Navigating from Rate Cuts to Ballot Boxes

We received the rate cut we were waiting for in Q3 and then some. Investors handled the shift in policy in stride, with most asset classes we follow posting positive returns. The hope for a soft landing remains alive. But many now have their eyes fixed on the upcoming Presidential election and are wondering how best to prepare their portfolios. We review the quarter and provide some perspective on the fast-approaching November 5th vote.

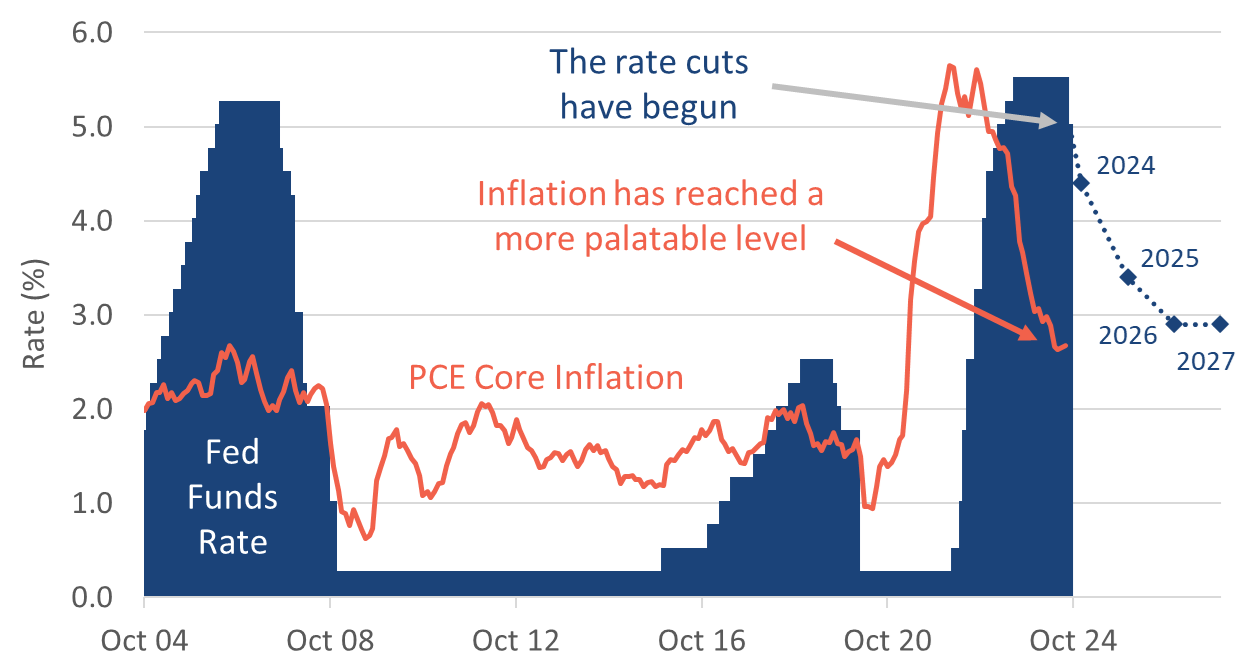

The Federal Reserve cut rates for the first time since 2020

It was no surprise that the Fed cut rates this quarter. It was well-flagged by Chairman Powell. However, the 50bps cut was more than most had expected. The cut came as inflation has fallen to a more palatable level and some cracks in the jobs market appeared to be forming.

PCE Core Inflation (a preferred Fed measure) did not fall much in the quarter. It has halved from its 2021 peak and has leveled around 2.6% level. The Fed would still like to see it a bit lower, but we are in the range of “normal” from pre-pandemic years.

Meanwhile unemployment rates, while still historically low, have crept up slightly from their 2023 levels. In September, the US Bureau of Labor Statistics reported total unemployment at 4.2%. That is up from the 3.4% low of the previous year. These are not big numbers, but the Fed is well aware that its policies have a lagged effect, and they do not want to get behind the curve as they try to stick the economic soft landing.

Chart 1: Rate Cuts Have Begun

Source: The US Federal Reserve, Bureau of Economic Analysis

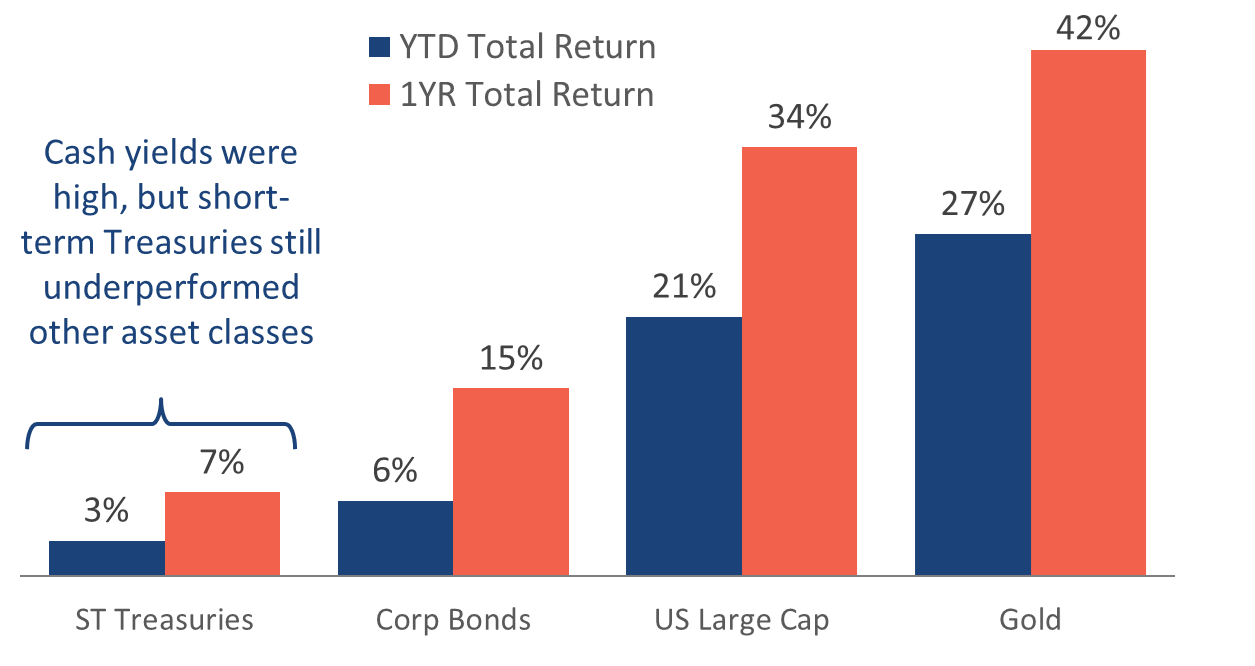

With lower Fed Funds rate comes lower yields on cash

Investors have been drawn in by relatively high yields on risk-free short-term Treasuries, but those rates are falling. Now is a good time for investors to ensure their allocation is not overly skewed toward cash.

The Fed’s dot plot (see Chart 1 above) shows where the Fed Governors see rates going. Over the next few years, current expectations are for declines to 2.9%. Short-term instruments, like money market funds, will quickly reflect the lower Fed Funds rates and will face reinvestment risk. Shifting to longer-term bond instruments has the benefit of locking in current rates for longer.

The past year has been a tough lesson for those who saw high-yielding short-term instruments as a “sure thing” and sold risky assets to hold cash-like investments. In the end, it was a sure thing… but unfortunately that sure thing significantly underperformed other riskier asset classes.

Chart 2: Cash Yields are Falling

Source: Factset, VGST, VCIT, S&P500, GLDM

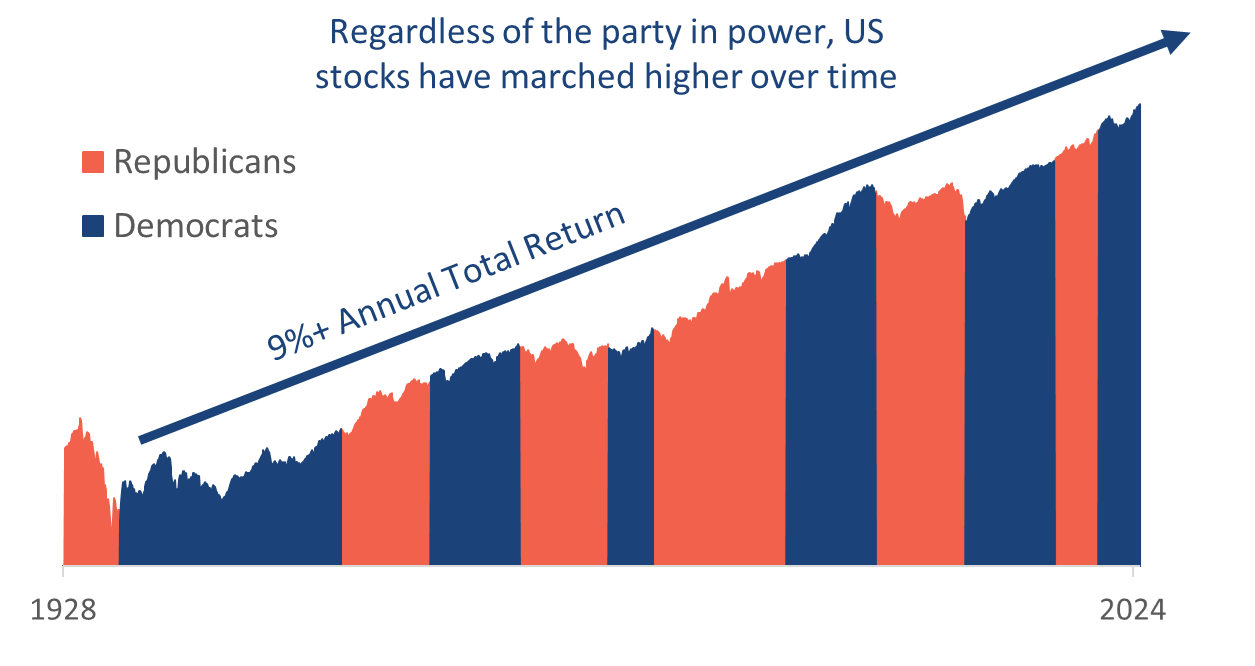

US stocks have advanced irrespective of the administration

If you are having a sense of déjà vu, it’s not you… we included this same section last quarter. Some messages are worth repeating multiple times.

Election angst remains high. The polls are signaling a close election, so the outcome of the is unknowable. But investors can take comfort in past precedents. As evidence-based investors, we take many of our queues from the past. It is not to say that history will repeat itself, but it rhymes often enough to provide an advantage to students of its lessons.

The world economy and the economic cycle are bigger determinants of stock market returns than those sitting in the White House. Policies can have an impact, but companies are dynamic and find a way to profit across administrative regimes.

An election is a binary uncertain event, which naturally elevates investor nerves. Attempts to predict the market reaction should be avoided. Evidence-based investors know that the future is unknowable, and the best investing action at any point in time is the one based on what we know today and not what we think will happen in the future.

Chart 3: The Economy Drives Investments Not Presidents

Source: Factset, S&P 500 index total return

Opportunistic rebalancing can capitalize on market volatility

Continuing on the election theme, we often get asked what we are doing to prepare portfolios for the election. It’s an understandable question. But uncertain events like the Presidential election are not a reason to change allocation or strategy. My crystal ball is currently in the shop, so we can’t predict the future better than anyone else. Even if we knew the election result, knowing how the market will react is a whole other question.

So, are investors helpless? No. Investors should not be trying to guess the result of uncertain events, but rather employ a strategy that is prepared to capitalize on whatever may come, be it an election, pandemic, or some other unknown unknown. Here’s a simplified version of our evidence-based approach:

- Start with a truly well-diversified portfolio devoid of home bias and concentration risk (across sectors, factors, geographies).

- Shift allocation tactically based on sound, evidence-based research.

- Monitor assets frequently for significant price moves up or down.

- Systematically sell high and buy low to take advantage of the best rallies and worst declines. We call this opportunistic rebalancing.

- Rinse and repeat.

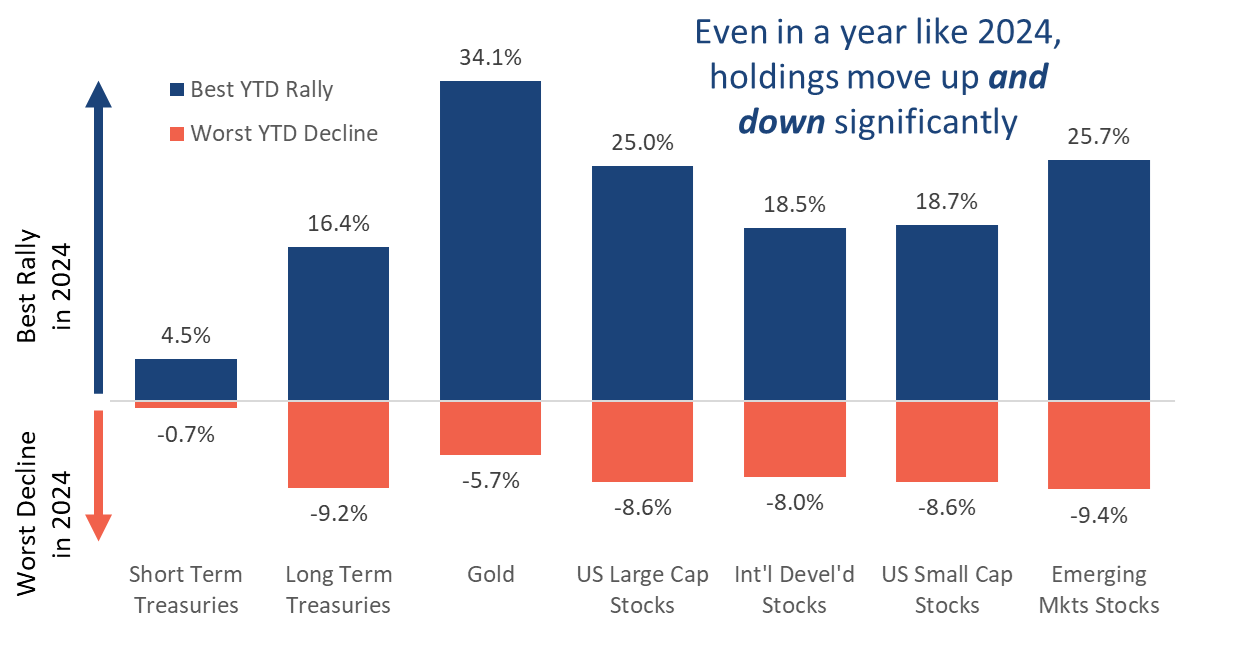

The chart below shows that even in a year like 2024, where most assets have gone up, there are meaningful short-term declines that create opportunities to rebalance. We don’t know what the election will bring, but it’s fairly certain we won’t have a result on November 5th. It will take a week or so to count ballots in those states that don’t start counting until the polls close. If this uncertainty brings market volatility, we will be ready to take advantage of those ups and downs.

Chart 4: Fear and Uncertainty Create Opportunity

Source: Factset, VGST, VGLT, GLDM, LRGF, INTF, SMLF, EMGF

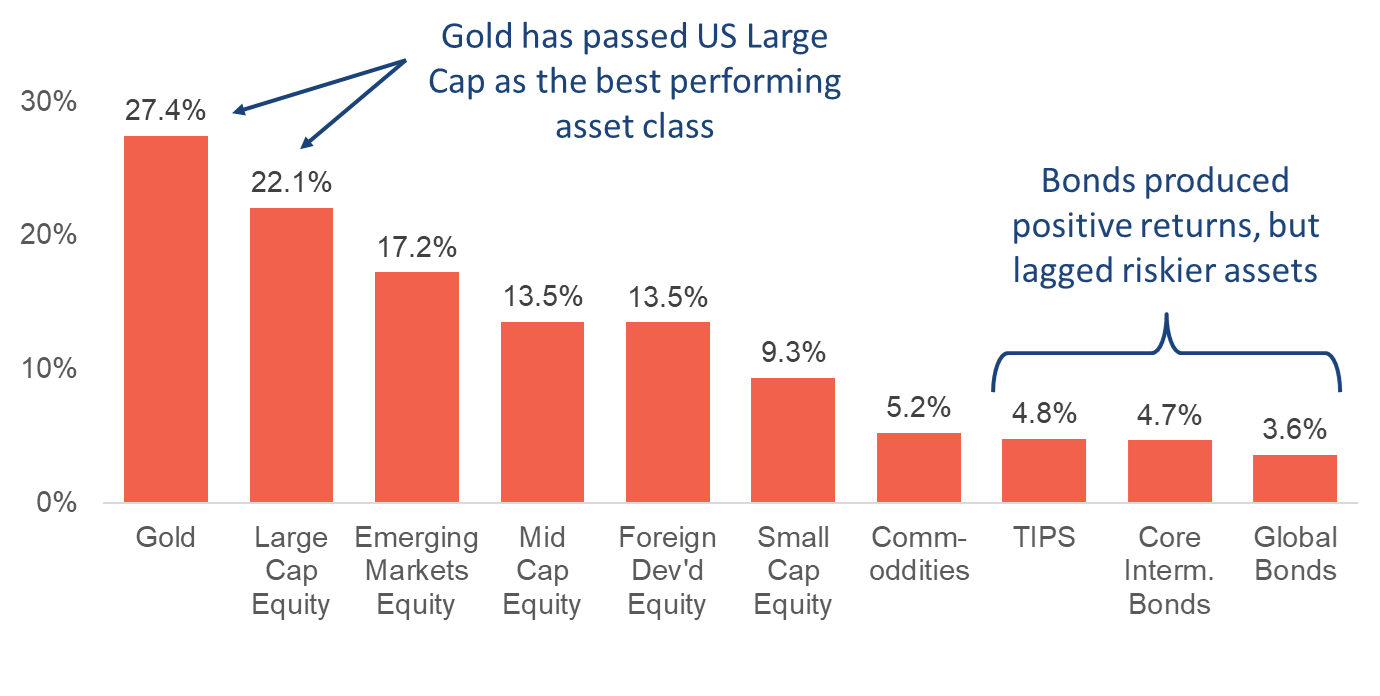

Diversifiers provided market leadership in Q3

As always, we wrap up our charts with an overview of the performance of the major asset classes. Performance was notably universally positive in the first three quarters of the year.

As good as US Large Cap stocks have performed this year, Gold has surpassed them as the best performing asset class this year. Gold is viewed as a store of value and a go to asset in times of uncertainty. However, the driver may have more to do with central bank stockpiling around the globe.

While US Large Cap stocks are leading amongst equities this year, diversifiers are catching up. Emerging Markets, US Mid-Cap stocks, Developed International stocks, and US Small Cap stocks all outperformed US Large Cap in the third quarter of the year. In short, it was an excellent quarter for a well-diversified portfolio.

On the bond side of the portfolio, yields have been attractive and market values have benefited from falling interest rates, but returns have not been able to match those of riskier assets.

Chart 5: YTD Asset Class Performance (through Q3)

Source: Factset

We always say we don’t predict we prepare. Warren Buffett said it better: “Predicting rain doesn’t count. Building arks does.”

In the world of investing, predictions are as common as pumpkin spice lattes in October. Every newsletter seems to have a crystal ball, forecasting market movements with unwavering certainty. But predicting the future is a fool’s errand. We’d rather spend our time preparing for it.

Regular readers of our publications know how we prepare as evidence-based investors… well-diversified portfolios, factor-based investing, and opportunistic rebalancing for starters. You’ve probably heard it a dozen times from us or more. But my question to you, the reader… Are you prepared?

Are you prepared for:

- The fact that it may be a week or more after the election until the final result is known?

- Stocks continuing to soar, entering bubble territory?

- Inflation ticking back up?

- Escalation of the conflict in the Middle East?

- A new wave of AI euphoria?

At any given time in history, we have had these emotionally charged uncertainties looming. That’s normal. My challenge to you as we close out 2024 is to see all of these, the good and the bad, as opportunities. Each of these has the potential to move markets, and disciplined investors know how to set emotions aside, evaluate what they know to be true today, and take advantage of any opportunity that presents itself.

In the wise words of Warren Buffett, “Outstanding long-term results are produced primarily by avoiding dumb decisions, rather than making brilliant ones.” We do not know with certainty what Q4 will bring, but we do know that those who try to guess will likely be wrong. And those that put dollars behind those guesses over time will likely underperform.

So, open your arms to the oncoming uncertainty. Don’t avoid it. Stay calm, stay invested, and embrace whatever the coming quarter brings as an opportunity to outperform. You are not alone in this journey. We are here to partner with you so you can navigate the unknown with confidence. On behalf of the team here at Strategic, I thank our clients, friends, and family members for placing their trust in us. We truly appreciate having you as part of our Strategic Community.

About Strategic

Founded in 1979, Strategic is a leading investment and wealth management firm managing and advising on total client assets of over $3 billion, as of 6/3/26.

Disclosures

Strategic Financial Services, Inc. is registered with the Securities and Exchange Commission (SEC) as an Investment Advisor. The term “registered” signifies compliance with regulatory requirements and does not imply a certain level of skill or training.

The information provided on our website, including weekly market commentaries, financial planning articles, and other educational resources, is intended solely for educational purposes. It is designed to offer insights into financial planning and investment management, aiming to enhance understanding of financial concepts, strategies, and market trends. This content should not be interpreted as personalized investment advice or a recommendation for any specific strategy, financial planning approach, or investment product. Financial decisions are deeply personal and should be made considering the individual’s specific circumstances, goals, and risk tolerance. We recommend consulting with a professional financial advisor for personalized advice.

Please be aware that Strategic Financial Services, Inc. does not provide legal or tax advice. The content on this website is not intended to be used as such or as a substitute for legal or tax advice from a licensed professional. We advise seeking guidance from qualified legal and tax advisors regarding these matters.

Investment Risks and Portfolio Management.

The discussion of any investments on this website is for illustrative purposes only and provides no guarantee that the advisor will make any investments with the same or similar characteristics as those presented. The investments identified and described herein do not represent all the investments purchased or sold for client accounts. The selection of representative investments to discuss is based on various factors, including recent company news or earnings releases.

It should not be assumed that any investments discussed were or will be profitable. All investments involve risk, including the potential loss of principal. There is no assurance that investments mentioned will remain in client accounts at the time you view this information.

When index returns are mentioned on this site, they are provided as a general indicator of market conditions and are not representative of any client’s portfolio performance. Indices are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. Therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

While index returns are used as a framework to report on general market conditions, they should not be construed as an indicator of future performance of any specific investment or portfolio. Discussion of index returns is intended to provide context and insight, not to suggest that clients will achieve similar results. Each client’s portfolio is managed according to their specific investment goals and financial situation.

The opinions and any forward-looking statements expressed in the articles and videos featured in our resource center are as of the date of publication. These statements are based on current laws, regulations, market conditions, and other relevant factors, including third-party data. Given the dynamic nature of financial and regulatory environments, as well as potential changes in market conditions or economic circumstances, the information provided may become outdated or may no longer be accurate.

We rely on third-party data to form our opinions and projections, which means that these are subject to the same uncertainties that affect all data-dependent analyses. As such, we advise readers to exercise caution and not rely solely on the statements made herein for making financial decisions. It is recommended that investors consult with a professional advisor who can help assess the relevance and accuracy of the content in light of the current economic climate and personal financial situation.

Our website contains links to third-party websites as a convenience to our users. Strategic Financial Services, Inc. does not control, endorse, or guarantee the content found on such sites. We are not responsible for the accuracy, legality, or content of the external site or for that of subsequent links.

Contact the external site for answers to questions regarding its content.

The inclusion of any link does not imply our endorsement of the site, nor does it imply any association with its operators. Use of any such linked website is at the user’s own risk.