No Time for Fortune Telling

The second quarter of the year was a wild one for US equities – first falling over 10% in a week, then rallying over 20% before quarter’s end. Yet it was once again a time for diversifying assets to shine, as international equity performance benefited from a weak US dollar, and gold remained… well… shiny. With the economic outlook cloudy, and the tariff and inflation dynamics still weighing on the minds of the Fed officials, we stand poised to prepare for whatever may come.

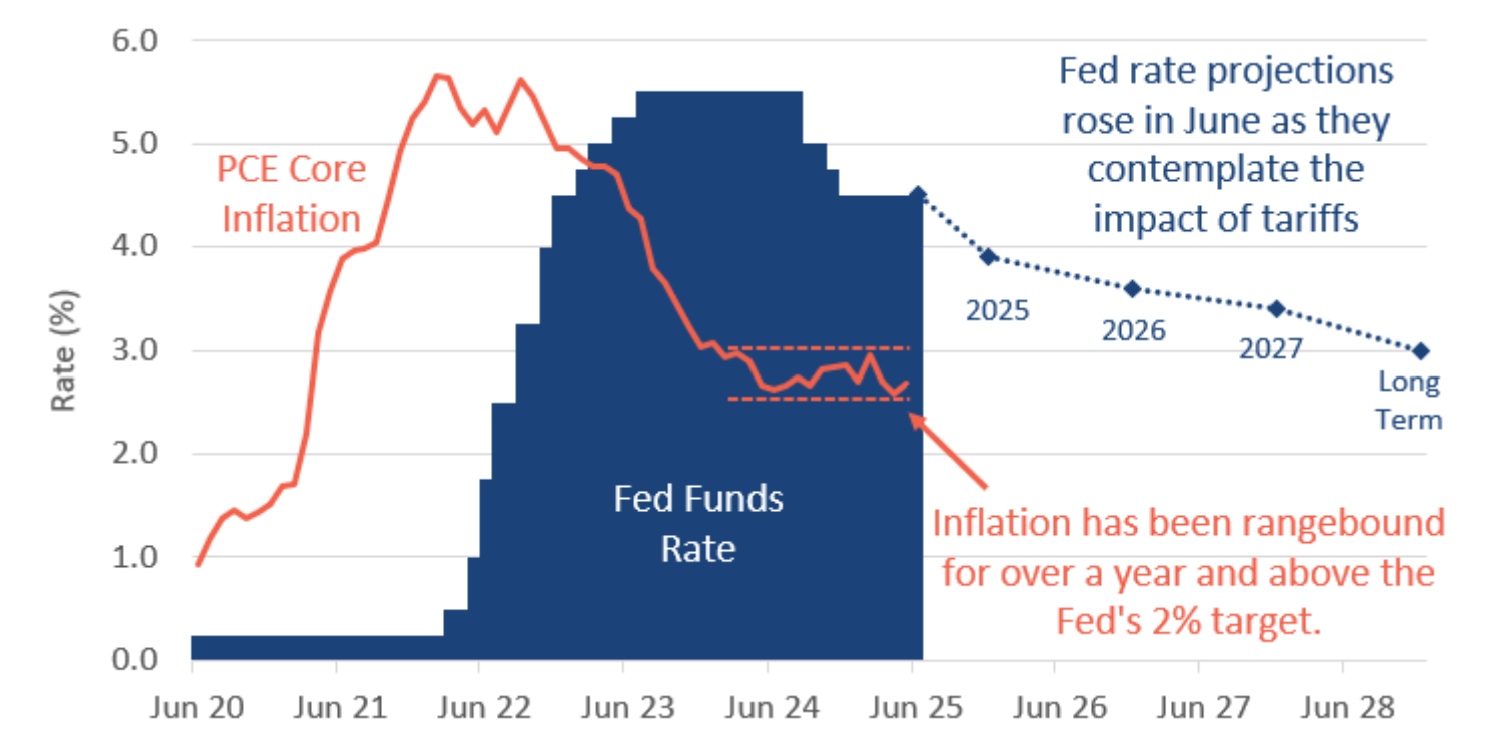

The Fed bumped up future rate expectations

Inflation continues to be a focus for market-watchers and it remained rangebound between 2.5% and 3.0% (as it has for over a year). The Fed wants to see continued progress toward their target of 2% inflation to justify additional rate cuts, but it is not budging. In addition, the Fed knows that the pending tariffs, tightened immigration controls and tax relief in the recent spending bill, are all widely considered inflationary policies. This is factoring into the rate decisions.

Why does it matter? The Fed’s high Interest rates are putting a damper on economic activity. Lower rates could stimulate economic investment and potentially be a positive for US equities. The next few months could provide some clues as to whether the inflation pressures will actually begin to push prices higher or not.

Chart 1: Inflation is rangebound

Source: The US Federal Reserve, Bureau of Economic Analysis

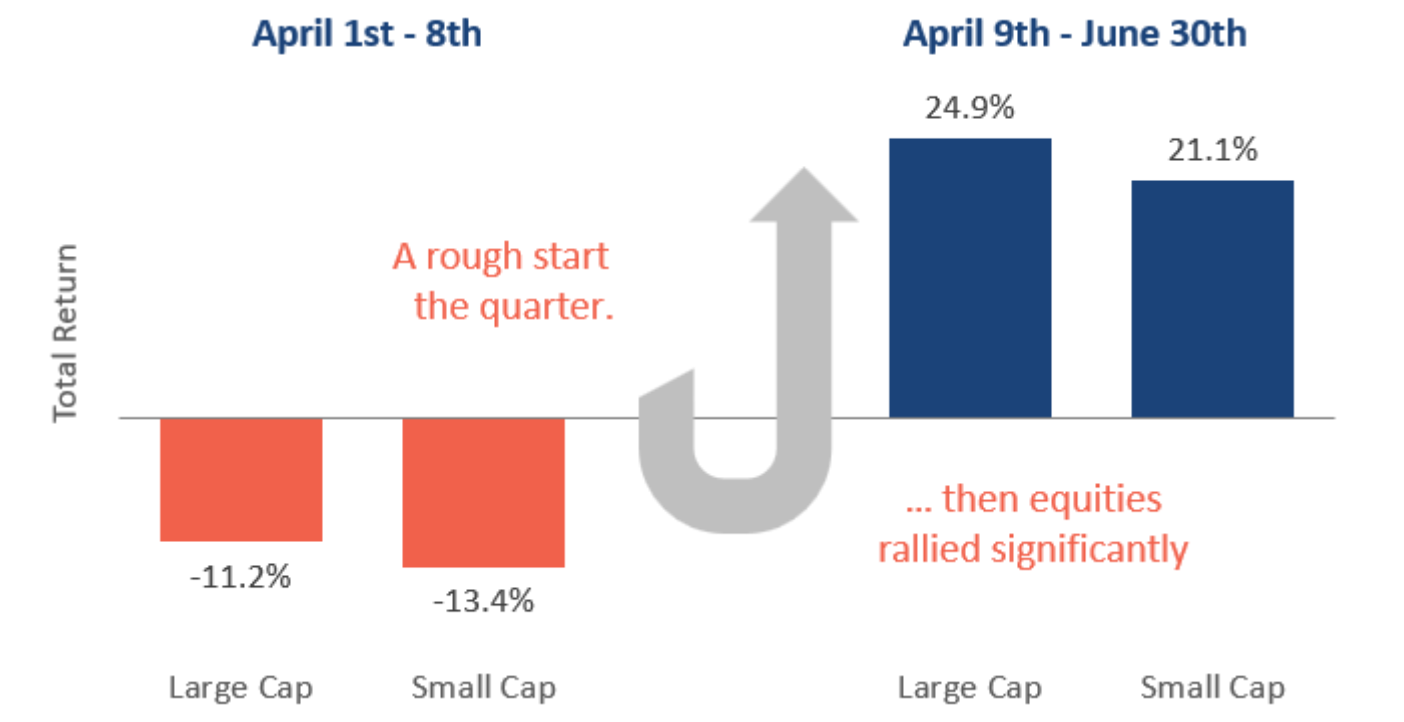

Equities started poorly, but recovered… and then some

US equities fell sharply to start the quarter; down double-digits in the first week of April. This followed an already weak first quarter resulting in a peak-to-trough decline of the S&P 500 of almost 20%. The decline was indiscriminate, with both large and small stocks weak. But the S&P 500 rebounded around 25%, as US large cap stocks outperformed small cap.

The quick turnaround is a useful reminder of the dangers of market timing. An investor with cold feet during the March and April stock market declines, may have missed the subsequent 25% rally. Evidence shows, market-timing does not pay off over time. Our playbook during this volatility included nimble rebalancing (we call opportunistic rebalancing). Evidence shows this has the potential to capitalize on these fleeting moments, by looking every week for moments to systematically sell high and buy low.

Chart 2: US equities fall… then rally

Source: Factset, S&P 500, S&P Small Cap 600

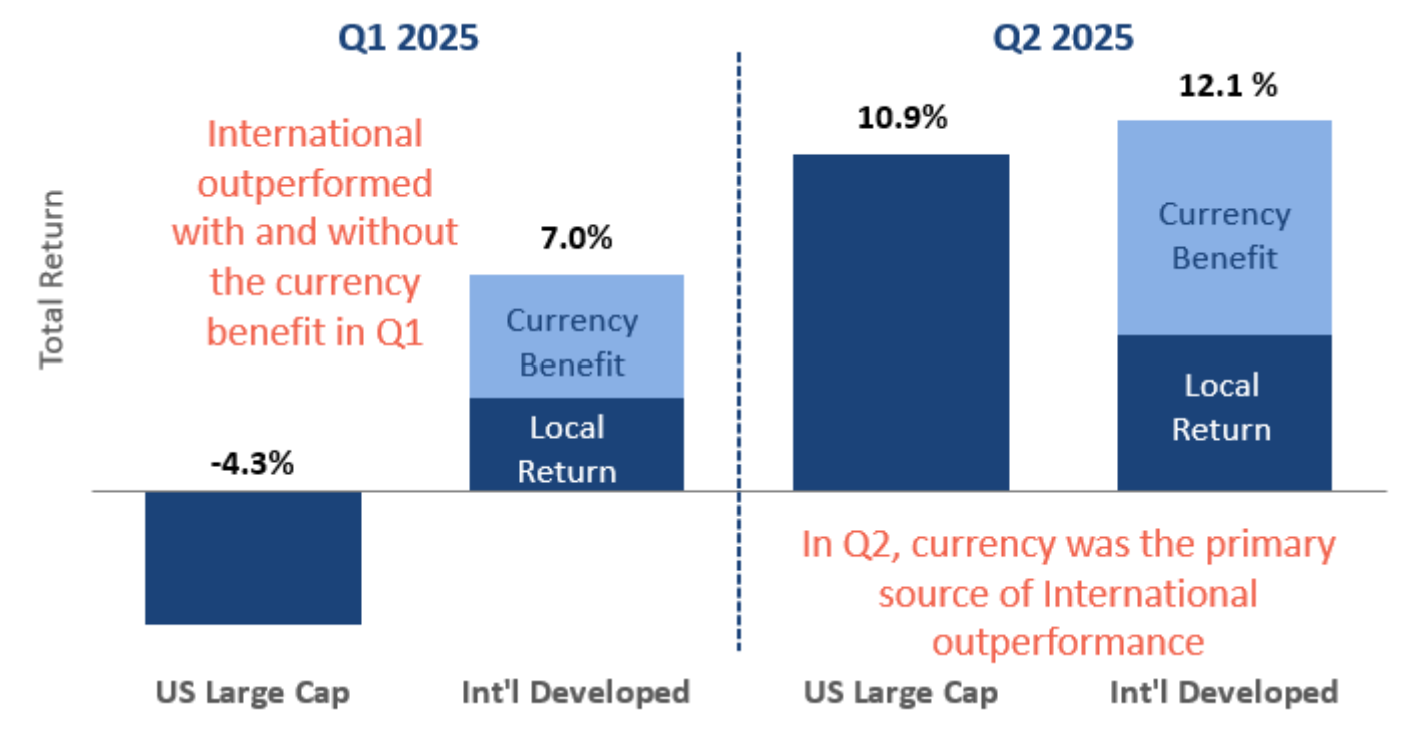

International strength continues as the dollar weakens

Well-diversified portfolios benefited from international holdings in the first half of the year. In the first quarter, foreign stocks significantly outperformed their US peers even before considering the US dollar weakness. While US stocks were down around -4%, international stocks were up about 3% in local currency and 7% in US dollar terms.

In the second quarter, international outperformed again. Both the US and international were up over 10%, but international received a 7% benefit from the weak US dollar.

Avoiding too much US home-bias has been beneficial in 2025. US equity strength in previous years has likely made high home-bias commonplace amongst asset allocators. But those instituting evidence-based investors will likely have avoided this lure.

Chart 3: International got a boost from a weak dollar

Source: Factset, S&P 500 index, MSCI EAFE

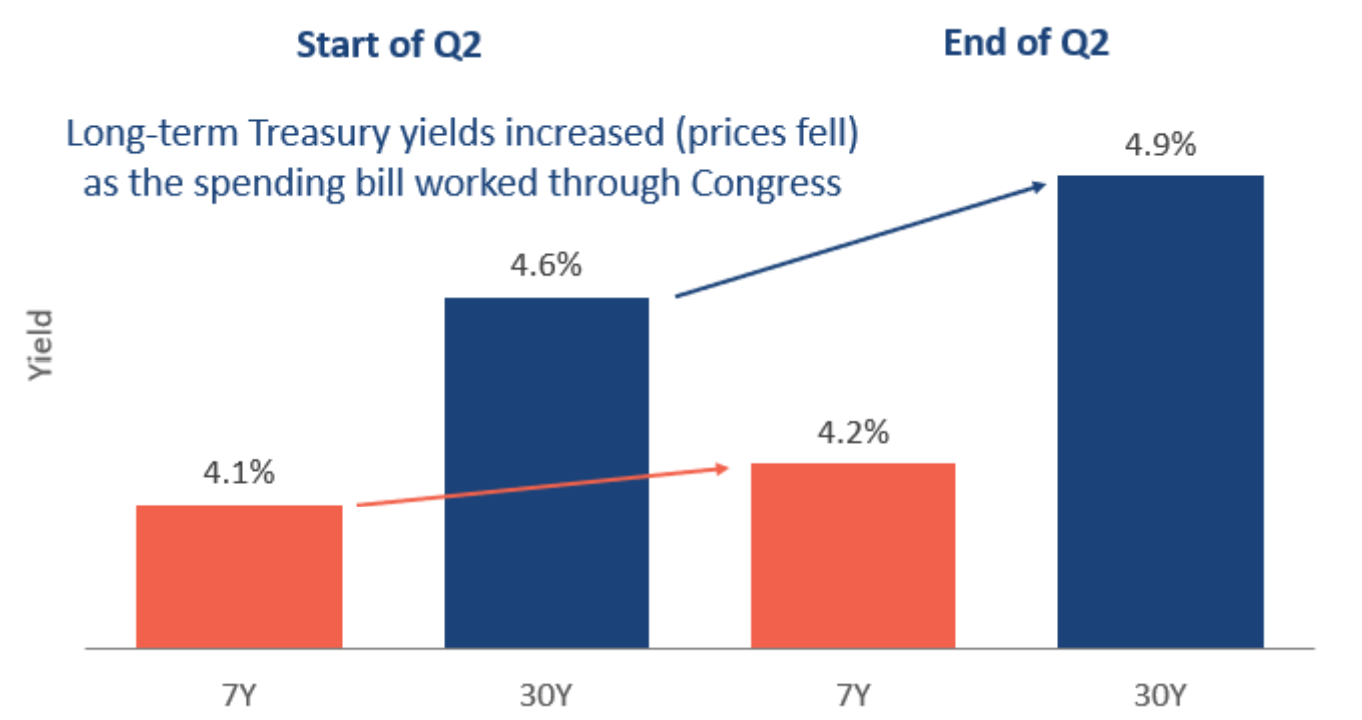

US debt concerns contribute to rising Treasury yields

The government’s spending bill did not pass until after the close of the quarter, but its impact was felt in the debt markets far in advance. Yields in longer-dated Treasuries (30Y) increased from 4.6% to 4.9%, while shorter-dated instruments were less affected. Investors are demanding higher yields from Treasuries to compensate for the higher risk that the additional debt burden brings.

As yields rise, prices fall, so longer-duration Treasuries underperformed in the second quarter. For example, Vanguard’s Short-Term Treasury ETF (VGSH) produced a total return of 1.2% in Q2, while their Long-Term Treasury ETF (VGLT) fell -1.5%.

Some allocation to longer-dated Treasuries is still warranted in our opinion for yield and volatility (rebalancing opportunities).

Chart 4: The spending bill impacted long-term Treasuries

Source: Factset, 7Y and 30Y benchmark Treasury indices

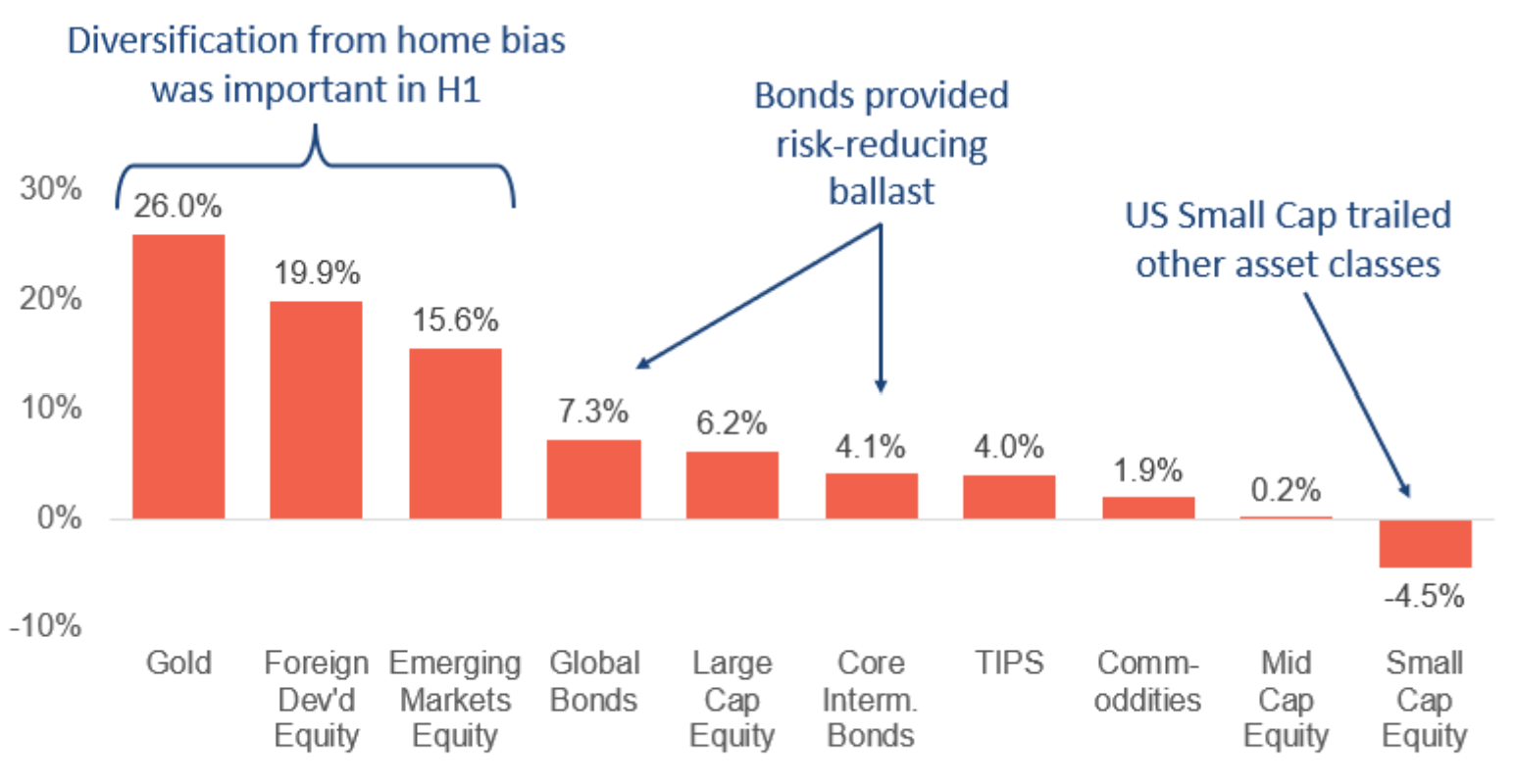

Gold and International shine as the tariff narrative plays out

A weak dollar and tariff uncertainty provided a backdrop in the first half of the year for outperformance from gold and International equities.

- Gold continues to advance, up 26%, driven by its perception as both an inflation hedge and safe-haven.

- International stocks significantly outperformed domestic stocks, helped by better valuations and currency.

- US small-cap stocks fell on fears they will bear the brunt of the tariff headwinds and higher-for-longer interest rates.

- US bonds produced positive returns despite recent weakness in longer-duration securities.

Chart 5: H1 2025 Asset Class Roundup

Source: Factset

“Trying to predict the future is like trying to drive down a country road at night with no lights while looking out the back window.” – Peter Drucker

The second quarter was a not-so gentle reminder to investors to remain patient. As we put pen to paper on Perspectives three months ago, the US equity market appeared to be in trouble. The tariff announcement caught investors off guard, and stocks were falling. Fast-forward three months, and equities are hitting all-time highs again. Patient investors were rewarded. But that is now behind us, so how should investors be thinking about the third quarter?

A no fortune-telling zone

It is commonplace in our industry to take these moments to pontificate about what the next three months will hold for investors. It’s a fool’s game. It may be comforting to read that all’s well and all will be well for investors this quarter, but it is conjecture. The future is unknowable and I’d be wary of any investor who bases their decisions on fortune-telling. As evidence-based investors, we will never do that. For us, preparation is far more important than prediction.

That is not to say we don’t think about the future. We think about it plenty. We consider the possible and take steps to be prepared for those possibilities (as well as some we may not have thought of). So, what does preparation look like? Here are a few examples:

- Diversification (international, bonds, gold, emerging, etc.).

- Tilting exposure to areas of the market that have historically performed well in times like these (e.g. factors like momentum as well as uncertainty hedges like gold).

- Avoiding unproven assets and those that have greater potential to suffer permanent loss of value (e.g. cryptocurrencies and perhaps private credit?).

- Avoid high-cost private equity investments with questionable return benefits and limited liquidity (Harvard and Yale’s castaways are headed for retail investors).

- Sophisticated trading systems and logic that can systematically sell high and buy low when the opportunities arise (i.e. take advantage of big market moves).

For us, good investing is about stringing together a series of small, evidence-based decisions, each designed to tip the scales in favor of our client’s portfolios. That is how we deal with the uncertainty of tariffs. That is how we deal with the uncertainty of inflation. Instead of trying to predict the unpredictable, we focus on what we can control, to help prepare for whatever comes our way. It’s not meant to be flashy. It’s meant to be good investing.

Thank you again to our clients, friends and family who have joined our Strategic community and place their trust in us. We look forward to opportunities to collaborate and elevate in the coming quarter.

About Strategic

Founded in 1979, Strategic is a leading investment and wealth management firm managing and advising on total client assets of over $3 billion, as of 6/3/26.

Disclosures

Strategic Financial Services, Inc. is registered with the Securities and Exchange Commission (SEC) as an Investment Advisor. The term “registered” signifies compliance with regulatory requirements and does not imply a certain level of skill or training.

The information provided on our website, including weekly market commentaries, financial planning articles, and other educational resources, is intended solely for educational purposes. It is designed to offer insights into financial planning and investment management, aiming to enhance understanding of financial concepts, strategies, and market trends. This content should not be interpreted as personalized investment advice or a recommendation for any specific strategy, financial planning approach, or investment product. Financial decisions are deeply personal and should be made considering the individual’s specific circumstances, goals, and risk tolerance. We recommend consulting with a professional financial advisor for personalized advice.

Please be aware that Strategic Financial Services, Inc. does not provide legal or tax advice. The content on this website is not intended to be used as such or as a substitute for legal or tax advice from a licensed professional. We advise seeking guidance from qualified legal and tax advisors regarding these matters.

Investment Risks and Portfolio Management.

The discussion of any investments on this website is for illustrative purposes only and provides no guarantee that the advisor will make any investments with the same or similar characteristics as those presented. The investments identified and described herein do not represent all the investments purchased or sold for client accounts. The selection of representative investments to discuss is based on various factors, including recent company news or earnings releases.

It should not be assumed that any investments discussed were or will be profitable. All investments involve risk, including the potential loss of principal. There is no assurance that investments mentioned will remain in client accounts at the time you view this information.

When index returns are mentioned on this site, they are provided as a general indicator of market conditions and are not representative of any client’s portfolio performance. Indices are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. Therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

While index returns are used as a framework to report on general market conditions, they should not be construed as an indicator of future performance of any specific investment or portfolio. Discussion of index returns is intended to provide context and insight, not to suggest that clients will achieve similar results. Each client’s portfolio is managed according to their specific investment goals and financial situation.

The opinions and any forward-looking statements expressed in the articles and videos featured in our resource center are as of the date of publication. These statements are based on current laws, regulations, market conditions, and other relevant factors, including third-party data. Given the dynamic nature of financial and regulatory environments, as well as potential changes in market conditions or economic circumstances, the information provided may become outdated or may no longer be accurate.

We rely on third-party data to form our opinions and projections, which means that these are subject to the same uncertainties that affect all data-dependent analyses. As such, we advise readers to exercise caution and not rely solely on the statements made herein for making financial decisions. It is recommended that investors consult with a professional advisor who can help assess the relevance and accuracy of the content in light of the current economic climate and personal financial situation.

Our website contains links to third-party websites as a convenience to our users. Strategic Financial Services, Inc. does not control, endorse, or guarantee the content found on such sites. We are not responsible for the accuracy, legality, or content of the external site or for that of subsequent links.

Contact the external site for answers to questions regarding its content.

The inclusion of any link does not imply our endorsement of the site, nor does it imply any association with its operators. Use of any such linked website is at the user’s own risk.