2017: The Road Ahead

Doug Walters

Doug Walters

In this edition of Insights, the Strategic Investment Team breaks from our normal format to focus on the outlook for the coming year.

Market Review

Contributed by Doug Walters

In our year-end letter last week, we emphasized the futility of predicting, and made the distinction between this black art and disciplined investing. Despite this prudent advice, we cannot resist pulling out our crystal ball in this first week of 2017 to provide our best guesses for the year that lies ahead.

Opposing forces

With the incoming administration comes enormous uncertainty, which we expect to result in periods of notable volatility for markets. Specifically, we predict:

- A slowly rising Fed Fund rates will favor short duration bond portfolios over the broader bond market and will offer opportunity to pick up higher yields going forward.

- Equities will face two opposing forces: the downward pressure of above-average valuation and the tailwind of investors exiting bonds.

- Additional uncertainty will come from continued tweet-targeting of Individual companies and sectors by the incoming president.

- As a result, we expect more modest equity returns in 2017 as earnings try to catch up to valuation (Prediction S&P 500 +5%)

- In this environment, we believe active management is going to be increasingly important.

Better to be lucky

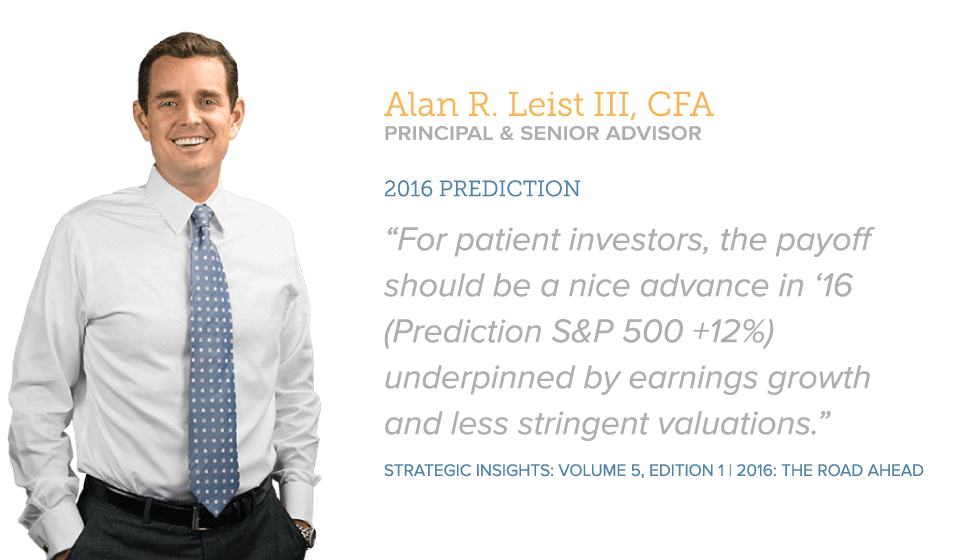

The best part of predictions is going back a year later to see just how far off you were. Last year Alan Leist III spearheaded our market predictions. He correctly predicted we would avoid a recession, the Fed would tighten a bit and we would experience a prolonged but fleeting slump (February definitely qualified). His prediction for the S&P 500 was +12%. Sadly he was way off here, as the index closed up +11.98%. Better luck next year Alan.

Economic Commentary

Coming off a solid yet volatile economic year in 2016, we take a look at the potential economic drivers for the year ahead.

Key Issues

Monetary Response

The Federal Reserve responded to market weakness early last year by once again kicking the can down the road. They were expected to raise interest rates three times last year but instead raised it only once at year end. Multiple rate increase are again forecast this year, but implementation will continue to depend on unemployment, inflation and perhaps the market.

The Trump Trade

The Donald trumped presidential politics and won the election on a protectionist platform with promises of steep tax cuts. The market rallied on his win with the S&P 500 up over 6% since the election. Promises of tax cuts and higher infrastructure spend could be a ‘huge’ fiscal stimulus to the economy, leading to higher GDP growth.

Global Protectionism

The surprise decision of the British to leave the European Union may be the beginning of a trend for other European countries to adopt the same protectionist policies. The ‘populist’ decision may stop the flow of migration to the United Kingdom which would protect middle-class jobs but may adversely affect GDP. If other countries follow suit, global trade could come under pressure.

2017 Predictions

The changing political and fiscal landscape will create economic winners and losers. We predict:

- Most companies will directly benefit from a lower corporate tax rate and less regulation. Coal and Oil & Gas companies, for example, have been highly regulated by the Environment Protection Agency and will benefit from less regulation. Renewable energy companies on the other hand will lose as they no longer enjoy the political incentives that encourage clean energy.

- Companies who rely on cheap imports from places such as China and Mexico will face headwinds as protectionist tariffs increase.

- Inflation will finally pick up as import taxes and fiscal stimulus lead to higher prices. A tightening labor market will enable employees to have more bargaining power and therefore higher wages.

- The Federal Reserve will monitor the above dynamics in deciding whether to raise interest rates. Consensus expectations are for them to raise rates three times this year but we predict fewer.

- Shale oil producers will once again flood the oil market after OPEC nations cut production in line with their quotas. The price of oil will start the year moving higher only to fall in an oversupplied market.

Year Ahead

Around the Globe

It’s been 6 years now, and Greek debt problems continue to pile up. We expect this to come to a head in 2017 as the IMF is cutting the bailouts after Greek lawmakers approved pension bonuses in 2016. However, besides the turmoil in Greece, there are a number of events around the globe that may impact world markets, particularly on the political front:

- Declaration of Article 50 lead by British Prime Minister Theresa May, initiating Brexit.

- Elections in France, where Marine Le Pen, the leader of the anti-immigrant National Front Party, has a shot to win.

- German elections might replace Chancellor Angela Merkel. Top candidate is leader of the Social Democratic Party (SPD) Sigmar Gabriel.

- An election for a new Prime Minister of Italy, as Matteo Renzi has resigned after the country voted against government reform referendum. Maybe this time Beppe Grillo the actor/comedian and leader of the Five Star Movement party will take the top job.

- Elections in Netherlands, where anti-immigration parties have picked up a lot of support.

- Iranian presidential election, which can trigger more headaches over nuclear deal with U.S. Current front runner is Hassan Rouhani, the incumbent.

- The Olympic Committee will decide where 2024 Summer Olympics will be held. The three candidates are Los Angeles, Budapest and Paris.

17 Trends/Events for ’17

Rate Hikes | Deportation | Higher Drug Prices | Lower Oil Prices | Tension in Middle East | Le Pen | Spread of Populism | Samsung Galaxy 8 on fire | Robots | OPEC Cheats | SnapChat | Russia | Star Wars | #MAGA | Calexit | Cost of Free Trade | Hot Coal |

Strategy Updates

Contributed by Max Berkovich ,

STRATEGIC ASSET ALLOCATION

Bumpy road ahead

There were a number of positive economic events last year that helped equity markets to push through new highs. The positive momentum might persist through this year but surly not without roadblocks. With uncertainty of how a new administration delivers on its agenda, we expect volatility to offer more rebalancing opportunities than 2016.

Bond Migration

Expectations for higher rates have sent fixed income yields higher. The market is expecting 2 to 3 rate hikes this year, and if the Fed sticks with their plan the 10-Year Treasury might finally push through the 3% yield level. Any surprises to the economic data or inflation, could result in aggressive bond selling.

Dollar Daze

In 2016, the U.S. Dollar had a strong rally as the economy improved faster than other developed markets. With a more protectionist bent and expectations of a stronger economy in the U.S., we expect further strength in the dollar. Be ready for plenty of retaliatory action from other global players as they try to maintain the standing of their own currency.

STRATEGIC GROWTH

Accounting for IT

Our bottom up work kept us out of high-flying Information Technology and social media names, whose valuations offered us little margin of safety. While our focus on valuation and quality steered us toward the Industrial space where global giants were under appreciated.

The top Stock was Caterpillar Inc. (CAT) while McKesson Corp. (MCK) came in last.

- 2016’s Stock Spotlight: Hain Celestial Group (HAIN 12/31/15 $40.39, 12/30/16 $40.42) did not achieve our hefty expectations. An accounting procedure review halted an impressive run and eliminated the possibility of a takeover by a traditional packaged food company (at least in 2016).

- 2017 Stock Spotlight: LKQ Corp. (LKQ) is a company that provides aftermarket car parts to repair shops. With a snow-filled winter and an increase in distracted driving, we see positive catalysts for earnings growth (besides the company has “Quality” in its name).

STRATEGIC EQUITY INCOME

Bank Shot

Even though the Telecom and Energy sectors provided stronger returns, it is the sheer size of the Financial sector that was responsible for driving the performance in the strategy.

Top Stock was Spectra Energy (SE) while CVS Corp. (CVS) came in last.

- 2016’s Stock Spotlight: BB&T Bancorp (BBT 12/31/15 $36.61, 12/30/16 $47.02) while not our top performer it was in the top ten. The entire bank space received a welcomed boost in the latter part of the year, as higher interest rates and hopes for a stronger economy and reduced regulatory burden allowed a cheap sector to catch up with the market’s valuation.

- 2017 Stock Spotlight: CVS Caremark Corp. (CVS) the pharmacy and pharmacy benefit management (PBM) company faced many headwinds in 2016. We see the company shaking off the subscriber losses and a stronger competitor in Walgreens (WBA) while it integrates its two most recent acquisitions in Omnicare and Target Pharmacies. The company has already increased its dividend by 18% and authorized an $18 Billion 5-year share buyback program.

About Strategic

Founded in 1979, Strategic is a leading investment and wealth management firm managing and advising on client assets of over $2 billion.

OverviewDisclosures

Strategic Financial Services, Inc. is a SEC-registered investment advisor. The term “registered” does not imply a certain level of skill or training. “Registered” means the company has filed the necessary documentation to maintain registration as an investment advisor with the Securities and Exchange Commission.

The information contained on this site is for informational purposes and should not be considered investment advice or a recommendation of any particular security, strategy or investment product. Every client situation is different. Strategic manages customized portfolios that seek to properly reflect the particular risk and return objectives of each individual client. The discussion of any investments is for illustrative purposes only and there is no assurance that the adviser will make any investments with the same or similar characteristics as any investments presented. The investments identified and described do not represent all of the investments purchased or sold for client accounts. Any representative investments discussed were selected based on a number of factors including recent company news or earnings release. The reader should not assume that an investment identified was or will be profitable. All investments contain risk and may lose value. There is no assurance that any investments identified will remain in client accounts at the time you receive this document.

Some of the material presented is based upon forward-looking statements, information and opinions, including descriptions of anticipated market changes and expectations of future activity. Strategic Financial Services believes that such statements, information, and opinions are based upon reasonable estimates and assumptions. However, forward-looking statements, information and opinions are inherently uncertain and actual events or results may differ materially from those reflected in the forward-looking statements. Therefore, undue reliance should not be placed on such forward-looking statements, information and opinions.

No content on this website is intended to provide tax or legal advice. You are advised to seek advice on these matters from separately retained professionals.

All index returns, unless otherwise noted, are presented as price returns and have been obtained from Bloomberg. Indices are unmanaged and cannot be purchased directly by investors.