Enter the New Year with Optimism

What comes around goes around. After two glutenous years of Washington monetary and fiscal stimulus, the Fed put an end to the party and set its sights on controlling inflation. Higher rates and a shrinking balance sheet were the tools. Both stocks and bonds were caught in the wake, resulting in one of the worst years on record for a balanced portfolio.

Investors now enter 2023 wondering if the worst is over or if a hard landing is lurking in our future. Many industry pundits will be on record this month with their 2023 predictions, claiming clarity on the road ahead for investors. This article will not claim such clairvoyance. The future is as uncertain and unknowable as always, which is okay. Successful investing comes from properly preparing for the future and taking advantage of the opportunities that the unpredictable markets present.

Looking for Signs of Peak Rates

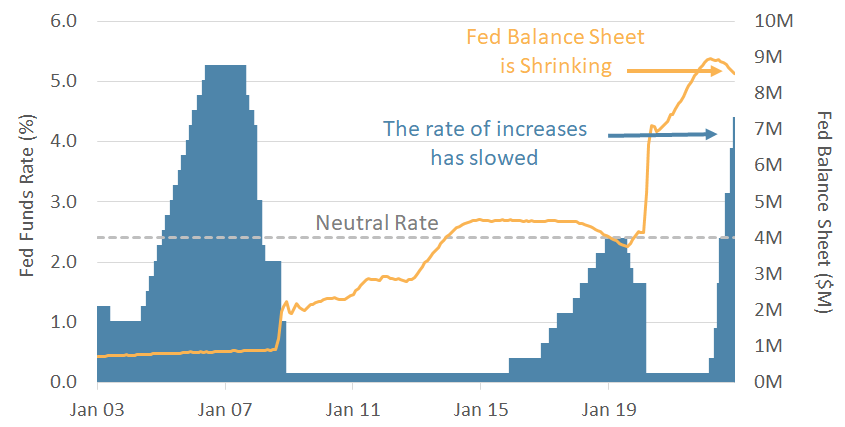

Inflation was the Fed’s primary concern in the fourth quarter. But it has moderated its approach. The last Fed Funds rate increase was “just” 50 bps. Historically that is still a large rate increase, but after four consecutive 75 bps raises, it is clearly a deceleration. The change comes as inflation has steadily declined from its peak in June of 2022. While still high, it is at least now headed in the right direction.

The change in tact from the Fed has investors eyeing “peak rates,” which could come as early as this Spring. The current consensus is a peak in the 5-5.5% range. The Fed is still doing everything it can to convince the market that the peak is still a ways off. If consumers get too much comfort too soon, the rate increases will be diluted and not have the desired deflationary impact. Monetary policy is as much about perception as it is about reality. If the Fed gets the balance right, they dismount with a soft landing. If they mismanage expectations, a hard landing is in our future. Portfolios should be prepared for both scenarios.

Chart 1: Investors are Eyeing Peak Rates

The Fed has moderated its inflation fight as investors eye peak rates

Source: The US Federal Reserve

Don’t Fear the “R” Word

Talk of recession was rampant in the fourth quarter. An economic slowdown is inevitable, and a recession of some sort is likely. But that does not mean that the coming years will necessarily be bad for investors at this point in the cycle.

Markets are forward-looking and pretty good at pricing in current sentiment and expectations. With the prevailing consensus that a recession is in our future, it is fair to assume that a recession is priced in. With stocks and bonds down significantly in 2022, markets are already reflecting a lot of bad news.

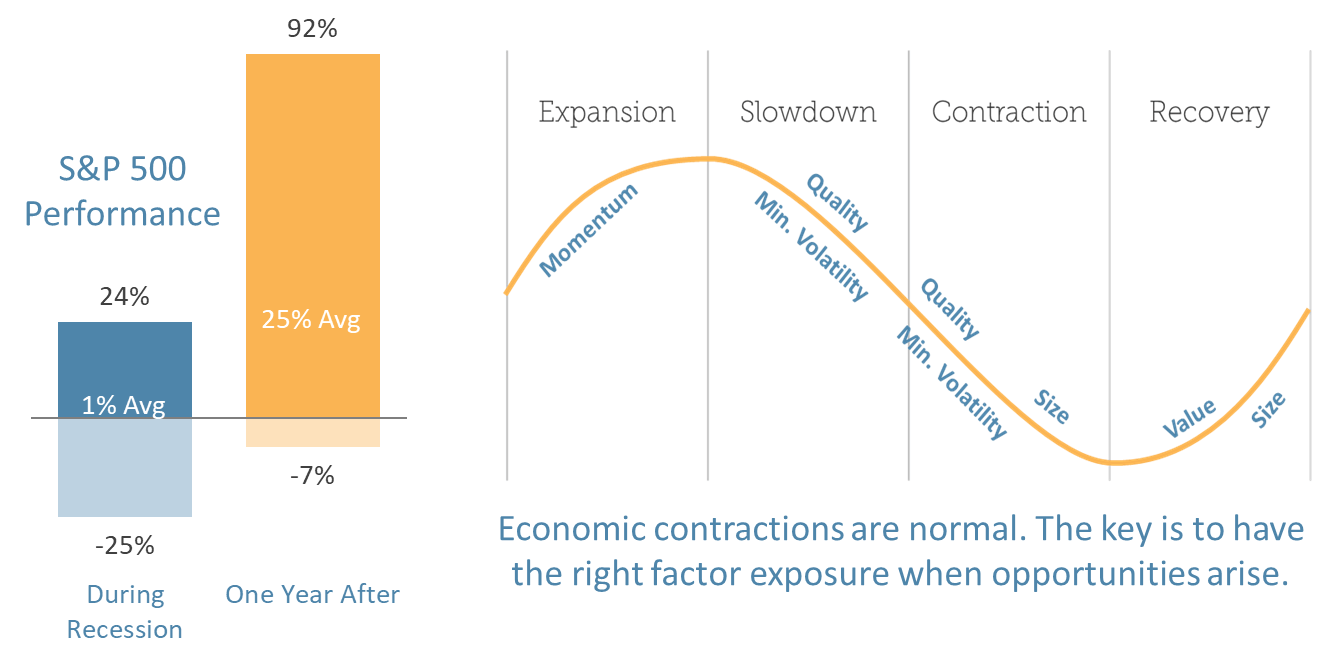

We like to look at past trends. What we find with recessions is that returns can vary dramatically. On average, the US stock market is up around 1% during recessions. In some recessions returns were down double-digits, in others, they were up double-digits (see Chart 2). The year after a recession is a different story. The average return was 25%! There is no need to try to time this dynamic. Combined, the years in and after a recession have historically provided attractive upside.

As evidence-based investors, we believe in focusing on proven persistent equity factors (eg. Quality, Value, Momentum, Size, Min Vol). Factors are an important strategy for managing economic cycles – particularly downturns. What we find is that each factor outperforms at different stages of the economic cycle (see Chart 2). Good factor diversity is a great first step in preparing a portfolio for the inevitable uncertainty of the future. Factors also provide excellent tools for tactical positioning in a recession. For example, Value has historically outperformed in recovery, so has been a good tactical overweight when a recession is already priced in.

Chart 2: Recession is Not Something to Fear

Recessions are normal and can present opportunities

Opportunities Within a Globally Diversified Equity Portfolio

We always promote the importance of diversification, but 2022 has put the benefits on display within equities. Large-cap US stocks had been infallible for a few years prompting questions about the benefits of diversification. That all changed last year as the mega-caps that could do no wrong came crashing down to earth. Developed International proved a much better performer.

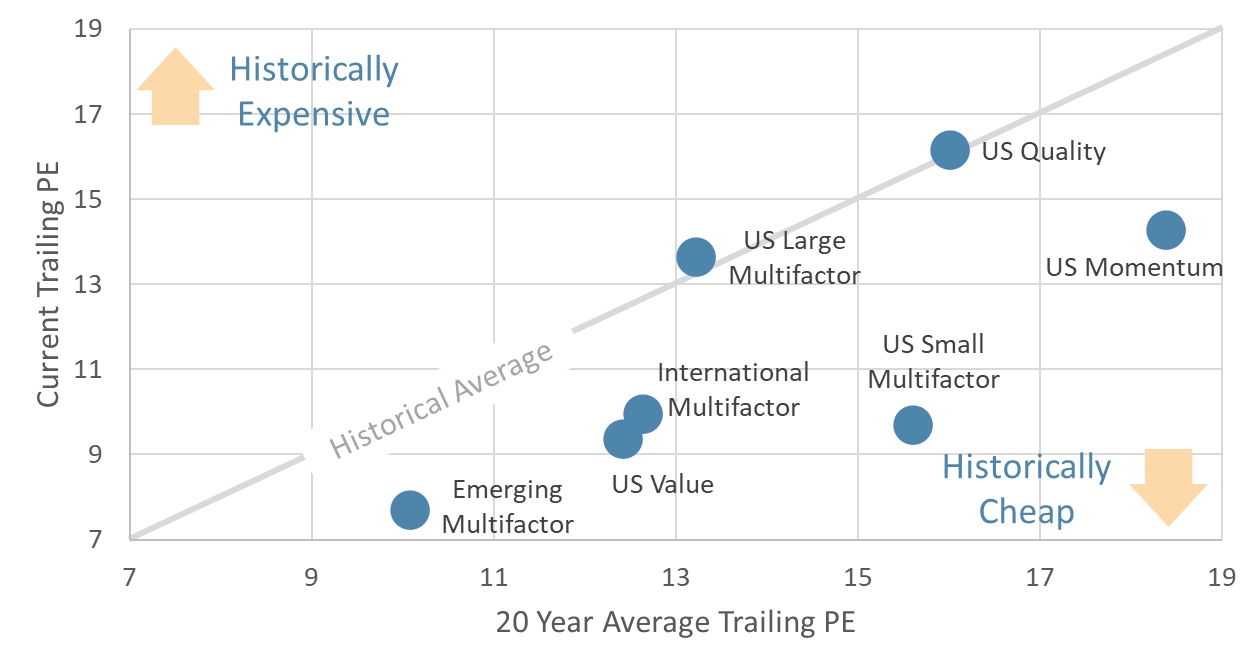

Looking at valuations today within our preferred universe of factor-based investments, not all regions and factors are valued at the same discount (see Chart 3).

- Value and Momentum are the cheapest individual factors (relative to their own trailing PE history).

- Small-Cap is far cheaper than Large-Cap.

- Large-Cap International is cheaper than Large-Cap US.

Valuation is just one way to evaluate an investment’s credentials, but we believe in the current environment, the chart below highlights a genuine opportunity in diversification and a risk for those with too much large-cap US domestic exposure.

Chart 3: Equity Opportunities Within a Diversified Portfolio

The sell-off has created value globally but not equally

A New Lease on Life for Fixed Income

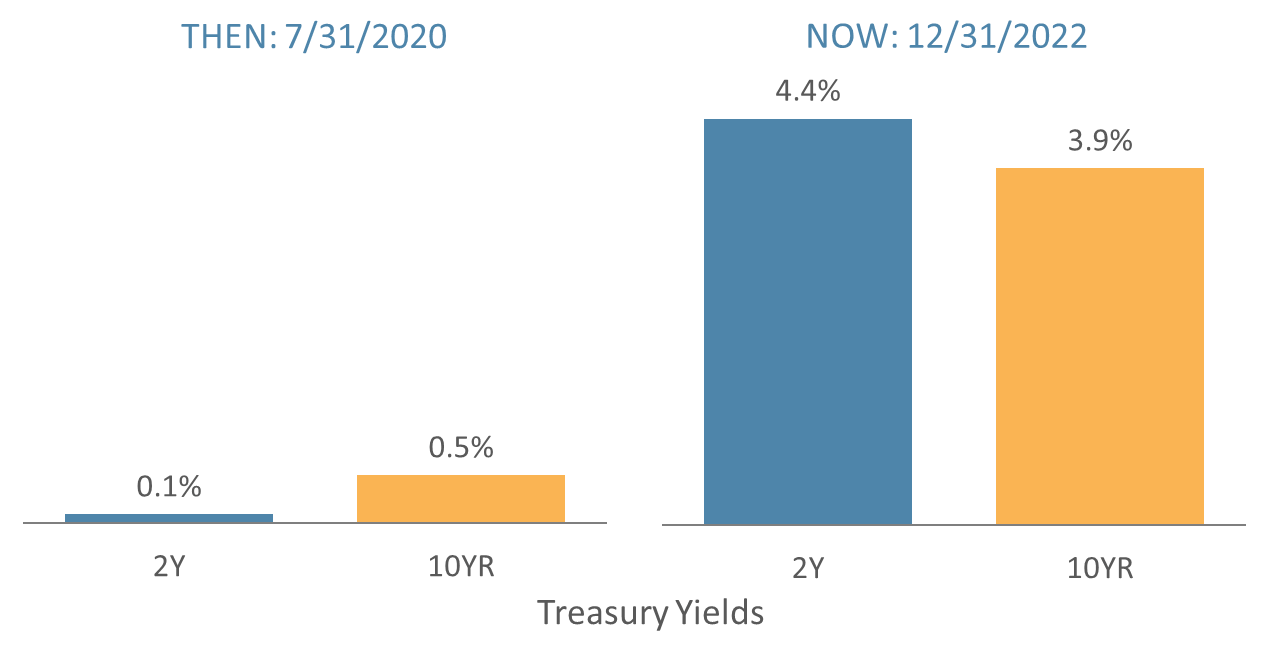

Rising rates from the Fed resulted in a rare, multi-year sell-off in bonds. The upside is a margin of safety in valuations that we have not seen in many years. In Chart 4 below, we contrast 2-year and 10-year Treasury yields from mid-2020 to the end of 2022. The change in yields is nothing short of exceptional. For the first time in a while, investors can earn decent income on bonds.

As the Fed raised rates, shorter-duration securities (like the 2-year) outperformed longer-duration securities, as would be expected. Despite the inverted yield curve, now is the time to think about extending portfolio duration. Longer-duration bonds should outperform if and when the Fed begins cutting rates, and at these yields, you are getting paid to wait. But now is not the time to be increasing your allocation to bonds. After a 20% sell-off in 2022, equities also look more attractive.

Chart 4: Treasury Yields Then and Now

A much greater margin of safety in bonds

A Historic and Forgettable Year for Balanced Portfolios

A balanced portfolio of equities and fixed income had one of the worst years on record as assets fell across the board. The correlation was high between equities and fixed income, with both having a challenging year. While bonds were down, they were down less than equities and therefore still provided some rebalancing opportunities.

Equities fell across regions and market cap (see Chart 5). Within that mix, Value was a relative bright spot, outperforming Growth by historic margins. Developed International equities faired better than their domestic peers. Commodities (primarily oil and gas) spiked in large part due to the war in Ukraine. While commodity returns are still high on the year, they are well off their peak.

Gold, a go-to asset in uncertain times, had strong returns in Q4, ending slightly down on the year.

Chart 5: Asset Class Performance in 2022

2022 was a remarkable year for diversified portfolios

Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas.

-Paul Samuelson

We enter 2022 with optimism. Are we predicting a big rebound this year? No. Why? Because, as evidence-based investors, we don’t predict. Instead, our optimism comes from the knowledge that:

- US stocks are down over 20% from their peak and therefore offer more potential upside than they did a year ago when valuations were well above average.

- Bonds offer a margin of safety and higher income than we have been able to enjoy for many years.

- Inflation is falling, and we are much closer to the peak Fed Funds rate than we were at this time in 2022.

So what is our advice to investors? Once you concede that prediction is a fool’s errand, you can better spend your time preparing your portfolio for the unknown. We recommend seeking to tip the odds in favor of outperformance at each step in the investment process:

- Diversify your portfolio with a mix of large and small-cap, domestic and international, equity and bonds, and uncorrelated protection such as gold.

- Avoid unnecessary fees and expensive alternative investments that don’t have a proven track record of providing higher returns.

- Put factors at the core. Why own the whole stock market when certain segments (Quality, Value, Momentum, Small Size, and Minimum Volatility) have persistently outperformed over time?

- Seek tactical opportunities within factors, not based on guesses about the future but based on what we know today. For example, we know individual equity factors like Value and Momentum are starting the year historically cheap and tend to outperform in recovery and expansion.

- Avoid shiny objects, like cryptocurrencies (not so shiny anymore) and NFT art. These are not investments. If you want them, be sure to use discretionary money, not your retirement accounts, to fund these hobbies.

- Opportunistically rebalance. Blindly rebalancing an entire portfolio periodically, like every quarter, is archaic and leaves money on the table. Instead, look weekly for opportunities to rebalance surgically at the ticker level. Looking often captures those unique and sometimes fleeting moments within a security to sell high and buy low.

- Harvest losses to save on taxes if the market misbehaves again. This is not a year-end exercise but a consistent, year-round effort to make the best lemonade possible out of the year’s lemons.

The above advice is not sexy, but it is a recipe, in our opinion, for long-term investing success. On behalf of the entire Strategic Financial Services team, I would like to thank our wonderful community of clients, associates, friends, and family. 2022 was not often an enjoyable one for investors, but yesterday’s weakness sets the disciplined investor up for tomorrow’s strength. May every day of the new year bring you one step closer to living your best life!

About Strategic

Founded in 1979, Strategic is a leading investment and wealth management firm managing and advising on total client assets of over $3 billion, as of 6/3/26.

Disclosures

Strategic Financial Services, Inc. is registered with the Securities and Exchange Commission (SEC) as an Investment Advisor. The term “registered” signifies compliance with regulatory requirements and does not imply a certain level of skill or training.

The information provided on our website, including weekly market commentaries, financial planning articles, and other educational resources, is intended solely for educational purposes. It is designed to offer insights into financial planning and investment management, aiming to enhance understanding of financial concepts, strategies, and market trends. This content should not be interpreted as personalized investment advice or a recommendation for any specific strategy, financial planning approach, or investment product. Financial decisions are deeply personal and should be made considering the individual’s specific circumstances, goals, and risk tolerance. We recommend consulting with a professional financial advisor for personalized advice.

Please be aware that Strategic Financial Services, Inc. does not provide legal or tax advice. The content on this website is not intended to be used as such or as a substitute for legal or tax advice from a licensed professional. We advise seeking guidance from qualified legal and tax advisors regarding these matters.

Investment Risks and Portfolio Management.

The discussion of any investments on this website is for illustrative purposes only and provides no guarantee that the advisor will make any investments with the same or similar characteristics as those presented. The investments identified and described herein do not represent all the investments purchased or sold for client accounts. The selection of representative investments to discuss is based on various factors, including recent company news or earnings releases.

It should not be assumed that any investments discussed were or will be profitable. All investments involve risk, including the potential loss of principal. There is no assurance that investments mentioned will remain in client accounts at the time you view this information.

When index returns are mentioned on this site, they are provided as a general indicator of market conditions and are not representative of any client’s portfolio performance. Indices are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. Therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

While index returns are used as a framework to report on general market conditions, they should not be construed as an indicator of future performance of any specific investment or portfolio. Discussion of index returns is intended to provide context and insight, not to suggest that clients will achieve similar results. Each client’s portfolio is managed according to their specific investment goals and financial situation.

The opinions and any forward-looking statements expressed in the articles and videos featured in our resource center are as of the date of publication. These statements are based on current laws, regulations, market conditions, and other relevant factors, including third-party data. Given the dynamic nature of financial and regulatory environments, as well as potential changes in market conditions or economic circumstances, the information provided may become outdated or may no longer be accurate.

We rely on third-party data to form our opinions and projections, which means that these are subject to the same uncertainties that affect all data-dependent analyses. As such, we advise readers to exercise caution and not rely solely on the statements made herein for making financial decisions. It is recommended that investors consult with a professional advisor who can help assess the relevance and accuracy of the content in light of the current economic climate and personal financial situation.

Our website contains links to third-party websites as a convenience to our users. Strategic Financial Services, Inc. does not control, endorse, or guarantee the content found on such sites. We are not responsible for the accuracy, legality, or content of the external site or for that of subsequent links.

Contact the external site for answers to questions regarding its content.

The inclusion of any link does not imply our endorsement of the site, nor does it imply any association with its operators. Use of any such linked website is at the user’s own risk.