Being Greedy in Times of Fear

The Federal Reserve’s heavy-handed fight against inflation was bound to break something, and this quarter, we found out what: bank balance sheets. The well-telegraphed rise in interest rates somehow caught some banks off guard, resulting in solvency fears, bank runs, bankruptcies, and bailouts. Through it all, US stocks had a strong quarter.

As we look forward to the rest of the year, the inflation and interest rate story still appears to have many chapters to be written. While the Fed has backstopped banks to stem the contagion of the recent crisis, other unintended consequences are undoubtedly possible. Yet, we entered 2023 with far more promise than a year ago when valuations were stretched for both stocks and bonds. Fear and uncertainty are admittedly high, yet historically that has been a good time to get greedy.

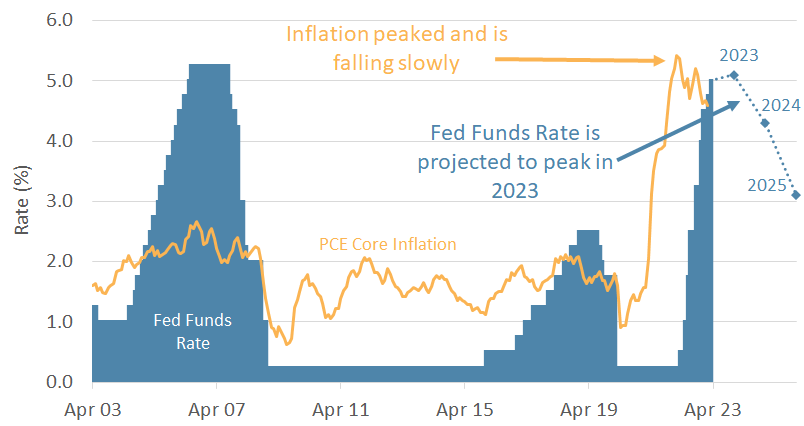

The Fed has moderated rate increases, with a peak in sight

Inflation is still high but slowing, and the Fed has eased its approach. There were two Fed Funds rate increases in Q1, both 25 bps. That is a significant slowdown from the meteoric pace of the past year, where 75 bps was the norm. Peak rates are now in sight. The latest average peak rate forecast by the Federal Reserve members is 5.1% in 2023, with declines to follow in subsequent years. From that estimate, it is clear that some Fed members believe we are already at the peak.

Chart 1: Peak in Sight for Inflation and Fed Funds Rates

Source: The US Federal Reserve, Bureau of Economic Analysis

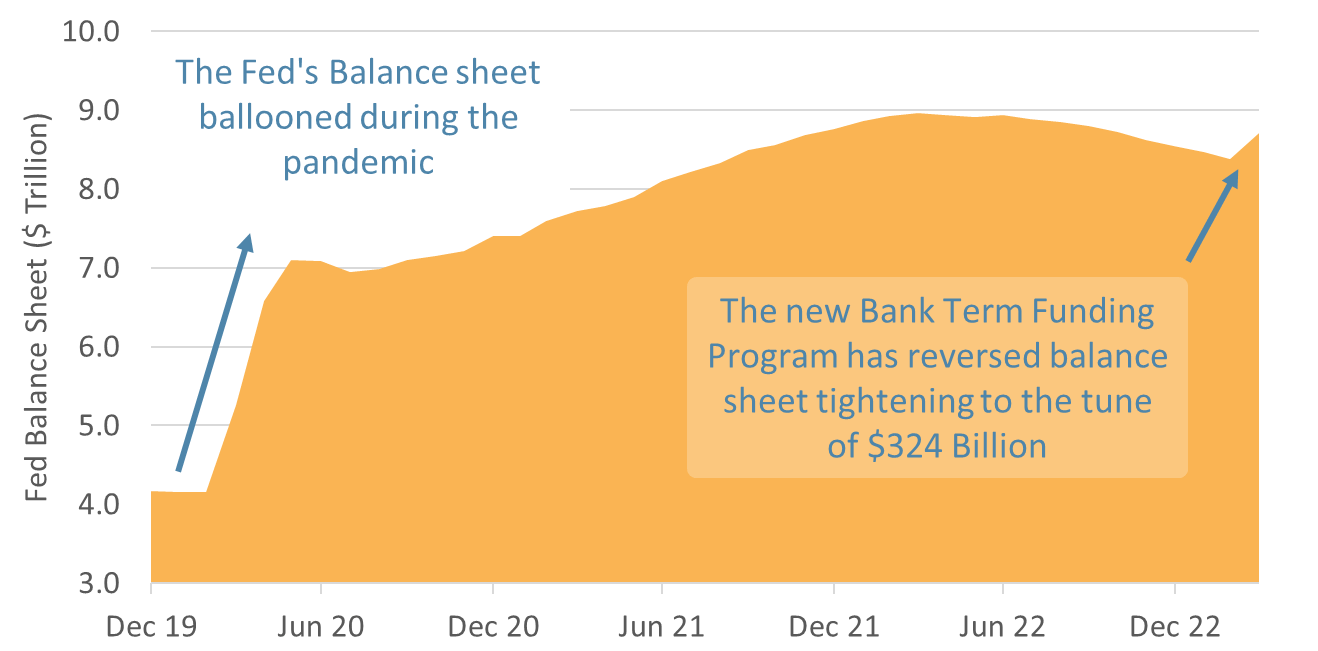

Rate increases exposed poorly constructed bond portfolios

While increases have moderated, banks are still reeling from the impact that past increases had on the value of their bond and loan portfolios. The rapid rate increase hit bond values and exposed those banks with too much duration in their portfolios, triggering a crisis of confidence and bank runs. Silicon Valley Bank and Signature Bank were high-profile poster children for the mini-banking crisis. The fallout may not be done, but for now, this was a problem specific to banks that did not do well matching their asset and liability exposures.

The Fed launched its Bank Term Funding Program to avoid additional bank runs and stem contagion. The program lends to banks allowing them to use the par value of their Treasuries and other qualifying assets as collateral. The Fed’s balance sheet grew $324B in March as financial institutions successfully utilized the facility.

Chart 2: The Fed Steps in to Calm Bank Fears

Source: Federal Reserve

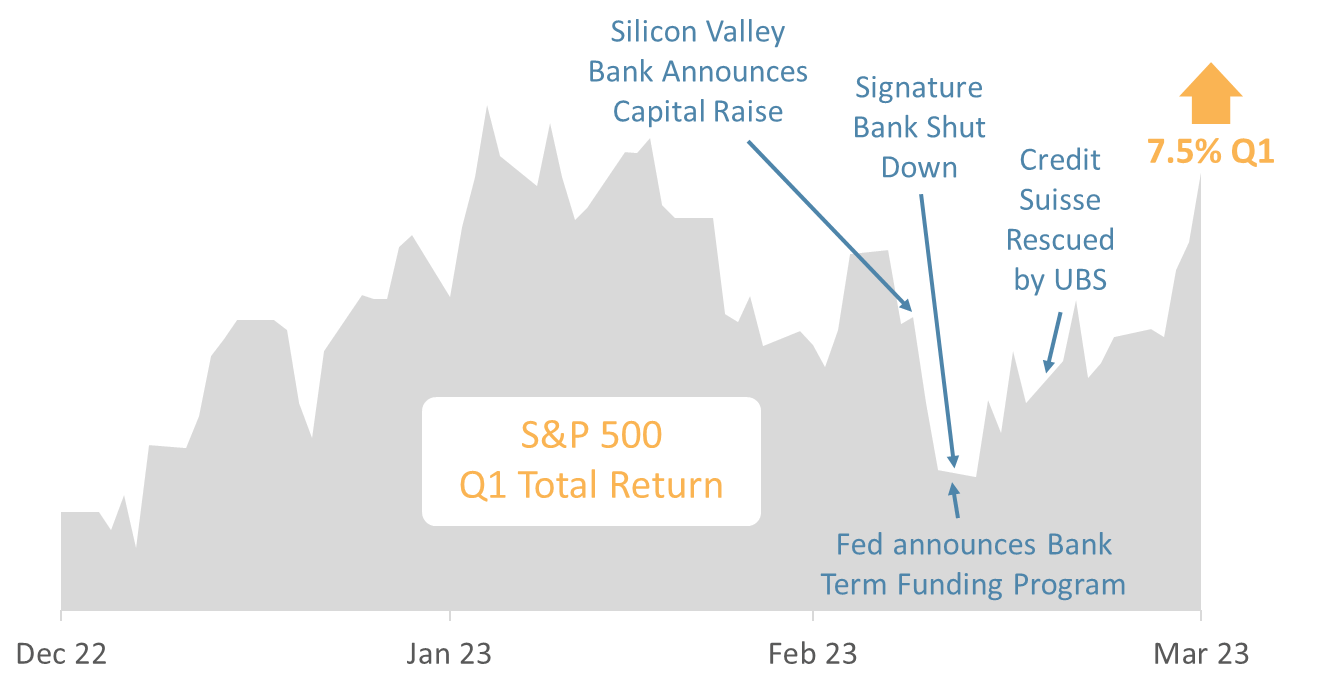

Stocks rose despite the barrage of dour headlines in Q1

There has been no shortage of scare stories this quarter, focusing on banking crisis contagion and the potential for recession. Despite that, the S&P 500 was up 7.5% in the first quarter and 16% from the October lows. Market recoveries can be swift and often start while the news flow is still at its worst. Investors should avoid falling into the trap of equating news and media sentiment with stock market returns.

Under the hood, the gains this year are largely a rebound in Tech. The top six companies in the S&P 500 (Apple, Microsoft, Amazon, Alphabet, Nvidia, Tesla) plus Meta accounted for over 80% of the upside in the S&P 500.

Chart 3: Stocks Defied Media Sentiment

Source: Factset

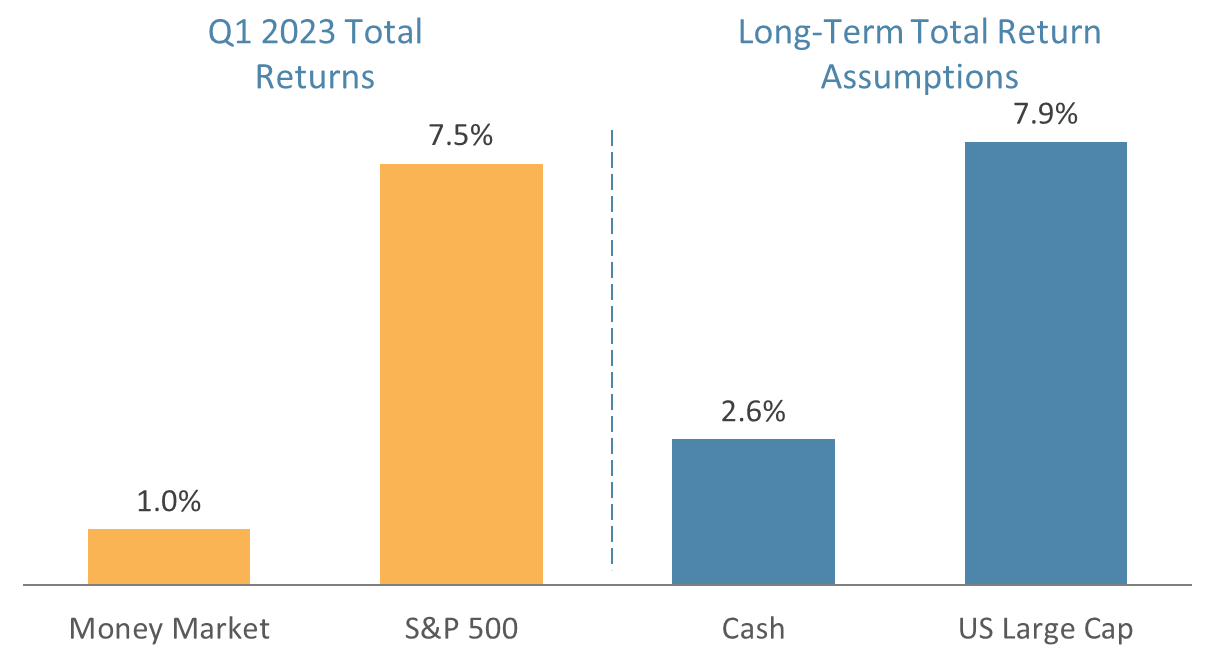

Higher yields do not necessitate allocation changes

The sell-off in bonds in 2022 raised yields across the fixed-income space and created a margin of safety not seen in many years. Investors can now enjoy earning yield on low-risk money market funds, but wholesale allocation changes are not justified in our view. Why? Fixed income is not the only asset class looking more attractive.

The 2022 sell-off in equities created opportunities for stocks as well. We saw a dramatic increase in the long-term expected returns of equities this year compared to last year’s start. As such, a higher allocation to cash and bonds may lock in higher yields, but it locks out the higher return potential of equities. This could limit portfolio returns and introduce unnecessary risk for long-term goals. In other words, attempts to de-risk portfolios could increase the chance that your long-term investing goals are missed.

Chart 4: De-Risking Can Add Unintended Risk

Source: Factset, Example MM w/4.2% yield, JP Morgan 2023 Long-Term Capital Market Assumptions

2023 has started on the right foot

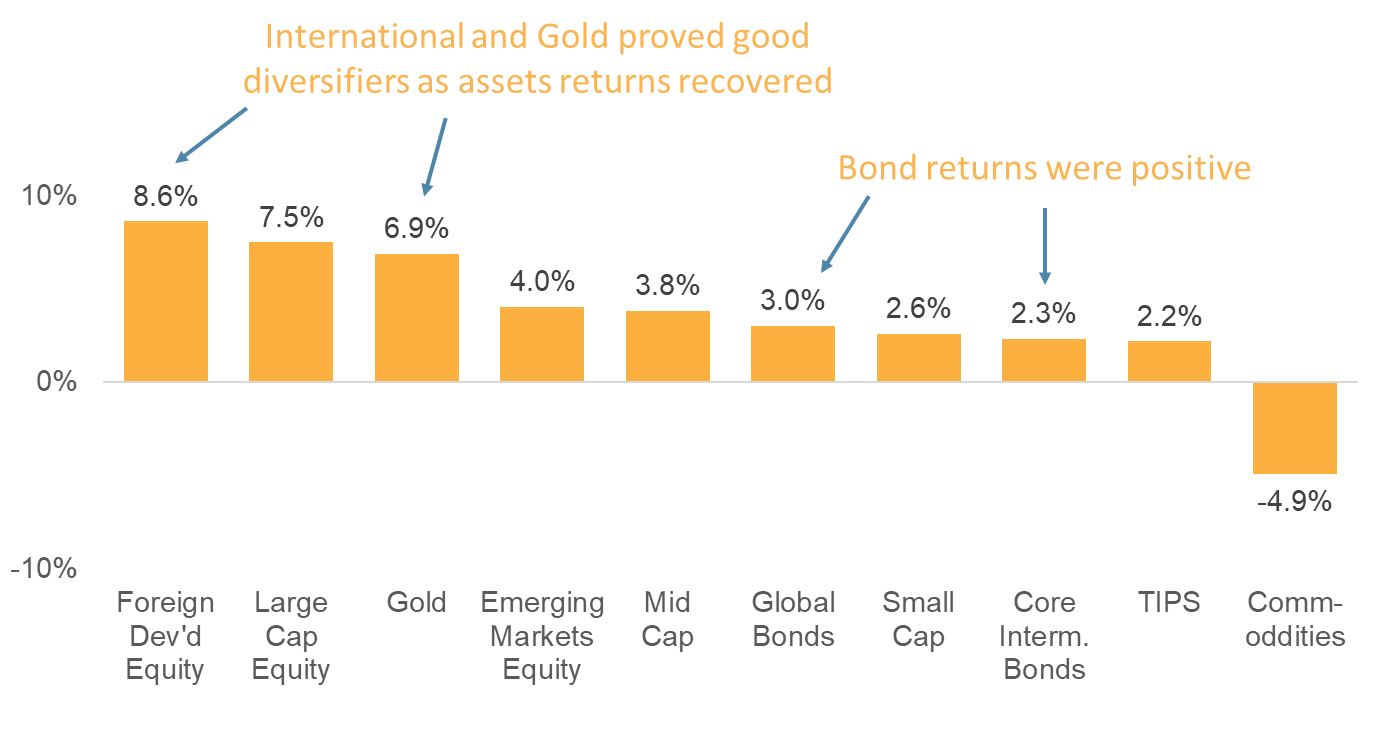

Poor returns in 2022 set up portfolios for better prospects in 2023, which played out in the first quarter. US Large Cap put in a strong performance, but Foreign Developed stocks were top of the returns table this year. Gold was also higher, continuing from a strong run in the fourth quarter. Both of these moves were a good reminder of the importance of diversification in a well-constructed portfolio.

It was also nice to see that bonds started the year in positive territory after the challenges in 2022. Commodities, the best performers last year, fell as energy prices moderated.

Chart 5: Asset Class Performance in Q1 2023

Source: Factset

Be “fearful when others are greedy, and greedy when others are fearful.”

– Warren Buffett

As we continue on the journey of 2023, we remain optimistic. As we said last quarter (in fact, we always say this), we are not predicting a market rebound this year. It is indeed a possibility, but that is not the source of our optimism. Instead, we take comfort in knowing that the 2022 market declines created a margin of safety for upside in both stocks and bonds that did not exist at the start of 2022.

We enter the second quarter with the luxury of high yields in our fixed-income instruments that we have not enjoyed for decades. Relatively safe money market funds earn upwards of four percent per year. The temptation in this environment is to de-risk… to allocate more of your portfolio to fixed income. For some, this may be a prudent move. For most, this is more likely to unnecessarily limit the upside of your portfolios and potentially even jeopardize your long-term savings goals.

Tactically, we are positioned to benefit from and enjoy the higher return potential that bonds offer today but remain fully invested in equities to capture their long-term return benefits. The long-term prospects for stock returns are still far greater than that of money markets and Treasuries, and we see no reason to reduce our exposure. In the words of Warren Buffett, we would much rather be “fearful when others are greedy, and greedy when others are fearful.” Right now, we see a lot of fear.

On behalf of the entire Strategic Financial Services team, I thank our incredible community of clients, associates, friends, and family for placing your trust in us. We appreciate your confidence and thoughtfulness in these unusual economic times.

About Strategic

Founded in 1979, Strategic is a leading investment and wealth management firm managing and advising on total client assets of over $3 billion, as of 6/3/26.

Disclosures

Strategic Financial Services, Inc. is registered with the Securities and Exchange Commission (SEC) as an Investment Advisor. The term “registered” signifies compliance with regulatory requirements and does not imply a certain level of skill or training.

The information provided on our website, including weekly market commentaries, financial planning articles, and other educational resources, is intended solely for educational purposes. It is designed to offer insights into financial planning and investment management, aiming to enhance understanding of financial concepts, strategies, and market trends. This content should not be interpreted as personalized investment advice or a recommendation for any specific strategy, financial planning approach, or investment product. Financial decisions are deeply personal and should be made considering the individual’s specific circumstances, goals, and risk tolerance. We recommend consulting with a professional financial advisor for personalized advice.

Please be aware that Strategic Financial Services, Inc. does not provide legal or tax advice. The content on this website is not intended to be used as such or as a substitute for legal or tax advice from a licensed professional. We advise seeking guidance from qualified legal and tax advisors regarding these matters.

Investment Risks and Portfolio Management.

The discussion of any investments on this website is for illustrative purposes only and provides no guarantee that the advisor will make any investments with the same or similar characteristics as those presented. The investments identified and described herein do not represent all the investments purchased or sold for client accounts. The selection of representative investments to discuss is based on various factors, including recent company news or earnings releases.

It should not be assumed that any investments discussed were or will be profitable. All investments involve risk, including the potential loss of principal. There is no assurance that investments mentioned will remain in client accounts at the time you view this information.

When index returns are mentioned on this site, they are provided as a general indicator of market conditions and are not representative of any client’s portfolio performance. Indices are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. Therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

While index returns are used as a framework to report on general market conditions, they should not be construed as an indicator of future performance of any specific investment or portfolio. Discussion of index returns is intended to provide context and insight, not to suggest that clients will achieve similar results. Each client’s portfolio is managed according to their specific investment goals and financial situation.

The opinions and any forward-looking statements expressed in the articles and videos featured in our resource center are as of the date of publication. These statements are based on current laws, regulations, market conditions, and other relevant factors, including third-party data. Given the dynamic nature of financial and regulatory environments, as well as potential changes in market conditions or economic circumstances, the information provided may become outdated or may no longer be accurate.

We rely on third-party data to form our opinions and projections, which means that these are subject to the same uncertainties that affect all data-dependent analyses. As such, we advise readers to exercise caution and not rely solely on the statements made herein for making financial decisions. It is recommended that investors consult with a professional advisor who can help assess the relevance and accuracy of the content in light of the current economic climate and personal financial situation.

Our website contains links to third-party websites as a convenience to our users. Strategic Financial Services, Inc. does not control, endorse, or guarantee the content found on such sites. We are not responsible for the accuracy, legality, or content of the external site or for that of subsequent links.

Contact the external site for answers to questions regarding its content.

The inclusion of any link does not imply our endorsement of the site, nor does it imply any association with its operators. Use of any such linked website is at the user’s own risk.