Panamanian Panic

Doug Walters

Doug Walters

The S&P 500 had a good week leading up to the tax filing deadline. For some, these gains may eventually lead to tax payments, but this is a luxury problem. Those named in the Panama Papers are probably regretting taking this luxury for granted.

Market Review

Contributed by Doug Walters

A Taxing Weekend

Tax season is upon us. While hopefully your weekend plans do not include spending time with 1099’s and supplemental worksheets, tax filers do have a few extra days to file this year thanks to the Emancipation Day holiday in Washington DC.

- We actively manage taxable gains year round; when appropriate using tax losses to offset gains.

- Paying taxes on capital gains is a luxury problem though; the byproduct of positive investment performance.

- The alternatives… poor investment performance or your name in the Panama Papers… are far worse.

Capital Gains

Equities have had a good start to the second quarter, continuing the momentum from March. Some of the positive sentiment is coming from China where there are signs that declining growth has begun to stabilize.

- We would approach this news somewhat cautiously. China’s economic statistics are notoriously unreliable, and often contradict empirical evidence on the ground.

- China is attempting to transition from an economy driven by massive state-owned enterprises to one driven by the consumer. While we agree this transformation is gaining ground, it is likely to be a bumpy ride, and we believe it is too soon to assume success.

| Indices & Price Returns | Week (%) | Year (%) |

|---|---|---|

| S&P 500 | 1.6 | 1.8 |

| S&P 400 (Mid Cap) | 2.6 | 4.7 |

| Russell 2000 (Small Cap) | 3.1 | -0.4 |

| MSCI EAFE (Developed International) | 3.5 | -2 |

| MSCI Emerging Markets | 3.5 | 6.5 |

| S&P GSCI (Commodities) | 3.2 | 9 |

| Gold | -0.4 | 16.2 |

| MSCI U.S. REIT Index | 0.2 | 4.7 |

| Barclays Int Govt Credit | -0.1 | 2.2 |

| Barclays US TIPS | -0.5 | 4.2 |

Economic Commentary

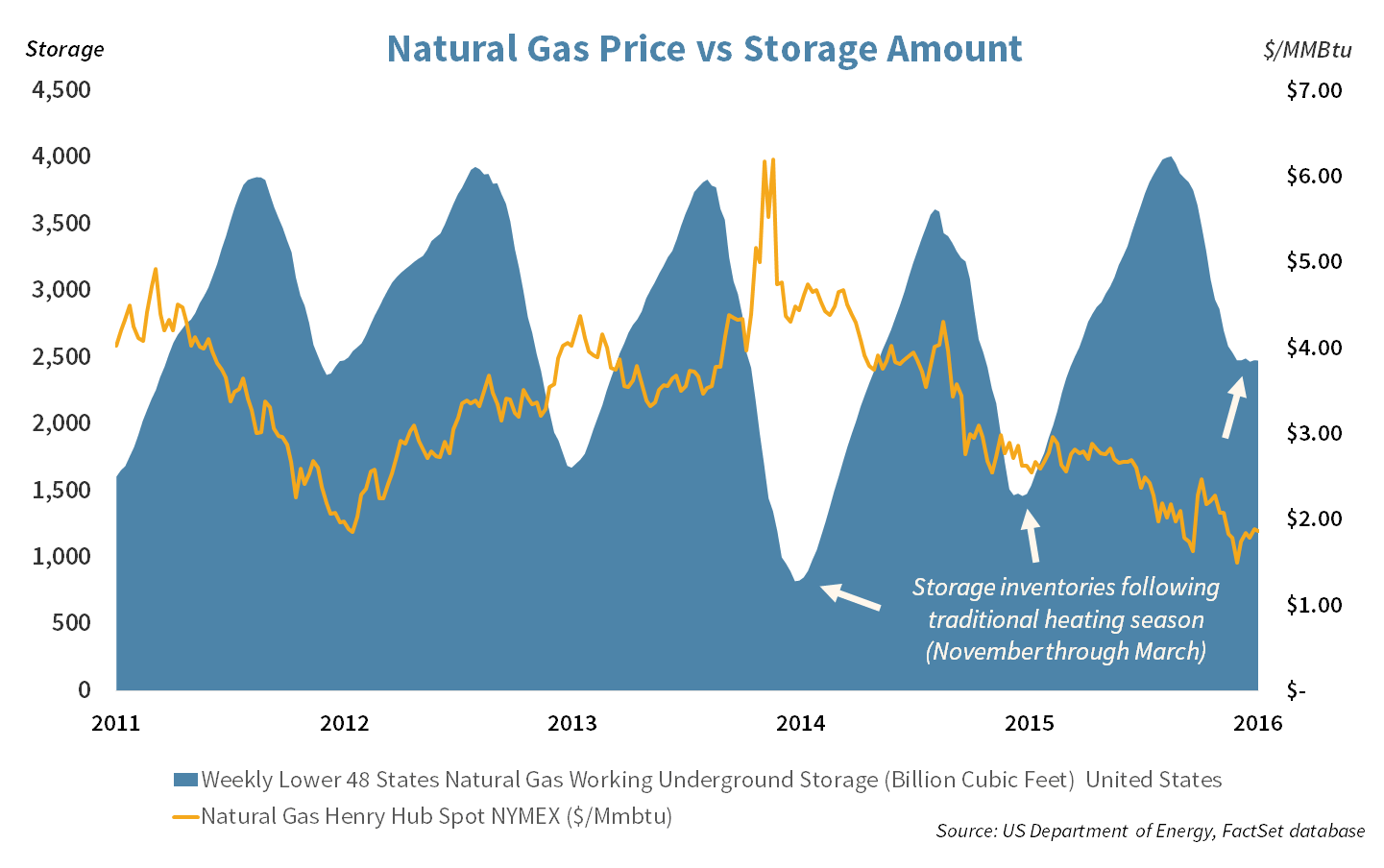

Have natural gas prices bottomed?

You may have noticed from your heating bills this past winter that natural gas prices are low. This is due to supply outweighing demand, leading to record natural gas storage amounts (shown below). The two main drivers of demand are:

- Heating homes, and

- Electricity generated by gas fueled power plants.

Both drivers have been weak this past year due to the mild winter and power plants having access to a glut of unused coal.

Despite the near term problems, our long term view is that natural gas demand will be strong. Three factors driving demand growth are:

- Liquefied Natural Gas (LNG) where natural gas is liquefied, exported and then re-gasified for use abroad,

- Power plants switching from using coal to natural gas in order to meet new environmental regulations, and

- Exports by pipeline to Mexico as the country’s need for the commodity grows.

Natural gas supply has increased as wells in the Appalachian basin, stretching along Pennsylvania, New York, West Virginia and Ohio, have out-produced geological expectations. We believe that supply will eventually rebalance as producing companies are spending less on drilling given the low price environment.

Week Ahead

Contributed by Aaron Evans

Home Field Advantage?

The presidential primary showdown will be right in our backyard next week in New York which is one of the last major battlegrounds for delegates before the national conventions.

- All signs point to Trump winning easily in his home state on the GOP side, while former NYS Senator Clinton is getting more competition than she would like from Bernie Sanders.

Bottom Line

More companies will report first quarter earnings next week, with Strategic holdings Microsoft, General Electric and Pepsico set to report among others.

- As earnings season gets into gear, we will start to see how companies fared amidst first quarter volatility in both the stock market and energy prices.

Ease-y Money

Overseas the European Central Bank will hold its monetary policy meeting followed by a press conference from President Mario Draghi.

- The meetings comes off the heels of the ECB’s March decision to expand stimulus measures (QE) in the Euro area in hopes of accelerating both economic growth and inflation.

Strategy Update

Contributed by David Lemire , Max Berkovich

Strategic Asset Allocation

Mid-month check in

Most equity markets are up strongly since a February 11th low. Growth, Value, and Developed International have posted mid-teen gains recently. These markets represent our larger weightings and thus have helped overall portfolio performance of late. Meanwhile, Small Cap and Emerging Markets have clocked upper teens and mid-20’s respectively over the same time frame. Their role is more complementary and thus do not pack quite the same punch on portfolios.

Bond markets have eased back off of a strong start to the month. TIPS and International have pulled back the most over the past two weeks but the moves have not been significant. Gold has pulled back slightly more than bonds after a strong rally since mid-January. In addition, REITs have started the month on a down note.

Overall, our growth assets are mostly in slight overweight positions with bonds slightly underweight. Central bankers and oil seem set to continue their dominant role in setting the market’s direction with negative rates and diminishing hopes for supply containment the latest themes.

STRATEGIC Growth

Half a world apart

Financials had a tremendous week thanks to sector bellwethers having a “not as bad as expected” earnings season. Consumer staples had a losing week. In other strategy news…

- The spice and packaged foods company McCormick & Co. (MKC) walked away from its attempt to acquire Premier Foods PLC a British packaged food company. A reasonable price could not be agreed upon. The Japanese firm Nissin Foods that holds a 20% stake in Premier was likely the unwilling party.

STRATEGIC Equity Income

Like a rock

Telecom, utilities, & consumer staples were laggards as the cyclical sectors took charge this past week. On the earnings front…

- JP Morgan & Co. (JPM) reported a quarter that beat estimates, but net income was lower than last year. Consumer & Community banking income was up 12% y/y, but other segments all saw declines. Progress on expenses and success in traditional banking outweighed a tough quarter from investment banking.

- Investment management giant BlackRock, Inc. (BLK) missed consensus expectations, but positive trends in the iShares unit helped overcome other negatives. $36.1 billion of long-term net inflows also helped.

About Strategic

Founded in 1979, Strategic is a leading investment and wealth management firm managing and advising on client assets of over $2 billion.

OverviewDisclosures

Strategic Financial Services, Inc. is a SEC-registered investment advisor. The term “registered” does not imply a certain level of skill or training. “Registered” means the company has filed the necessary documentation to maintain registration as an investment advisor with the Securities and Exchange Commission.

The information contained on this site is for informational purposes and should not be considered investment advice or a recommendation of any particular security, strategy or investment product. Every client situation is different. Strategic manages customized portfolios that seek to properly reflect the particular risk and return objectives of each individual client. The discussion of any investments is for illustrative purposes only and there is no assurance that the adviser will make any investments with the same or similar characteristics as any investments presented. The investments identified and described do not represent all of the investments purchased or sold for client accounts. Any representative investments discussed were selected based on a number of factors including recent company news or earnings release. The reader should not assume that an investment identified was or will be profitable. All investments contain risk and may lose value. There is no assurance that any investments identified will remain in client accounts at the time you receive this document.

Some of the material presented is based upon forward-looking statements, information and opinions, including descriptions of anticipated market changes and expectations of future activity. Strategic Financial Services believes that such statements, information, and opinions are based upon reasonable estimates and assumptions. However, forward-looking statements, information and opinions are inherently uncertain and actual events or results may differ materially from those reflected in the forward-looking statements. Therefore, undue reliance should not be placed on such forward-looking statements, information and opinions.

No content on this website is intended to provide tax or legal advice. You are advised to seek advice on these matters from separately retained professionals.

All index returns, unless otherwise noted, are presented as price returns and have been obtained from Bloomberg. Indices are unmanaged and cannot be purchased directly by investors.