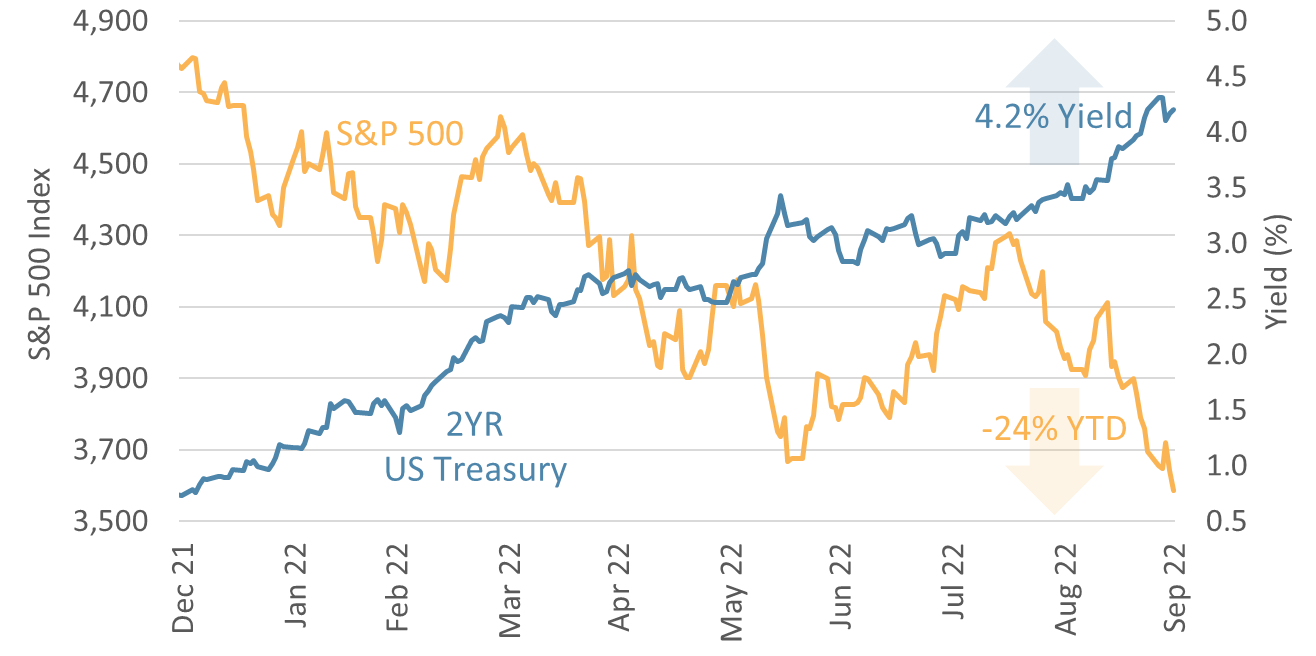

The yield on the 2YR treasury crested over 4% in Q3. With that increase came many questions about whether portfolios should increase their fixed income allocation.

- It has been a while since yields on Treasuries have been this high, and it is tempting for investors to consider locking them and even increasing allocation to them in their portfolios.

- But stocks are more attractive than they were at the beginning of the year as well. The S&P 500 fell about 24% through the first nine months of 2022. If you liked stocks at the end of 2021, you should like them even more now!

Short-term market moves are uncertain, and we do not see evidence that higher fixed income allocations are justified. Enjoy the higher yields within your fixed income allocation, but also take comfort knowing that the stocks in your portfolio cheaper than they were nine months ago (and have a better chance of outperforming inflation in the long run).

Chart 3: Yields are Higher and Stocks are Cheaper

Attractive Yields Should Not be Chased

Source: Factset, S&P 500 price return

Putting This Year’s Market Volatility in Perspective

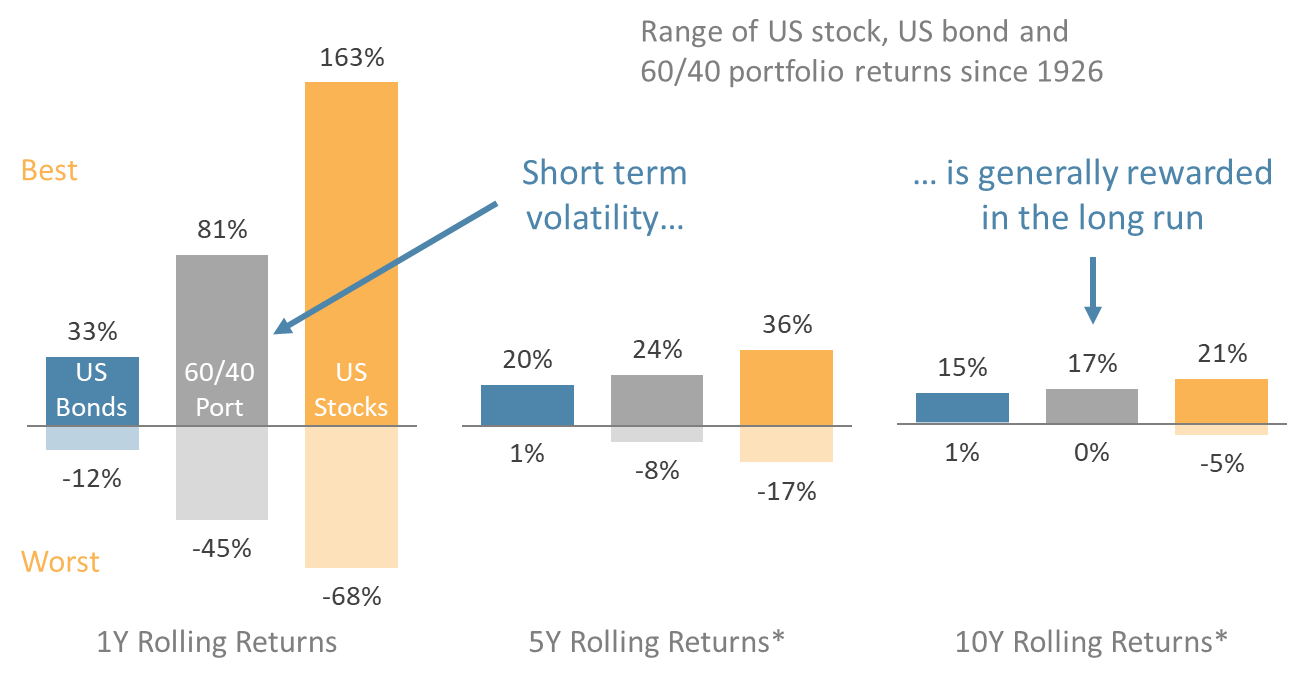

2022 has seen significant market volatility, made worse by the high positive correlation between stocks and bonds. A sell-off in equities is not often accompanied by such weakness in bonds.

- But history shows that over short periods, volatility is typical. In any given year, we have seen a basic 60/40 portfolio return as much as 81% and decline as much as 45%.

- But over more extended periods, like ten years, that volatility moderates. Since 1926, a 60/40 portfolio has almost always produced a positive annual return.

For long-term investors, weakness like we have been experiencing presents opportunities. Values present themself, and disciplined opportunistic rebalancing of their well-diversified portfolio can systematically sell high and buy low.

Chart 4: Putting Short-Term Volatility in Perspective

Short-term volatility is generally rewarded in the long-term

Source: Blackrock, Student of the Market, Sept 2022

* annualized

A Highly Correlated Decline

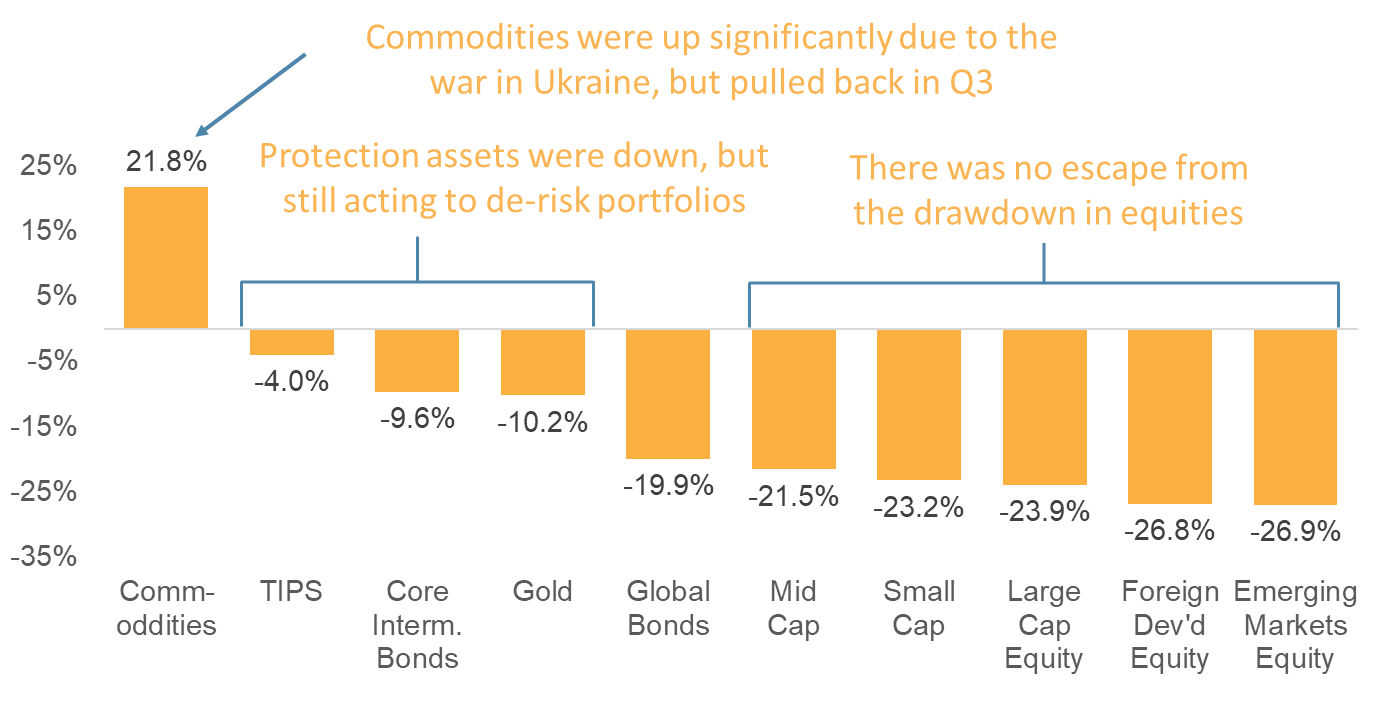

Risk assets fell across the board in the first nine months of the year. Protection assets were down, but not as much, providing some rebalancing benefits.

- Equities fell across regions and market cap.

- Value stocks generally outperformed Growth.

- Commodities spiked primarily due to oil and the war in Ukraine. While still high, those returns are way off their peak (they were up 36% in H1).

- TIPS has done relatively well. We believe that dynamic has played out and moved our allocation to underweight earlier in the year.

Years like 2022 are part of investing. The long-term positive returns that we seek come at the cost of short-term volatility. Patient, disciplined investors know this and look for opportunities within weakness.

Chart 5: Asset Class Performance through Q3 2022

Weakness Across the Board Through Q3 2022

Source: Factset

“I will tell you how to become rich. Close the doors. Be fearful when others are greedy. Be greedy when others are fearful.” — Warren Buffett

Every three months, as we consider the quarter that lies ahead, we make a conscious effort to avoid fortune-telling. As Mark Twain said, “Prediction is difficult, particularly when it involves the future.” For markets, I would take it a step further and say prediction is futile. The only guarantee is that markets will go up and down.

Yet, in some ways, there is more clarity today about market drivers than is typical. For one, we know that the asset values are being driven by the Fed. The more work the Fed has to do to bring inflation under control, the worse it will get for investors. That is why bad news will likely be good news in the fourth quarter. Economic indicators showing signs of weakness, such as rising unemployment, declining real estate traffic, and weakening retail sales, could all be received positively as signs that the Fed’s actions are having an impact and that the end of restrictive policies are in sight.

The other fact we know is that bond yields are higher now than they were at the beginning of the year, and stock valuations have fallen significantly. We do not mention this to claim we are calling the bottom of the market. That can only be done with a crystal ball. But we can enter the fourth quarter with confidence that the potential for higher future returns is much greater now than it was at the start of the year. Successful long-term investors recognize these moments and lean into them. Unsuccessful investors flee in the face of declines with an unrealistic hope that they will time their re-entry perfectly. The odds are against it.

We aim to put the odds in our favor consistently. That is why we put proven persistent factors (high quality, attractive value, strong momentum, small size) at the core of our portfolio strategies. It is also why we systematically seek to buy low and sell high through opportunistic rebalancing and avoid common behavioral biases that plague investors. Over time, these decisions are designed to outperform more passive strategies. Better days lie ahead for investors. They may or may not begin in Q4, but disciplined investors will be ready to take advantage.

About Strategic

Founded in 1979, Strategic is a leading investment and wealth management firm managing and advising on total client assets of over $3 billion, as of 6/3/26.

Disclosures

Strategic Financial Services, Inc. is registered with the Securities and Exchange Commission (SEC) as an Investment Advisor. The term “registered” signifies compliance with regulatory requirements and does not imply a certain level of skill or training.

The information provided on our website, including weekly market commentaries, financial planning articles, and other educational resources, is intended solely for educational purposes. It is designed to offer insights into financial planning and investment management, aiming to enhance understanding of financial concepts, strategies, and market trends. This content should not be interpreted as personalized investment advice or a recommendation for any specific strategy, financial planning approach, or investment product. Financial decisions are deeply personal and should be made considering the individual’s specific circumstances, goals, and risk tolerance. We recommend consulting with a professional financial advisor for personalized advice.

Please be aware that Strategic Financial Services, Inc. does not provide legal or tax advice. The content on this website is not intended to be used as such or as a substitute for legal or tax advice from a licensed professional. We advise seeking guidance from qualified legal and tax advisors regarding these matters.

Investment Risks and Portfolio Management.

The discussion of any investments on this website is for illustrative purposes only and provides no guarantee that the advisor will make any investments with the same or similar characteristics as those presented. The investments identified and described herein do not represent all the investments purchased or sold for client accounts. The selection of representative investments to discuss is based on various factors, including recent company news or earnings releases.

It should not be assumed that any investments discussed were or will be profitable. All investments involve risk, including the potential loss of principal. There is no assurance that investments mentioned will remain in client accounts at the time you view this information.

When index returns are mentioned on this site, they are provided as a general indicator of market conditions and are not representative of any client’s portfolio performance. Indices are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. Therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

While index returns are used as a framework to report on general market conditions, they should not be construed as an indicator of future performance of any specific investment or portfolio. Discussion of index returns is intended to provide context and insight, not to suggest that clients will achieve similar results. Each client’s portfolio is managed according to their specific investment goals and financial situation.

The opinions and any forward-looking statements expressed in the articles and videos featured in our resource center are as of the date of publication. These statements are based on current laws, regulations, market conditions, and other relevant factors, including third-party data. Given the dynamic nature of financial and regulatory environments, as well as potential changes in market conditions or economic circumstances, the information provided may become outdated or may no longer be accurate.

We rely on third-party data to form our opinions and projections, which means that these are subject to the same uncertainties that affect all data-dependent analyses. As such, we advise readers to exercise caution and not rely solely on the statements made herein for making financial decisions. It is recommended that investors consult with a professional advisor who can help assess the relevance and accuracy of the content in light of the current economic climate and personal financial situation.

Our website contains links to third-party websites as a convenience to our users. Strategic Financial Services, Inc. does not control, endorse, or guarantee the content found on such sites. We are not responsible for the accuracy, legality, or content of the external site or for that of subsequent links.

Contact the external site for answers to questions regarding its content.

The inclusion of any link does not imply our endorsement of the site, nor does it imply any association with its operators. Use of any such linked website is at the user’s own risk.